Nanjing King-Friend Biochemical Pharmaceutical Co.,Ltd.'s (SHSE:603707) Popularity With Investors Is Under Threat From Overpricing

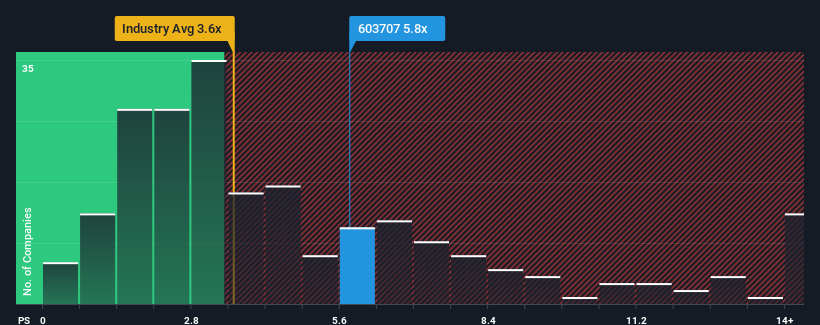

When you see that almost half of the companies in the Pharmaceuticals industry in China have price-to-sales ratios (or "P/S") below 3.6x, Nanjing King-Friend Biochemical Pharmaceutical Co.,Ltd. (SHSE:603707) looks to be giving off strong sell signals with its 5.8x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Nanjing King-Friend Biochemical PharmaceuticalLtd

How Has Nanjing King-Friend Biochemical PharmaceuticalLtd Performed Recently?

Nanjing King-Friend Biochemical PharmaceuticalLtd hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. It might be that many expect the dour revenue performance to recover substantially, which has kept the P/S from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Nanjing King-Friend Biochemical PharmaceuticalLtd.How Is Nanjing King-Friend Biochemical PharmaceuticalLtd's Revenue Growth Trending?

In order to justify its P/S ratio, Nanjing King-Friend Biochemical PharmaceuticalLtd would need to produce outstanding growth that's well in excess of the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 3.2%. That put a dampener on the good run it was having over the longer-term as its three-year revenue growth is still a noteworthy 9.6% in total. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 37% during the coming year according to the seven analysts following the company. That's shaping up to be materially lower than the 212% growth forecast for the broader industry.

In light of this, it's alarming that Nanjing King-Friend Biochemical PharmaceuticalLtd's P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

What Does Nanjing King-Friend Biochemical PharmaceuticalLtd's P/S Mean For Investors?

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've concluded that Nanjing King-Friend Biochemical PharmaceuticalLtd currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you settle on your opinion, we've discovered 1 warning sign for Nanjing King-Friend Biochemical PharmaceuticalLtd that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

If you're looking to trade Nanjing King-Friend Biochemical PharmaceuticalLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nanjing King-Friend Biochemical PharmaceuticalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603707

Nanjing King-Friend Biochemical PharmaceuticalLtd

Nanjing King-Friend Biochemical Pharmaceutical Co.,Ltd.

High growth potential with excellent balance sheet.