Advertisement

3 Stocks That May Be Trading Up To 42.2% Below Intrinsic Estimates

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of rising U.S. Treasury yields and tepid economic growth, investors are keenly observing how these factors impact stock valuations and future rate expectations. With the S&P 500 recently experiencing a downturn after several weeks of gains, identifying stocks that may be trading below their intrinsic value becomes increasingly relevant for those seeking potential opportunities amidst market fluctuations. In such an environment, a good stock is often characterized by its resilience to broader market pressures and its potential for growth despite current undervaluations.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Trimegah Bangun Persada (IDX:NCKL) | IDR890.00 | IDR1777.58 | 49.9% |

| Provident Financial Services (NYSE:PFS) | US$19.03 | US$37.92 | 49.8% |

| Western Alliance Bancorporation (NYSE:WAL) | US$84.27 | US$168.24 | 49.9% |

| California Resources (NYSE:CRC) | US$52.32 | US$104.35 | 49.9% |

| Geovis TechnologyLtd (SHSE:688568) | CN¥41.40 | CN¥81.05 | 48.9% |

| Beyout Investment Group Holding Company - K.S.C. (Holding) (KWSE:BEYOUT) | KWD0.395 | KWD0.79 | 49.9% |

| Acerinox (BME:ACX) | €8.52 | €16.98 | 49.8% |

| Enento Group Oyj (HLSE:ENENTO) | €18.40 | €36.57 | 49.7% |

| ChromaDex (NasdaqCM:CDXC) | US$3.58 | US$7.15 | 49.9% |

| Fine Foods & Pharmaceuticals N.T.M (BIT:FF) | €8.36 | €16.70 | 49.9% |

Let's uncover some gems from our specialized screener.

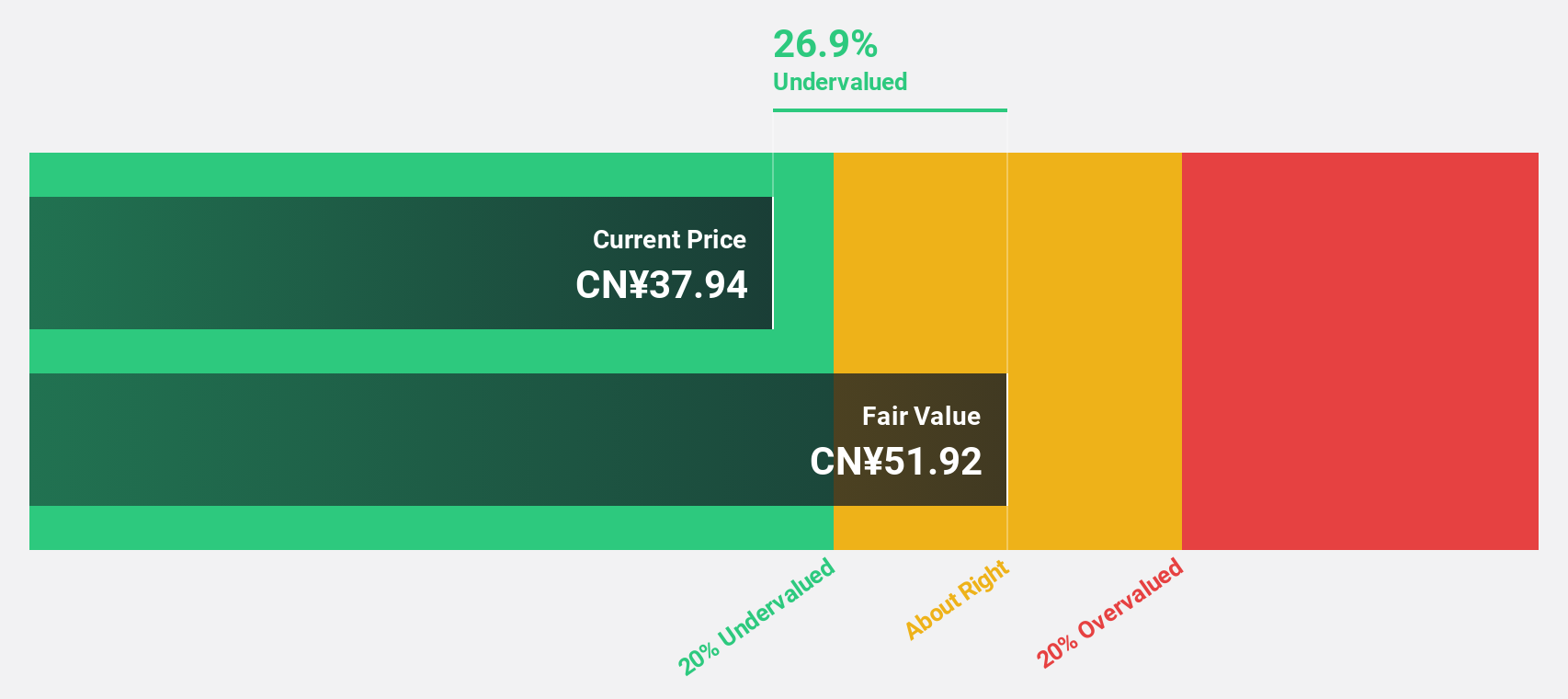

SKSHU PaintLtd (SHSE:603737)

Overview: SKSHU Paint Co., Ltd. operates under the 3trees brand, producing and selling paints, coatings, and building materials in China with a market cap of CN¥22.40 billion.

Operations: The company generates revenue from its segments, including paints, coatings, and building materials under the 3trees brand in China.

Estimated Discount To Fair Value: 19.3%

SKSHU Paint Ltd. reported a decline in net income to CNY 410.34 million for the nine months ended September 30, 2024, despite sales of CNY 9.15 billion. The stock trades at CN¥44.6, below its fair value estimate of CN¥55.28, indicating potential undervaluation based on cash flows. However, profit margins have decreased significantly from last year and the company carries a high level of debt with earnings impacted by large one-off items.

- Our earnings growth report unveils the potential for significant increases in SKSHU PaintLtd's future results.

- Click to explore a detailed breakdown of our findings in SKSHU PaintLtd's balance sheet health report.

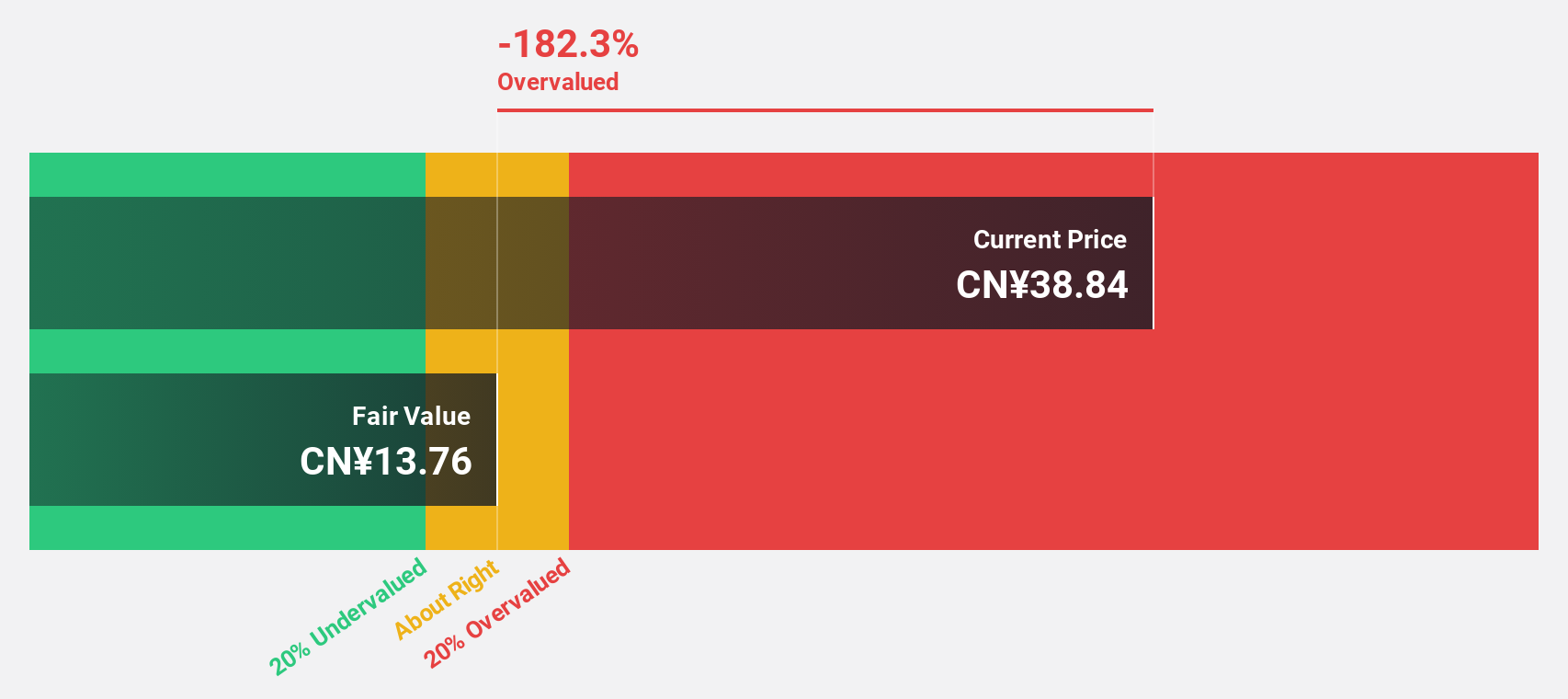

AVIC Jonhon Optronic TechnologyLtd (SZSE:002179)

Overview: AVIC Jonhon Optronic Technology Co., Ltd. focuses on the research and development of optical, electrical, and fluid connection technologies and equipment in China, with a market cap of CN¥94.87 billion.

Operations: Revenue segments for SZSE:002179 include optical connection technology and equipment at CN¥5.23 billion, electrical connection technology and equipment at CN¥3.47 billion, and fluid connection technology and equipment at CN¥1.89 billion.

Estimated Discount To Fair Value: 19.3%

AVIC Jonhon Optronic Technology Ltd. reported a decline in net income to CNY 2.51 billion for the nine months ended September 30, 2024, with sales of CNY 14.10 billion. Trading at CN¥44.15, below its fair value estimate of CN¥54.69, it presents potential undervaluation based on cash flows despite lower revenue and earnings compared to last year. Forecasts show robust revenue growth of over 21% annually, though earnings growth is slightly below market expectations.

- Our growth report here indicates AVIC Jonhon Optronic TechnologyLtd may be poised for an improving outlook.

- Click here to discover the nuances of AVIC Jonhon Optronic TechnologyLtd with our detailed financial health report.

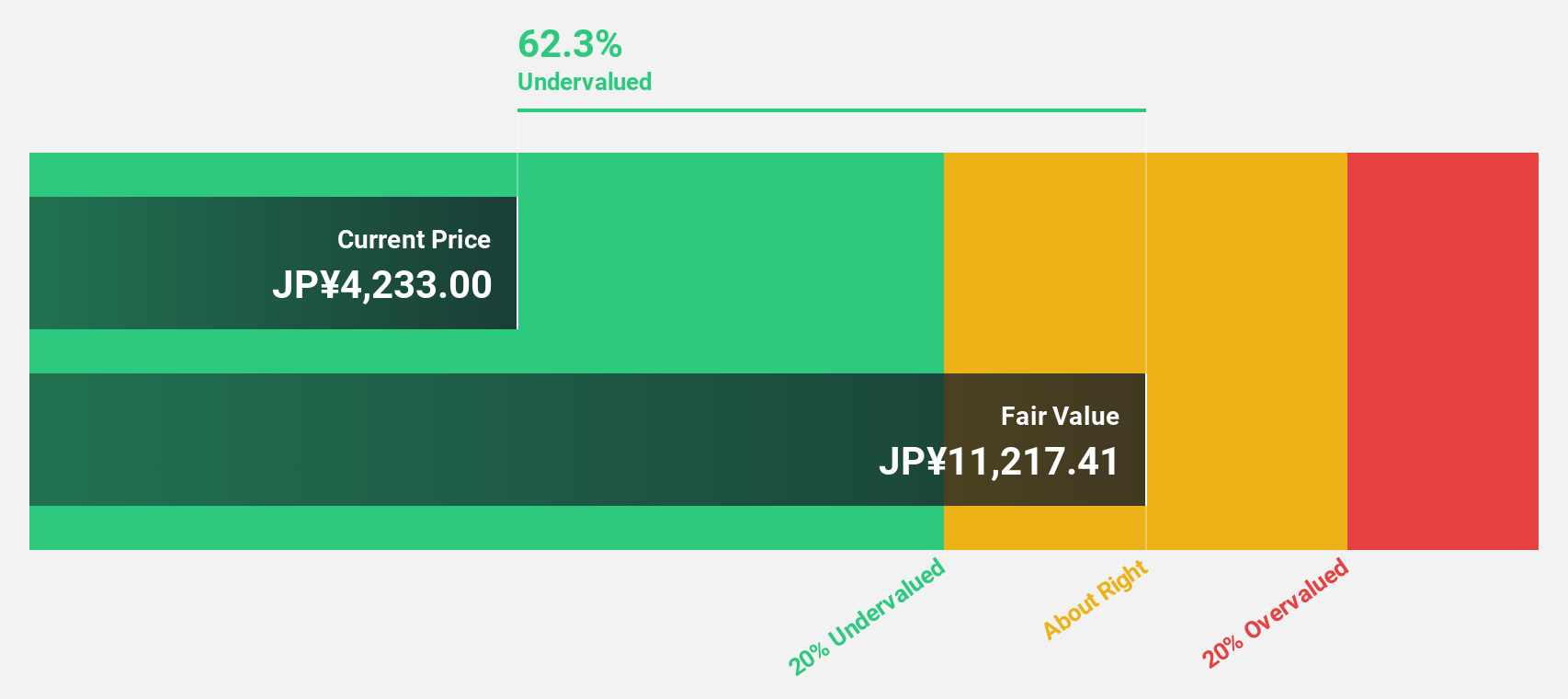

AGC (TSE:5201)

Overview: AGC Inc. is a global manufacturer and seller of glass, automotive, electronics, chemicals, and ceramics with a market cap of approximately ¥993.85 billion.

Operations: The company's revenue segments include Chemicals at ¥581.78 billion, Automotive at ¥510.88 billion, Electronics at ¥340.54 billion, Life Science at ¥122.40 billion, and Architectural Glass at ¥461.20 billion.

Estimated Discount To Fair Value: 42.2%

AGC Inc. trades at ¥4,702, significantly below its estimated fair value of ¥8,134.68, suggesting potential undervaluation based on cash flows. Despite forecasted annual earnings growth of over 68%, revenue is expected to grow modestly at 4.3% annually. Recent product launches in high-speed communication materials and expansion in semiconductor solutions highlight strategic growth initiatives amid challenges like lowered financial guidance due to European economic slowdown and biopharmaceutical sales decline.

- The analysis detailed in our AGC growth report hints at robust future financial performance.

- Unlock comprehensive insights into our analysis of AGC stock in this financial health report.

Where To Now?

- Dive into all 959 of the Undervalued Stocks Based On Cash Flows we have identified here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5201

AGC

Manufactures and sells glass, electronics, chemicals, automotive, and ceramics worldwide.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor