- Japan

- /

- Aerospace & Defense

- /

- TSE:186A

3 Growth Companies With High Insider Ownership Growing Revenues At 43%

Reviewed by Simply Wall St

In the current landscape, global markets have shown mixed performances, with major U.S. stock indexes like the S&P 500 and Nasdaq Composite reaching record highs amid a rally in growth stocks, while geopolitical events and economic reports continue to influence investor sentiment. Amidst this backdrop of fluctuating indices and sector-specific gains, identifying growth companies with high insider ownership can be compelling for investors seeking alignment of interests between company insiders and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Medley (TSE:4480) | 34% | 31.7% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.4% | 110.9% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's review some notable picks from our screened stocks.

Angelalign Technology (SEHK:6699)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Angelalign Technology Inc. is an investment holding company that focuses on researching, developing, designing, manufacturing, and marketing clear aligner treatment solutions in the People's Republic of China with a market cap of HK$10.02 billion.

Operations: The company's revenue primarily comes from its Dental Equipment & Supplies segment, which generated CN¥1.72 billion.

Insider Ownership: 18.4%

Revenue Growth Forecast: 15.3% p.a.

Angelalign Technology is poised for robust growth, with earnings projected to increase by 67.04% annually, outpacing the Hong Kong market. Despite a decline in profit margins from 13.1% to 2.5%, the company trades slightly below its fair value estimate and analysts anticipate a 36.2% price rise. However, Return on Equity is expected to remain low at 6.5%. Revenue growth of 15.3% annually also surpasses market averages but remains under the high-growth threshold.

- Click here and access our complete growth analysis report to understand the dynamics of Angelalign Technology.

- Our valuation report unveils the possibility Angelalign Technology's shares may be trading at a discount.

BrightGene Bio-Medical Technology (SHSE:688166)

Simply Wall St Growth Rating: ★★★★★☆

Overview: BrightGene Bio-Medical Technology Co., Ltd. is a pharmaceutical company involved in the research, development, manufacture, and commercialization of pharmaceutical products in China, with a market cap of CN¥13.24 billion.

Operations: BrightGene Bio-Medical Technology Co., Ltd. generates its revenue through the research, development, manufacture, and commercialization of pharmaceutical products in China.

Insider Ownership: 32.2%

Revenue Growth Forecast: 26.5% p.a.

BrightGene Bio-Medical Technology is positioned for significant growth, with earnings expected to rise by 34.79% annually, surpassing the Chinese market's average. Despite a slight decline in net income to CNY 177.41 million and volatile share prices recently, the company trades at 41.5% below its estimated fair value. Revenue is forecasted to grow at 26.5% annually, outpacing market averages, although Return on Equity remains modest at a projected 10%.

- Click here to discover the nuances of BrightGene Bio-Medical Technology with our detailed analytical future growth report.

- The analysis detailed in our BrightGene Bio-Medical Technology valuation report hints at an inflated share price compared to its estimated value.

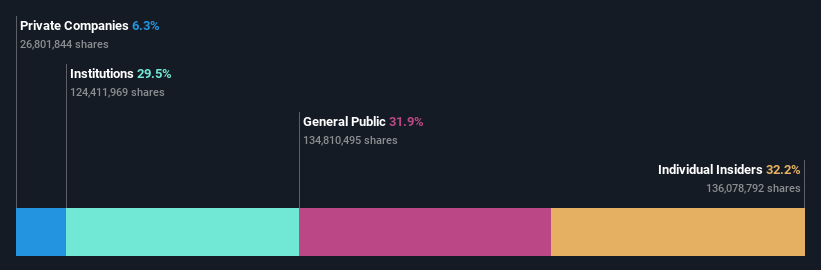

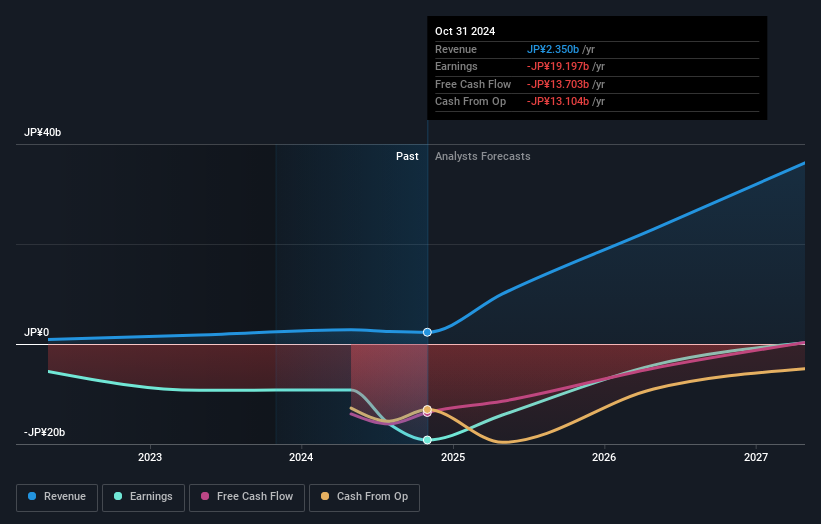

Astroscale Holdings (TSE:186A)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Astroscale Holdings Inc. offers on-orbit service solutions and has a market cap of ¥96.49 billion.

Operations: The company generates revenue from its In-Orbit Servicing Business, amounting to ¥2.51 billion.

Insider Ownership: 21.3%

Revenue Growth Forecast: 43% p.a.

Astroscale Holdings is poised for substantial growth, with revenue expected to increase by 43% annually, significantly outpacing the Japanese market average. Despite a highly volatile share price recently and a low projected Return on Equity of 6.6%, the company is forecasted to become profitable within three years. Recent news highlights a JPY 91 million government contract awarded to its subsidiary, supporting its growth trajectory without significant insider trading activity in recent months.

- Navigate through the intricacies of Astroscale Holdings with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Astroscale Holdings shares in the market.

Taking Advantage

- Delve into our full catalog of 1510 Fast Growing Companies With High Insider Ownership here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:186A

High growth potential with excellent balance sheet.