As global markets continue to react positively to recent political developments and AI enthusiasm, major indexes like the S&P 500 have reached new highs, with growth stocks outperforming value shares for the first time this year. In this optimistic environment, identifying growth companies with strong insider ownership can be a strategic approach, as high insider support often signals confidence in the company's future prospects and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 20.5% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.6% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.9% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Pharma Mar (BME:PHM) | 11.9% | 55.1% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Underneath we present a selection of stocks filtered out by our screen.

Maharah for Human Resources (SASE:1831)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Maharah for Human Resources Company offers manpower services to both public and private sectors in Saudi Arabia and the United Arab Emirates, with a market cap of SAR2.99 billion.

Operations: The company's revenue is primarily derived from its Corporate segment at SAR1.54 billion, followed by the Individual segment at SAR433.54 million, and Facility Management at SAR113.02 million.

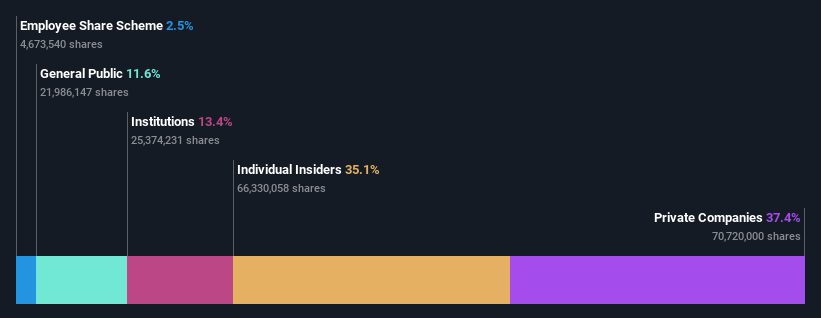

Insider Ownership: 26.3%

Maharah for Human Resources demonstrates growth potential with forecasted earnings growth of 15.2% annually, outpacing the South African market's 6% rate. Revenue is also expected to grow at 10.9% per year. However, its dividend yield of 2.18% isn't well supported by free cash flow, and interest payments are not adequately covered by earnings. Recent quarterly results show sales increased to SAR 558.4 million, but net income remained stable at SAR 24.37 million year-over-year.

- Unlock comprehensive insights into our analysis of Maharah for Human Resources stock in this growth report.

- The analysis detailed in our Maharah for Human Resources valuation report hints at an inflated share price compared to its estimated value.

Jiangsu Jibeier Pharmaceutical (SHSE:688566)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jiangsu Jibeier Pharmaceutical Co., Ltd. is a pharmaceutical company involved in the research, development, production, and sale of chemical pharmaceutical preparations and Chinese medicine, with a market cap of CN¥4.44 billion.

Operations: The company's revenue primarily comes from its pharmaceutical manufacturing segment, totaling CN¥887.17 million.

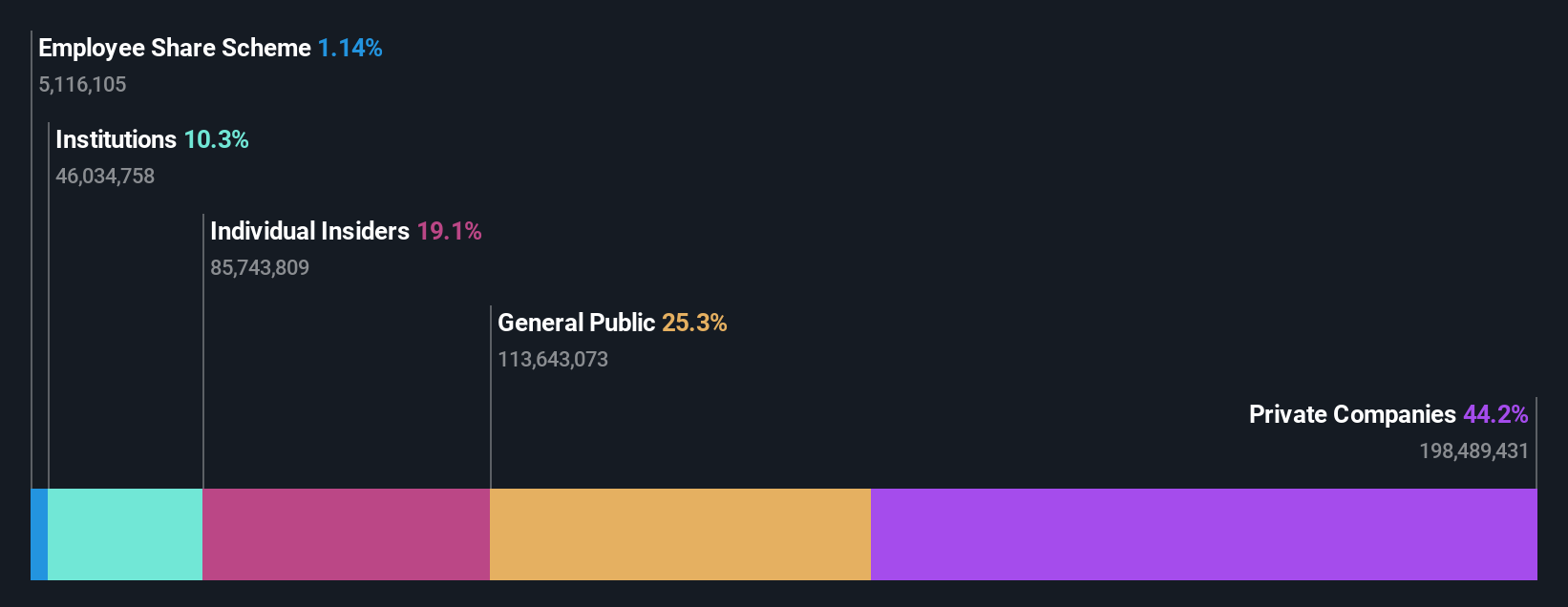

Insider Ownership: 33.7%

Jiangsu Jibeier Pharmaceutical is positioned for substantial growth, with revenue projected to increase by 23.2% annually, outpacing the Chinese market's 13.3% rate. Despite a low forecasted return on equity of 14.5%, its earnings are expected to grow significantly at 23.75% per year, though slightly below the market average of 25%. Trading at a price-to-earnings ratio of 18.6x, it offers good value compared to peers and industry standards.

- Click to explore a detailed breakdown of our findings in Jiangsu Jibeier Pharmaceutical's earnings growth report.

- Our valuation report unveils the possibility Jiangsu Jibeier Pharmaceutical's shares may be trading at a discount.

ApicHope Pharmaceutical Group (SZSE:300723)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ApicHope Pharmaceutical Group Co., Ltd. operates in the research and development, production, and sale of pharmaceutical drugs with a market cap of CN¥7.11 billion.

Operations: Revenue Segments (in millions of CN¥):

Insider Ownership: 19.2%

ApicHope Pharmaceutical Group is expected to see revenue growth of 18% annually, surpassing the Chinese market's average but falling short of high-growth benchmarks. Earnings are projected to grow at a significant rate of 96.97% per year, with profitability anticipated within three years. Despite a volatile share price and low forecasted return on equity at 10.6%, the company remains financially challenged due to insufficient operating cash flow coverage for its debt obligations. Recent shareholder meetings focused on patent agreements and connected transactions indicate strategic moves for future growth.

- Dive into the specifics of ApicHope Pharmaceutical Group here with our thorough growth forecast report.

- According our valuation report, there's an indication that ApicHope Pharmaceutical Group's share price might be on the expensive side.

Next Steps

- Click through to start exploring the rest of the 1475 Fast Growing Companies With High Insider Ownership now.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688566

Jiangsu Jibeier Pharmaceutical

A pharmaceutical company, engages in the research, development, production, and sale of chemical pharmaceutical preparations, Chinese medicine, and drugs.

Excellent balance sheet with reasonable growth potential.

Market Insights

Community Narratives