Advertisement

- South Korea

- /

- Biotech

- /

- KOSDAQ:A214450

Three Insider-Favored Growth Stocks To Watch

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have been navigating a complex landscape marked by U.S. tariff uncertainties and mixed economic signals, with major indices like the S&P 500 experiencing slight declines amid these challenges. As investors assess the implications of trade policies and economic data on their portfolios, insider ownership in growth companies can serve as a potential indicator of confidence in long-term prospects, making such stocks particularly intriguing to watch during volatile times.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 50.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.9% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 111.4% |

We're going to check out a few of the best picks from our screener tool.

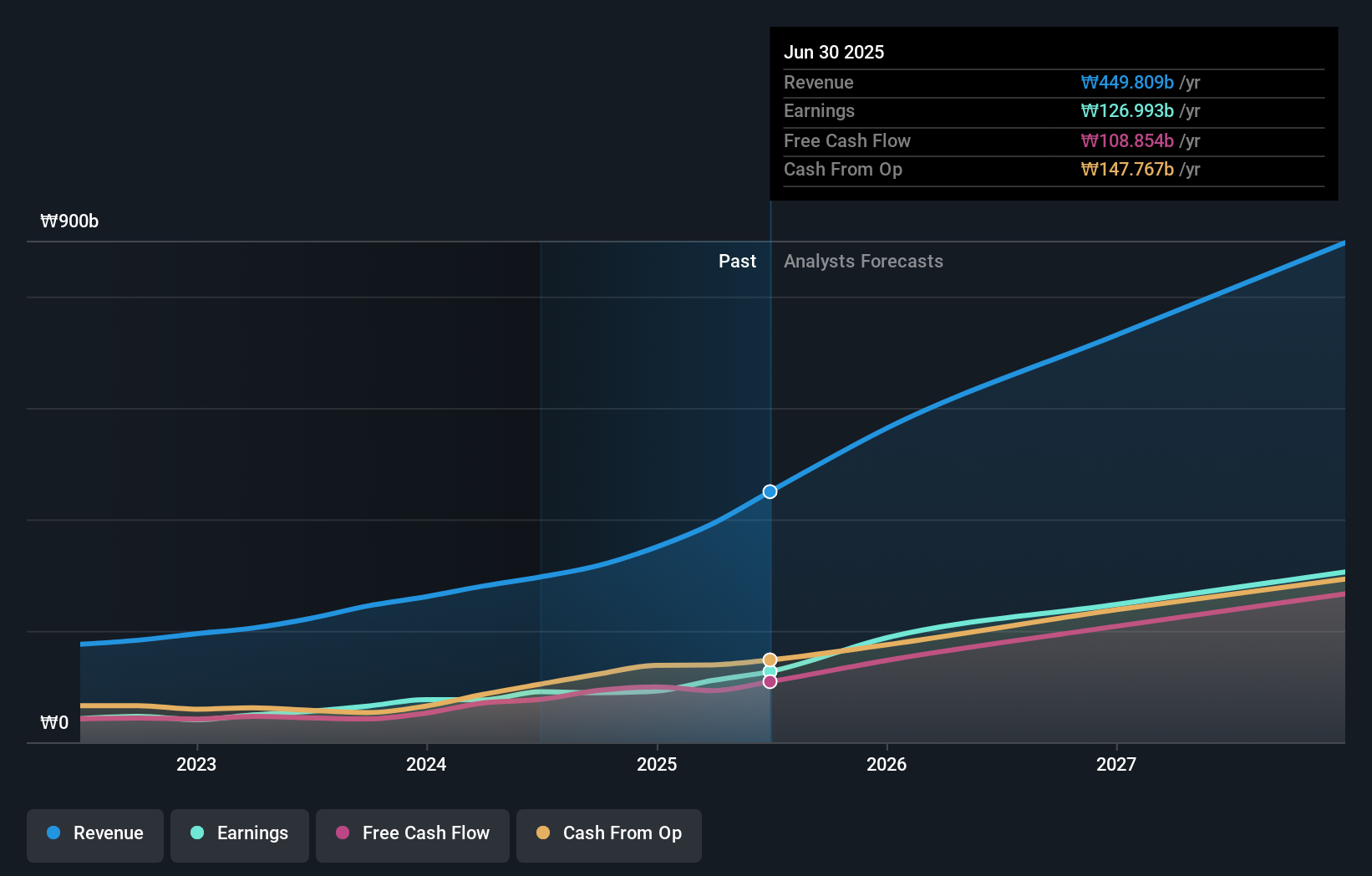

PharmaResearch (KOSDAQ:A214450)

Simply Wall St Growth Rating: ★★★★★☆

Overview: PharmaResearch Co., Ltd., along with its subsidiaries, operates as a biopharmaceutical company primarily in South Korea, with a market cap of ₩2.83 trillion.

Operations: The company generates its revenue from the pharmaceuticals segment, amounting to ₩317.00 billion.

Insider Ownership: 38.6%

Earnings Growth Forecast: 25.7% p.a.

PharmaResearch's earnings are projected to grow at 25.69% annually, slightly below the Korean market's 26%, but its revenue growth of 22.7% outpaces the market significantly. The company trades at a slight discount to its estimated fair value and boasts a high forecasted return on equity of 22.8%. Despite no recent insider trading activity, PharmaResearch's strong financial forecasts highlight its potential as a growth-focused investment with substantial insider ownership.

- Click here to discover the nuances of PharmaResearch with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of PharmaResearch shares in the market.

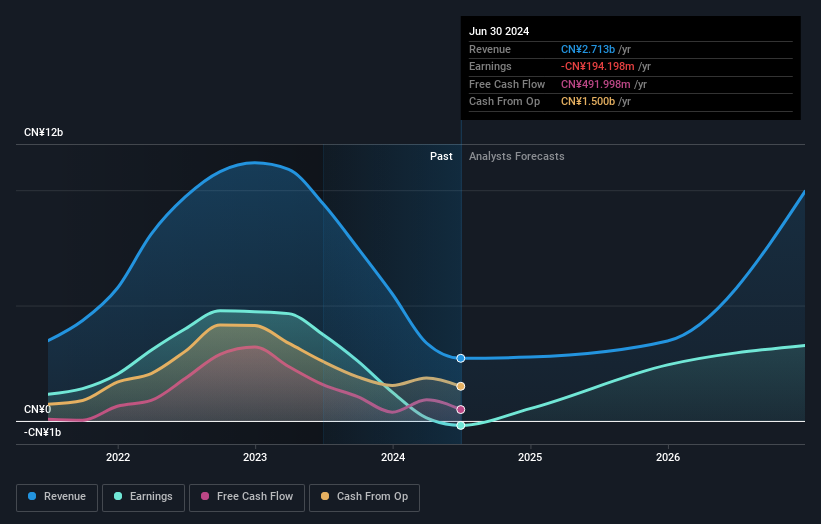

Beijing Wantai Biological Pharmacy Enterprise (SHSE:603392)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beijing Wantai Biological Pharmacy Enterprise Co., Ltd. is a company engaged in the development, production, and sale of vaccines and diagnostic reagents, with a market cap of CN¥83.12 billion.

Operations: The company's revenue segments include the development, production, and sale of vaccines and diagnostic reagents.

Insider Ownership: 24.1%

Earnings Growth Forecast: 109.4% p.a.

Beijing Wantai Biological Pharmacy Enterprise is poised for significant growth with earnings forecasted to expand at 109.45% annually, outpacing the market. The company's revenue is expected to grow by 59.4% per year, surpassing the Chinese market's average of 13.4%. Despite a low forecasted return on equity of 17.9%, its anticipated profitability within three years underscores its potential as an investment opportunity with substantial insider ownership and strong growth prospects.

- Take a closer look at Beijing Wantai Biological Pharmacy Enterprise's potential here in our earnings growth report.

- Our valuation report here indicates Beijing Wantai Biological Pharmacy Enterprise may be overvalued.

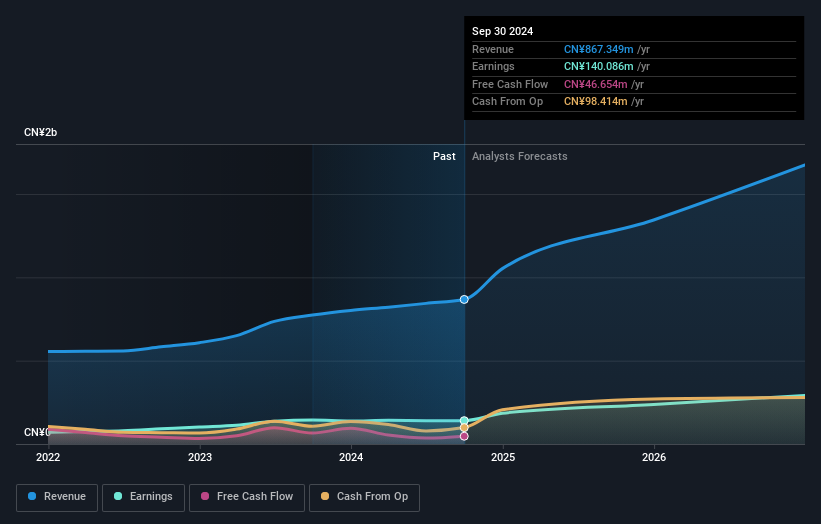

Zhejiang Fengmao Technology (SZSE:301459)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Fengmao Technology Co., Ltd. is involved in the research, development, manufacture, and sale of belt-driven systems, fluid pipelines, and rubber sealing systems in China with a market cap of CN¥3.40 billion.

Operations: The company's revenue is primarily derived from its Machinery & Industrial Equipment segment, which generated CN¥867.35 million.

Insider Ownership: 12.5%

Earnings Growth Forecast: 29.4% p.a.

Zhejiang Fengmao Technology is projected to experience robust growth, with earnings expected to increase by 29.4% annually, surpassing the Chinese market's average of 25.3%. The company's revenue is forecasted to grow at 27.6% per year, exceeding the market's 13.4%. Despite a lower forecasted return on equity of 11.1%, its price-to-earnings ratio of 29.2x remains attractive compared to the market average of 36.4x, highlighting its potential in growth investment strategies with substantial insider ownership.

- Click here and access our complete growth analysis report to understand the dynamics of Zhejiang Fengmao Technology.

- Our expertly prepared valuation report Zhejiang Fengmao Technology implies its share price may be too high.

Key Takeaways

- Explore the 1447 names from our Fast Growing Companies With High Insider Ownership screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A214450

PharmaResearch

Operates as a biopharmaceutical company primarily in South Korea.

Exceptional growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor