Investors Still Waiting For A Pull Back In Nanjing King-Friend Biochemical Pharmaceutical Co.,Ltd. (SHSE:603707)

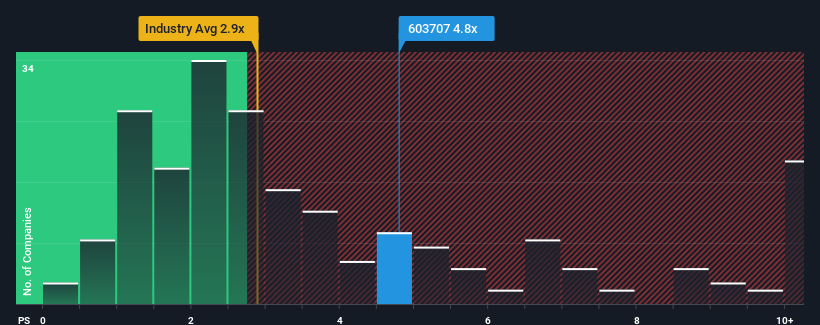

When you see that almost half of the companies in the Pharmaceuticals industry in China have price-to-sales ratios (or "P/S") below 2.9x, Nanjing King-Friend Biochemical Pharmaceutical Co.,Ltd. (SHSE:603707) looks to be giving off some sell signals with its 4.8x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Nanjing King-Friend Biochemical PharmaceuticalLtd

How Has Nanjing King-Friend Biochemical PharmaceuticalLtd Performed Recently?

Nanjing King-Friend Biochemical PharmaceuticalLtd could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Nanjing King-Friend Biochemical PharmaceuticalLtd will help you uncover what's on the horizon.Is There Enough Revenue Growth Forecasted For Nanjing King-Friend Biochemical PharmaceuticalLtd?

The only time you'd be truly comfortable seeing a P/S as high as Nanjing King-Friend Biochemical PharmaceuticalLtd's is when the company's growth is on track to outshine the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 5.6%. That put a dampener on the good run it was having over the longer-term as its three-year revenue growth is still a noteworthy 18% in total. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 30% as estimated by the five analysts watching the company. With the industry only predicted to deliver 16%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Nanjing King-Friend Biochemical PharmaceuticalLtd's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Nanjing King-Friend Biochemical PharmaceuticalLtd's P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Nanjing King-Friend Biochemical PharmaceuticalLtd maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Pharmaceuticals industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you take the next step, you should know about the 1 warning sign for Nanjing King-Friend Biochemical PharmaceuticalLtd that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Nanjing King-Friend Biochemical PharmaceuticalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603707

Nanjing King-Friend Biochemical PharmaceuticalLtd

Nanjing King-Friend Biochemical Pharmaceutical Co.,Ltd.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives