Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1109

3 Noteworthy Dividend Stocks Yielding Up To 6.3%

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with tariff uncertainties and mixed economic signals, investors are seeking stability amid the volatility. With U.S. job growth falling short of expectations and manufacturing showing signs of recovery, dividend stocks can offer a reliable income stream in uncertain times. In this context, selecting stocks with strong dividend yields can be a prudent strategy to balance risk and reward within an investment portfolio.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.88% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.01% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.98% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.38% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.12% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.04% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.31% | ★★★★★★ |

| DoshishaLtd (TSE:7483) | 3.82% | ★★★★★★ |

| FALCO HOLDINGS (TSE:4671) | 6.51% | ★★★★★★ |

| Archer-Daniels-Midland (NYSE:ADM) | 4.46% | ★★★★★☆ |

Click here to see the full list of 1973 stocks from our Top Dividend Stocks screener.

We'll examine a selection from our screener results.

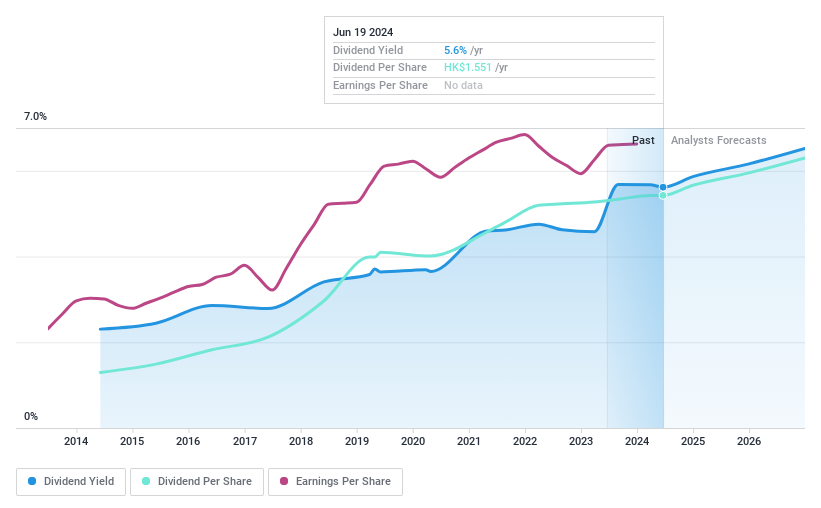

China Resources Land (SEHK:1109)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: China Resources Land Limited is an investment holding company involved in the investment, development, management, and sale of properties in the People’s Republic of China with a market cap of approximately HK$173.28 billion.

Operations: China Resources Land's revenue segments include CN¥239.18 billion from the Development Property Business, CN¥23.92 billion from the Investment Property Business, CN¥15.66 billion from the Eco-system Elementary Business, and CN¥14.74 billion from the Asset-light Management Business.

Dividend Yield: 6.3%

China Resources Land offers a mixed profile for dividend investors. The stock trades at a significant discount to its estimated fair value, suggesting potential upside. However, its dividends are not well covered by cash flows, indicating potential sustainability concerns despite being well covered by earnings. Dividends have been stable and growing over the past decade but yield remains lower than top-tier peers in Hong Kong. Recent debt financing may impact financial flexibility moving forward.

- Click here to discover the nuances of China Resources Land with our detailed analytical dividend report.

- The valuation report we've compiled suggests that China Resources Land's current price could be quite moderate.

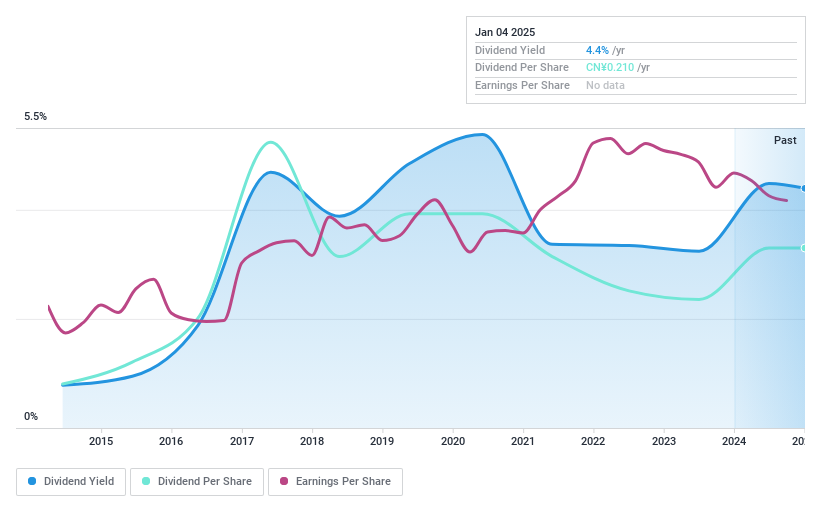

Wuchan Zhongda GroupLtd (SHSE:600704)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Wuchan Zhongda Group Co., Ltd., along with its subsidiaries, offers bulk commodity supply chain integration services both in China and internationally, with a market capitalization of approximately CN¥26.17 billion.

Operations: Wuchan Zhongda Group Co., Ltd. generates its revenue through the provision of bulk commodity supply chain integration services across domestic and international markets.

Dividend Yield: 4.2%

Wuchan Zhongda Group's dividend yield of 4.17% ranks in the top 25% of CN market payers, but its dividends are not covered by free cash flows, raising sustainability concerns. Despite a low payout ratio of 34.6%, past dividend payments have been volatile and unreliable, with significant drops over the decade. The recent share buyback completed for CNY 111.53 million may signal confidence but does not address underlying cash flow challenges impacting dividend stability.

- Dive into the specifics of Wuchan Zhongda GroupLtd here with our thorough dividend report.

- Our comprehensive valuation report raises the possibility that Wuchan Zhongda GroupLtd is priced higher than what may be justified by its financials.

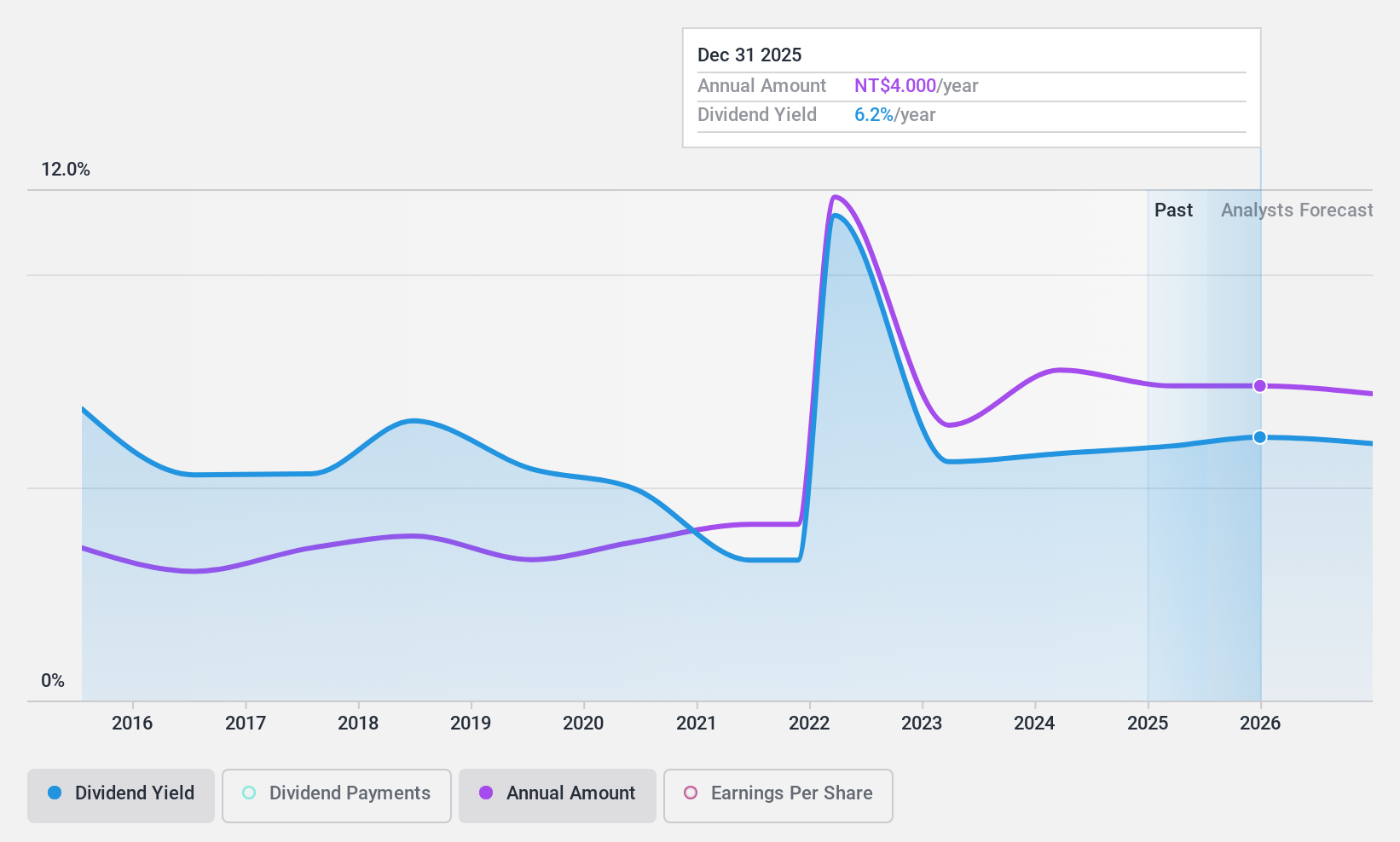

Tung Ho Steel Enterprise (TWSE:2006)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Tung Ho Steel Enterprise Corporation, along with its subsidiaries, engages in the production and sale of steel products in Taiwan and has a market capitalization of NT$52.87 billion.

Operations: Tung Ho Steel Enterprise Corporation generates revenue primarily from its Steel Department, contributing NT$55.50 billion, and its Steel Structure Department, which adds NT$13.85 billion.

Dividend Yield: 5.8%

Tung Ho Steel Enterprise's dividend yield of 5.8% places it among the top 25% in Taiwan, supported by a reasonable payout ratio of 65.4% and cash payout ratio of 53.6%, indicating coverage by earnings and cash flows. However, the dividends have been volatile over the past decade, with inconsistent growth patterns despite an increase over ten years. The stock trades at a value below its estimated fair value but faces potential earnings declines in coming years.

- Delve into the full analysis dividend report here for a deeper understanding of Tung Ho Steel Enterprise.

- Our valuation report unveils the possibility Tung Ho Steel Enterprise's shares may be trading at a discount.

Turning Ideas Into Actions

- Click here to access our complete index of 1973 Top Dividend Stocks.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1109

China Resources Land

An investment holding company, engages in the investment, development, management, and sale of properties in the People’s Republic of China.

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.2% undervalued

TO

Community Contributor