- China

- /

- Tech Hardware

- /

- SZSE:002152

GRG Banking Equipment Co., Ltd.'s (SZSE:002152) 25% Share Price Surge Not Quite Adding Up

Those holding GRG Banking Equipment Co., Ltd. (SZSE:002152) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Unfortunately, despite the strong performance over the last month, the full year gain of 5.7% isn't as attractive.

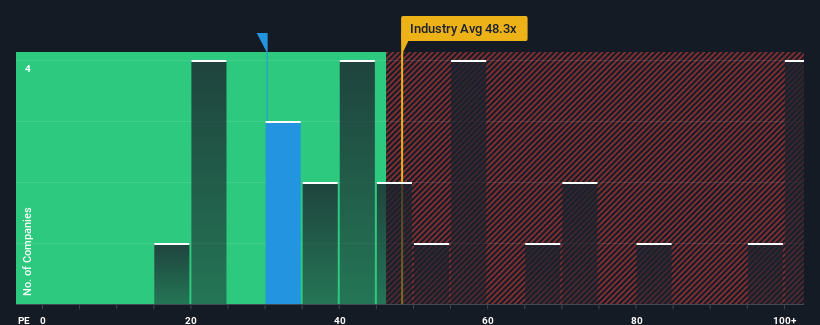

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about GRG Banking Equipment's P/E ratio of 30.1x, since the median price-to-earnings (or "P/E") ratio in China is also close to 30x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

With its earnings growth in positive territory compared to the declining earnings of most other companies, GRG Banking Equipment has been doing quite well of late. One possibility is that the P/E is moderate because investors think the company's earnings will be less resilient moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for GRG Banking Equipment

Is There Some Growth For GRG Banking Equipment?

In order to justify its P/E ratio, GRG Banking Equipment would need to produce growth that's similar to the market.

Retrospectively, the last year delivered an exceptional 18% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 36% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 17% as estimated by the three analysts watching the company. With the market predicted to deliver 41% growth , the company is positioned for a weaker earnings result.

In light of this, it's curious that GRG Banking Equipment's P/E sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On GRG Banking Equipment's P/E

GRG Banking Equipment's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of GRG Banking Equipment's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

You always need to take note of risks, for example - GRG Banking Equipment has 1 warning sign we think you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002152

GRG Banking Equipment

Provides artificial intelligence solutions for financial self-service industry in China and internationally.

Excellent balance sheet average dividend payer.