- China

- /

- Entertainment

- /

- SZSE:300860

Funshine Culture Group Co.,Ltd.'s (SZSE:300860) Popularity With Investors Is Clear

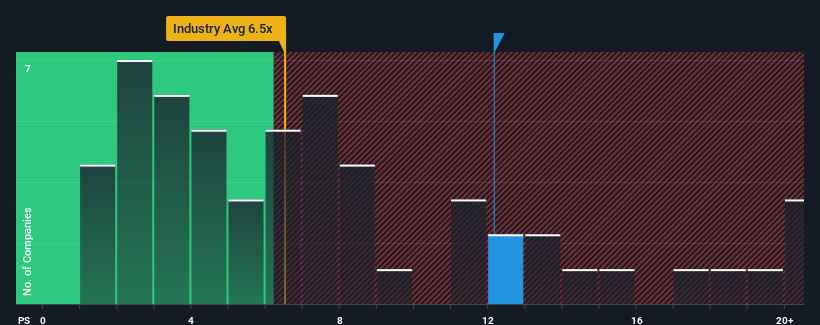

With a price-to-sales (or "P/S") ratio of 12.2x Funshine Culture Group Co.,Ltd. (SZSE:300860) may be sending very bearish signals at the moment, given that almost half of all the Entertainment companies in China have P/S ratios under 6.5x and even P/S lower than 3x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Funshine Culture GroupLtd

What Does Funshine Culture GroupLtd's Recent Performance Look Like?

Recent times have been advantageous for Funshine Culture GroupLtd as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Funshine Culture GroupLtd's future stacks up against the industry? In that case, our free report is a great place to start.How Is Funshine Culture GroupLtd's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Funshine Culture GroupLtd's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 16%. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 58% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 268% during the coming year according to the dual analysts following the company. With the industry only predicted to deliver 35%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Funshine Culture GroupLtd's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Funshine Culture GroupLtd's P/S?

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look into Funshine Culture GroupLtd shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Funshine Culture GroupLtd that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300860

Funshine Culture GroupLtd

Engages in cultural performing events, cultural tourism, and public artistic lighting business in China.

Flawless balance sheet with moderate growth potential.

Market Insights

Community Narratives