Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SHSE:600563

Little Excitement Around Xiamen Faratronic Co., Ltd.'s (SHSE:600563) Earnings

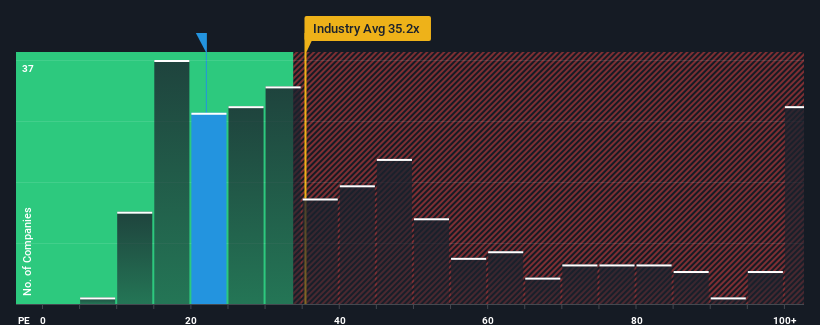

With a price-to-earnings (or "P/E") ratio of 21.9x Xiamen Faratronic Co., Ltd. (SHSE:600563) may be sending bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 29x and even P/E's higher than 53x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Xiamen Faratronic certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for Xiamen Faratronic

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Xiamen Faratronic's to be considered reasonable.

Retrospectively, the last year delivered a decent 6.3% gain to the company's bottom line. Pleasingly, EPS has also lifted 98% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the nine analysts covering the company suggest earnings should grow by 27% over the next year. With the market predicted to deliver 41% growth , the company is positioned for a weaker earnings result.

With this information, we can see why Xiamen Faratronic is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Xiamen Faratronic's P/E?

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Xiamen Faratronic's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for Xiamen Faratronic with six simple checks.

If you're unsure about the strength of Xiamen Faratronic's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600563

Xiamen Faratronic

Manufactures and sells film capacitors and metallized coating materials in China and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets