Cautious Investors Not Rewarding Zhejiang Huahai Pharmaceutical Co., Ltd.'s (SHSE:600521) Performance Completely

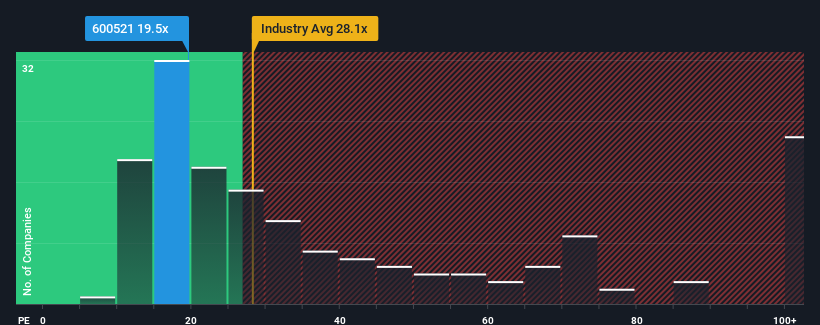

When close to half the companies in China have price-to-earnings ratios (or "P/E's") above 37x, you may consider Zhejiang Huahai Pharmaceutical Co., Ltd. (SHSE:600521) as an attractive investment with its 19.5x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Zhejiang Huahai Pharmaceutical as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Zhejiang Huahai Pharmaceutical

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Zhejiang Huahai Pharmaceutical would need to produce sluggish growth that's trailing the market.

If we review the last year of earnings growth, the company posted a worthy increase of 3.0%. This was backed up an excellent period prior to see EPS up by 67% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next year should generate growth of 38% as estimated by the three analysts watching the company. With the market predicted to deliver 37% growth , the company is positioned for a comparable earnings result.

In light of this, it's peculiar that Zhejiang Huahai Pharmaceutical's P/E sits below the majority of other companies. It may be that most investors are not convinced the company can achieve future growth expectations.

What We Can Learn From Zhejiang Huahai Pharmaceutical's P/E?

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Zhejiang Huahai Pharmaceutical's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Zhejiang Huahai Pharmaceutical that you need to be mindful of.

Of course, you might also be able to find a better stock than Zhejiang Huahai Pharmaceutical. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Huahai Pharmaceutical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600521

Zhejiang Huahai Pharmaceutical

Operates as a pharmaceutical company in China and internationally.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Community Narratives