Are Robust Financials Driving The Recent Rally In Yili Chuanning Biotechnology Co.,Ltd.'s (SZSE:301301) Stock?

Yili Chuanning BiotechnologyLtd's (SZSE:301301) stock is up by a considerable 22% over the past three months. Given the company's impressive performance, we decided to study its financial indicators more closely as a company's financial health over the long-term usually dictates market outcomes. Specifically, we decided to study Yili Chuanning BiotechnologyLtd's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

View our latest analysis for Yili Chuanning BiotechnologyLtd

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Yili Chuanning BiotechnologyLtd is:

18% = CN¥1.4b ÷ CN¥7.6b (Based on the trailing twelve months to September 2024).

The 'return' is the yearly profit. One way to conceptualize this is that for each CN¥1 of shareholders' capital it has, the company made CN¥0.18 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Yili Chuanning BiotechnologyLtd's Earnings Growth And 18% ROE

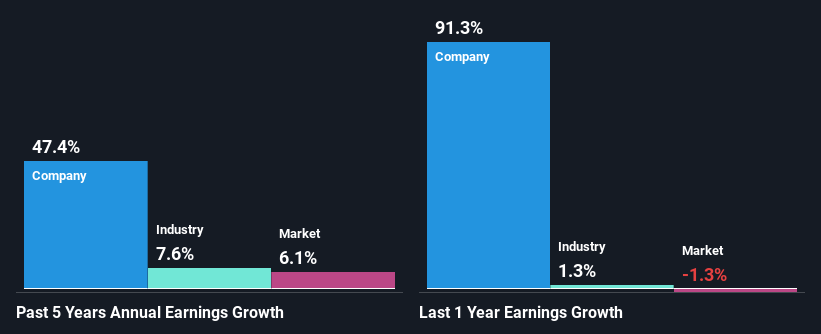

To start with, Yili Chuanning BiotechnologyLtd's ROE looks acceptable. Especially when compared to the industry average of 5.9% the company's ROE looks pretty impressive. This certainly adds some context to Yili Chuanning BiotechnologyLtd's exceptional 47% net income growth seen over the past five years. We believe that there might also be other aspects that are positively influencing the company's earnings growth. Such as - high earnings retention or an efficient management in place.

As a next step, we compared Yili Chuanning BiotechnologyLtd's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 7.6%.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Yili Chuanning BiotechnologyLtd's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Yili Chuanning BiotechnologyLtd Using Its Retained Earnings Effectively?

Yili Chuanning BiotechnologyLtd has a three-year median payout ratio of 39% (where it is retaining 61% of its income) which is not too low or not too high. This suggests that its dividend is well covered, and given the high growth we discussed above, it looks like Yili Chuanning BiotechnologyLtd is reinvesting its earnings efficiently.

While Yili Chuanning BiotechnologyLtd has seen growth in its earnings, it only recently started to pay a dividend. It is most likely that the company decided to impress new and existing shareholders with a dividend. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 49% over the next three years. Regardless, the ROE is not expected to change much for the company despite the higher expected payout ratio.

Conclusion

Overall, we are quite pleased with Yili Chuanning BiotechnologyLtd's performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you're looking to trade Yili Chuanning BiotechnologyLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301301

Yili Chuanning BiotechnologyLtd

Engages in the research and development, and industrialization of biological fermentation technology in China.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Community Narratives