Some Qingdao Vland Biotech INC. (SHSE:603739) Shareholders Look For Exit As Shares Take 27% Pounding

Qingdao Vland Biotech INC. (SHSE:603739) shareholders won't be pleased to see that the share price has had a very rough month, dropping 27% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 21% share price drop.

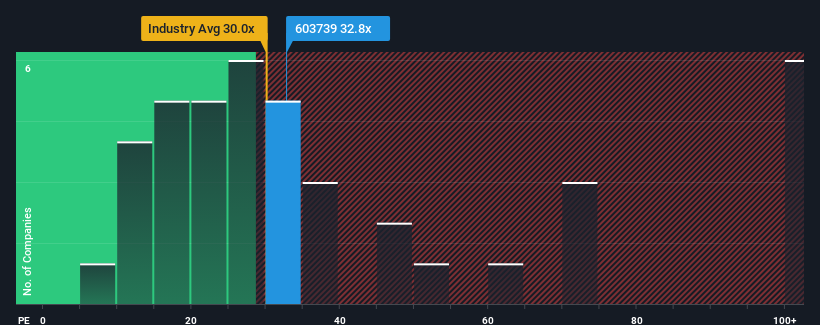

Even after such a large drop in price, Qingdao Vland Biotech's price-to-earnings (or "P/E") ratio of 32.8x might still make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 27x and even P/E's below 16x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Qingdao Vland Biotech certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It seems that many are expecting the company to continue defying the broader market adversity, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Qingdao Vland Biotech

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Qingdao Vland Biotech's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 34%. However, this wasn't enough as the latest three year period has seen a very unpleasant 37% drop in EPS in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 11% each year as estimated by the three analysts watching the company. With the market predicted to deliver 20% growth per year, the company is positioned for a weaker earnings result.

In light of this, it's alarming that Qingdao Vland Biotech's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

What We Can Learn From Qingdao Vland Biotech's P/E?

Qingdao Vland Biotech's P/E hasn't come down all the way after its stock plunged. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Qingdao Vland Biotech's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It is also worth noting that we have found 2 warning signs for Qingdao Vland Biotech that you need to take into consideration.

If these risks are making you reconsider your opinion on Qingdao Vland Biotech, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao Vland Biotech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603739

Qingdao Vland Biotech

Engages in the research and development, production, and sale of enzyme preparations, microecological preparations, and animal health products in China and internationally.

Excellent balance sheet and fair value.