Is Weakness In China Resources Sanjiu Medical & Pharmaceutical Co., Ltd. (SZSE:000999) Stock A Sign That The Market Could be Wrong Given Its Strong Financial Prospects?

With its stock down 8.4% over the past three months, it is easy to disregard China Resources Sanjiu Medical & Pharmaceutical (SZSE:000999). However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. In this article, we decided to focus on China Resources Sanjiu Medical & Pharmaceutical's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for China Resources Sanjiu Medical & Pharmaceutical

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for China Resources Sanjiu Medical & Pharmaceutical is:

14% = CN¥3.7b ÷ CN¥26b (Based on the trailing twelve months to September 2024).

The 'return' is the amount earned after tax over the last twelve months. That means that for every CN¥1 worth of shareholders' equity, the company generated CN¥0.14 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

China Resources Sanjiu Medical & Pharmaceutical's Earnings Growth And 14% ROE

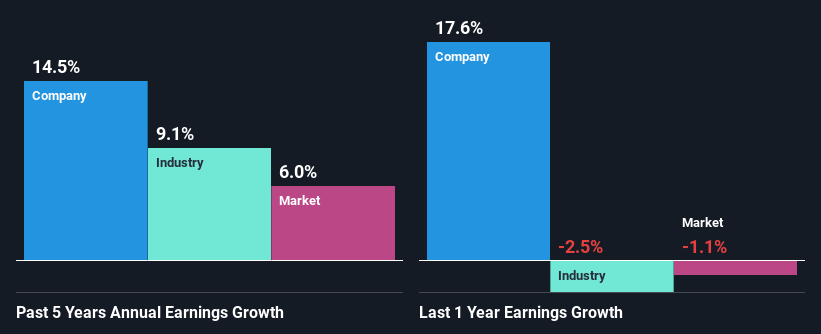

At first glance, China Resources Sanjiu Medical & Pharmaceutical seems to have a decent ROE. On comparing with the average industry ROE of 7.7% the company's ROE looks pretty remarkable. This probably laid the ground for China Resources Sanjiu Medical & Pharmaceutical's moderate 14% net income growth seen over the past five years.

As a next step, we compared China Resources Sanjiu Medical & Pharmaceutical's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 9.1%.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for 000999? You can find out in our latest intrinsic value infographic research report.

Is China Resources Sanjiu Medical & Pharmaceutical Making Efficient Use Of Its Profits?

With a three-year median payout ratio of 38% (implying that the company retains 62% of its profits), it seems that China Resources Sanjiu Medical & Pharmaceutical is reinvesting efficiently in a way that it sees respectable amount growth in its earnings and pays a dividend that's well covered.

Additionally, China Resources Sanjiu Medical & Pharmaceutical has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 51% over the next three years. Still, forecasts suggest that China Resources Sanjiu Medical & Pharmaceutical's future ROE will rise to 18% even though the the company's payout ratio is expected to rise. We presume that there could some other characteristics of the business that could be driving the anticipated growth in the company's ROE.

Summary

Overall, we are quite pleased with China Resources Sanjiu Medical & Pharmaceutical's performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000999

China Resources Sanjiu Medical & Pharmaceutical

China Resources Sanjiu Medical & Pharmaceutical Co., Ltd.

Very undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives