- China

- /

- Semiconductors

- /

- SZSE:300708

Focus Lightings Tech's (SZSE:300708) Promising Earnings May Rest On Soft Foundations

Unsurprisingly, Focus Lightings Tech Co., Ltd.'s (SZSE:300708) stock price was strong on the back of its healthy earnings report. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

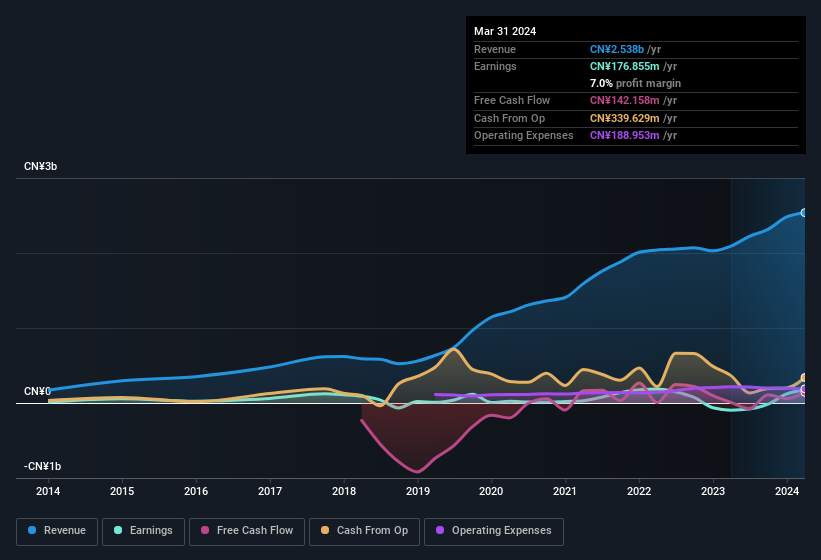

See our latest analysis for Focus Lightings Tech

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Focus Lightings Tech issued 18% more new shares over the last year. That means its earnings are split among a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Focus Lightings Tech's historical EPS growth by clicking on this link.

A Look At The Impact Of Focus Lightings Tech's Dilution On Its Earnings Per Share (EPS)

We don't have any data on the company's profits from three years ago. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. What we do know is that while it's great to see a profit over the last twelve months, that profit would have been better, on a per share basis, if the company hadn't needed to issue shares. So you can see that the dilution has had a bit of an impact on shareholders.

If Focus Lightings Tech's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Power Of Non-Operating Revenue

Most companies divide classify their revenue as either 'operating revenue', which comes from normal operations, and other revenue, which could include government grants, for example. Generally speaking, operating revenue is a more reliable guide to the sustainable revenue generating capacity of the business. However, we note that when non-operating revenue increases suddenly, it will sometimes generate an unsustainable boost to profit. As well as the aforementioned dilution, Focus Lightings Tech saw a spike in non-operating revenue, over the last year. Indeed, its non-operating revenue rose from CN¥880.7m last year to CN¥1.22b this year. The high levels of non-operating revenue are problematic because if (and when) they do not repeat, then overall revenue (and profitability) of the firm will fall. In order to better understand a company's profit result, it can sometimes help to consider whether the result would be very different without a sudden increase in non-operating revenue.

Our Take On Focus Lightings Tech's Profit Performance

In its last report Focus Lightings Tech benefitted from a spike in non-operating revenue which may make its top line look unsustainably good, and even flow down to its profit. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. For the reasons mentioned above, we think that a perfunctory glance at Focus Lightings Tech's statutory profits might make it look better than it really is on an underlying level. If you'd like to know more about Focus Lightings Tech as a business, it's important to be aware of any risks it's facing. While conducting our analysis, we found that Focus Lightings Tech has 2 warning signs and it would be unwise to ignore these.

Our examination of Focus Lightings Tech has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300708

Focus Lightings Tech

Engages in the research and development, production, and sale of compound optoelectronic semiconductor materials in China and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Community Narratives