Apeloa Pharmaceutical Co.,Ltd's (SZSE:000739) Share Price Boosted 26% But Its Business Prospects Need A Lift Too

Apeloa Pharmaceutical Co.,Ltd (SZSE:000739) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 20% over that time.

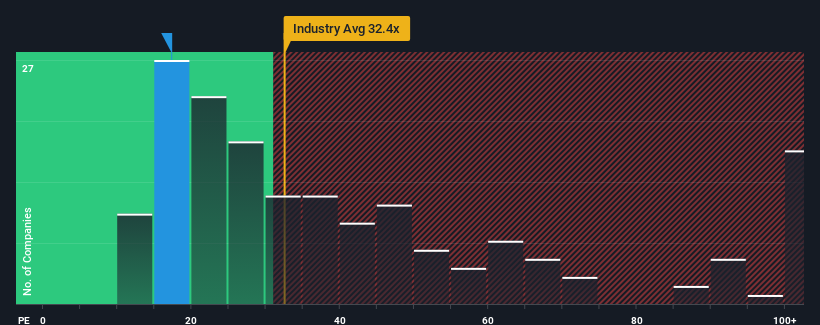

In spite of the firm bounce in price, Apeloa PharmaceuticalLtd's price-to-earnings (or "P/E") ratio of 17.3x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 33x and even P/E's above 63x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Apeloa PharmaceuticalLtd could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for Apeloa PharmaceuticalLtd

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Apeloa PharmaceuticalLtd would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 1.3% decrease to the company's bottom line. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 21% in total. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Shifting to the future, estimates from the seven analysts covering the company suggest earnings should grow by 16% each year over the next three years. Meanwhile, the rest of the market is forecast to expand by 26% per annum, which is noticeably more attractive.

With this information, we can see why Apeloa PharmaceuticalLtd is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Apeloa PharmaceuticalLtd's P/E

Apeloa PharmaceuticalLtd's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Apeloa PharmaceuticalLtd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 1 warning sign for Apeloa PharmaceuticalLtd you should be aware of.

If you're unsure about the strength of Apeloa PharmaceuticalLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000739

Apeloa PharmaceuticalLtd

Provides raw materials and intermediates to various pharmaceutical factories in the People’s Republic of China and internationally.

Very undervalued with excellent balance sheet and pays a dividend.