Suzhou Novosense Microelectronics And 2 Insider Picks For High Growth Potential

Reviewed by Simply Wall St

In a week marked by volatility and competitive pressures in the AI sector, global markets have experienced mixed performances, with U.S. stocks facing challenges from new technological developments and tariff uncertainties. Amidst these fluctuations, identifying growth companies with substantial insider ownership can be crucial for investors seeking potential resilience and alignment of interests in uncertain times.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 25.7% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.4% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 86% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Let's review some notable picks from our screened stocks.

Suzhou Novosense Microelectronics (SHSE:688052)

Simply Wall St Growth Rating: ★★★★★☆

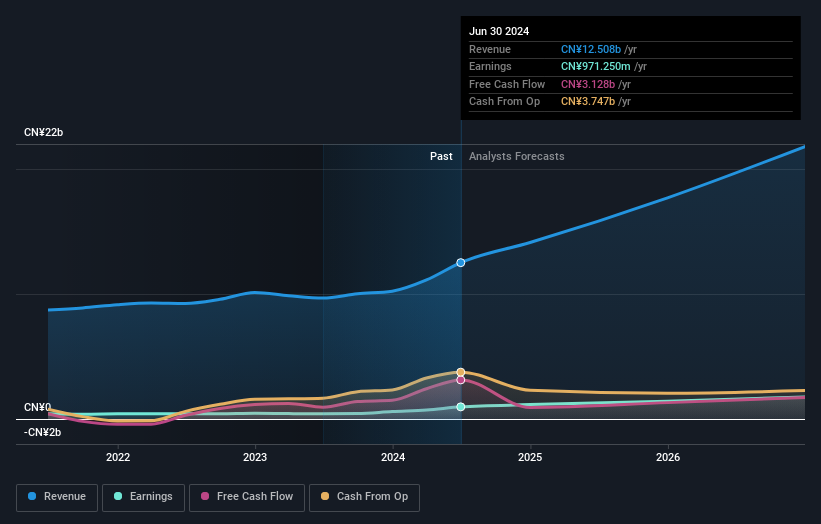

Overview: Suzhou Novosense Microelectronics Co., Ltd. operates in the microelectronics industry, focusing on developing and manufacturing semiconductor products, with a market cap of CN¥19.14 billion.

Operations: Unfortunately, the revenue segment details for Suzhou Novosense Microelectronics are missing from the provided text. Therefore, I can't provide a summary of its revenue segments.

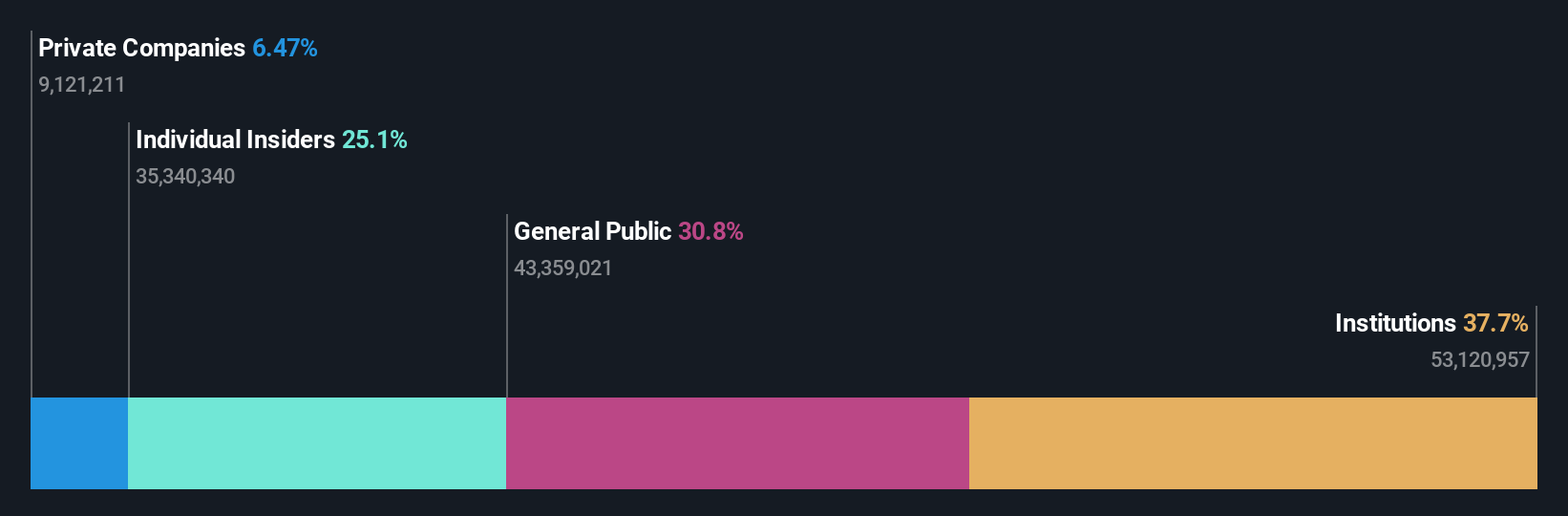

Insider Ownership: 25.1%

Earnings Growth Forecast: 121.1% p.a.

Suzhou Novosense Microelectronics is forecast to experience significant growth, with revenue expected to increase by 30.3% annually, outpacing the Chinese market's average of 13.5%. The company is projected to become profitable within three years, with earnings growing at an impressive rate of over 121% per year. Despite these promising growth prospects, insider trading activity has been minimal over the past three months, indicating stable insider sentiment rather than aggressive buying or selling.

- Click to explore a detailed breakdown of our findings in Suzhou Novosense Microelectronics' earnings growth report.

- Upon reviewing our latest valuation report, Suzhou Novosense Microelectronics' share price might be too optimistic.

Jiangsu Leadmicro Nano-Equipment Technology (SHSE:688147)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Leadmicro Nano-Equipment Technology Ltd designs, manufactures, and services film deposition and etching equipment, with a market cap of CN¥11.33 billion.

Operations: The company's revenue is primarily derived from its equipment manufacturing segment, totaling CN¥2.20 billion.

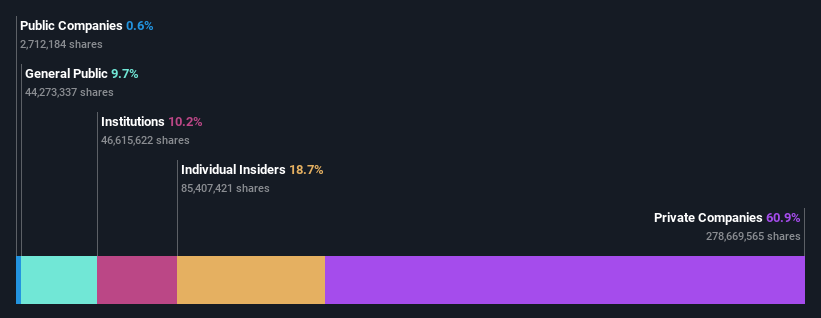

Insider Ownership: 18.7%

Earnings Growth Forecast: 37% p.a.

Jiangsu Leadmicro Nano-Equipment Technology is set for robust growth, with earnings projected to increase by 37% annually and revenue by 27.1%, both surpassing the Chinese market averages. The company recently announced a CNY 80 million share buyback program to enhance employee incentives and support long-term development, indicating confidence in its future prospects. Despite high volatility in its share price, the company's Price-To-Earnings ratio remains attractive compared to industry standards.

- Click here to discover the nuances of Jiangsu Leadmicro Nano-Equipment Technology with our detailed analytical future growth report.

- Our valuation report unveils the possibility Jiangsu Leadmicro Nano-Equipment Technology's shares may be trading at a premium.

Ninebot (SHSE:689009)

Simply Wall St Growth Rating: ★★★★★★

Overview: Ninebot Limited designs, develops, produces, sells, and services transportation and robot products globally with a market cap of CN¥35.78 billion.

Operations: Revenue Segments (in millions of CN¥):

Insider Ownership: 15.4%

Earnings Growth Forecast: 28.5% p.a.

Ninebot is positioned for strong growth, with revenue expected to rise 24.8% annually, outpacing the Chinese market average. Its earnings are projected to grow significantly at 28.5% per year, also above market expectations. The company's Price-To-Earnings ratio of 31.6x is below the CN market average, suggesting potential value despite high earnings growth forecasts and a forecasted Return on Equity of 23.4%. No recent insider trading activity has been reported.

- Get an in-depth perspective on Ninebot's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Ninebot's share price might be on the expensive side.

Where To Now?

- Access the full spectrum of 1478 Fast Growing Companies With High Insider Ownership by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Ninebot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:689009

Ninebot

Engages in the design, research and development, production, sale, and servicing of transportation and robot products worldwide.

Exceptional growth potential with flawless balance sheet.

Market Insights

Community Narratives