Advertisement

Zhejiang Yatai Pharmaceutical Co., Ltd.'s (SZSE:002370) Popularity With Investors Under Threat As Stock Sinks 25%

Zhejiang Yatai Pharmaceutical Co., Ltd. (SZSE:002370) shareholders won't be pleased to see that the share price has had a very rough month, dropping 25% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 29% share price drop.

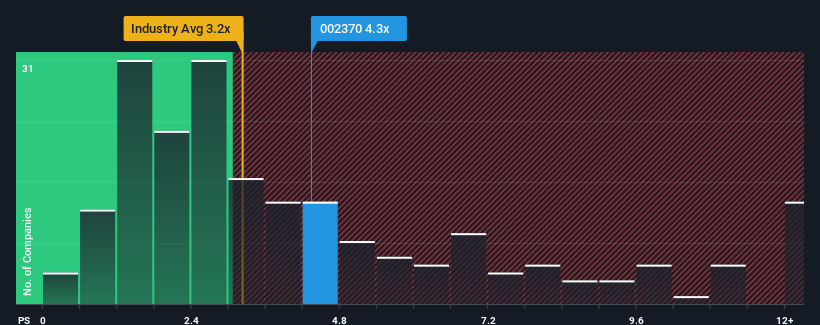

Although its price has dipped substantially, when almost half of the companies in China's Pharmaceuticals industry have price-to-sales ratios (or "P/S") below 3.2x, you may still consider Zhejiang Yatai Pharmaceutical as a stock probably not worth researching with its 4.3x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Zhejiang Yatai Pharmaceutical

How Zhejiang Yatai Pharmaceutical Has Been Performing

As an illustration, revenue has deteriorated at Zhejiang Yatai Pharmaceutical over the last year, which is not ideal at all. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Zhejiang Yatai Pharmaceutical's earnings, revenue and cash flow.How Is Zhejiang Yatai Pharmaceutical's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Zhejiang Yatai Pharmaceutical's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 3.5%. That put a dampener on the good run it was having over the longer-term as its three-year revenue growth is still a noteworthy 14% in total. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

This is in contrast to the rest of the industry, which is expected to grow by 178% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we find it concerning that Zhejiang Yatai Pharmaceutical is trading at a P/S higher than the industry. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Key Takeaway

Despite the recent share price weakness, Zhejiang Yatai Pharmaceutical's P/S remains higher than most other companies in the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of Zhejiang Yatai Pharmaceutical revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

Having said that, be aware Zhejiang Yatai Pharmaceutical is showing 1 warning sign in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Zhejiang Yatai Pharmaceutical, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Yatai Pharmaceutical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002370

Zhejiang Yatai Pharmaceutical

Researches, produces, sells, and exports pharmaceutical products in China and internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor