Shanghai Haixin Group Co., Ltd.'s (SHSE:600851) 26% Share Price Surge Not Quite Adding Up

Despite an already strong run, Shanghai Haixin Group Co., Ltd. (SHSE:600851) shares have been powering on, with a gain of 26% in the last thirty days. Notwithstanding the latest gain, the annual share price return of 9.0% isn't as impressive.

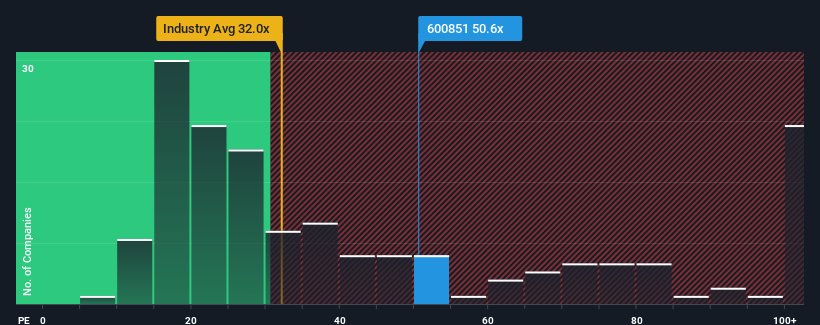

After such a large jump in price, Shanghai Haixin Group may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 50.6x, since almost half of all companies in China have P/E ratios under 37x and even P/E's lower than 21x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Shanghai Haixin Group certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Shanghai Haixin Group

How Is Shanghai Haixin Group's Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Shanghai Haixin Group's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 49% gain to the company's bottom line. As a result, it also grew EPS by 21% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 38% over the next year, materially higher than the company's recent medium-term annualised growth rates.

In light of this, it's alarming that Shanghai Haixin Group's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Shanghai Haixin Group's P/E

The large bounce in Shanghai Haixin Group's shares has lifted the company's P/E to a fairly high level. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Shanghai Haixin Group currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. Right now we are increasingly uncomfortable with the high P/E as this earnings performance isn't likely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Shanghai Haixin Group that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Shanghai Haixin Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600851

Shanghai Haixin Group

Engages in the pharmaceutical, textile and clothing, and finance businesses.

Flawless balance sheet with acceptable track record.

Market Insights

Community Narratives