- Japan

- /

- Electronic Equipment and Components

- /

- TSE:7732

High Growth Tech Leads These 3 Promising Stocks with Strong Potential

Reviewed by Simply Wall St

In a week marked by record highs in major indices like the S&P 500 and Russell 2000, global markets demonstrated resilience despite geopolitical tensions and tariff concerns. As small-cap stocks join their larger peers in reaching new heights, investors are increasingly focused on identifying high-growth tech companies that can thrive amid economic shifts and policy changes. A good stock in this environment typically exhibits strong innovation potential, robust market positioning, and adaptability to evolving economic landscapes.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Material Group | 20.45% | 24.01% | ★★★★★★ |

| Seojin SystemLtd | 35.41% | 39.86% | ★★★★★★ |

| Yggdrazil Group | 30.20% | 87.10% | ★★★★★★ |

| eWeLLLtd | 27.24% | 28.74% | ★★★★★★ |

| Ascelia Pharma | 76.15% | 47.16% | ★★★★★★ |

| Mental Health TechnologiesLtd | 24.68% | 97.53% | ★★★★★★ |

| Medley | 25.57% | 31.67% | ★★★★★★ |

| CD Projekt | 22.02% | 28.64% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 131.08% | ★★★★★★ |

| JNTC | 29.48% | 104.37% | ★★★★★★ |

Click here to see the full list of 1282 stocks from our High Growth Tech and AI Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

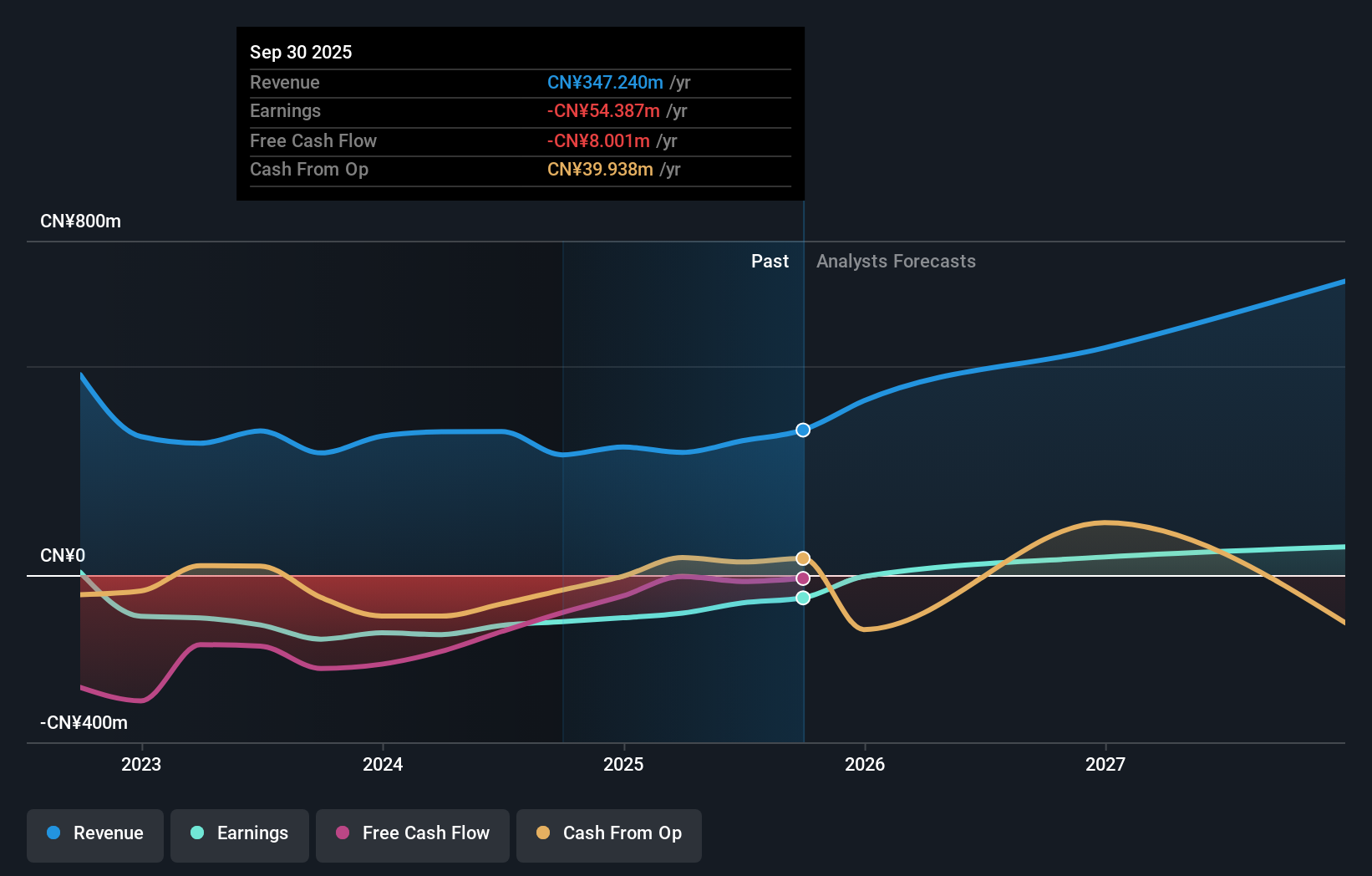

Hangzhou Arcvideo Technology (SHSE:688039)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hangzhou Arcvideo Technology Co., Ltd. offers smart and secure video solutions and video cloud services for media platforms, with a market cap of CN¥3.68 billion.

Operations: The company generates revenue primarily through its smart video solutions and cloud services tailored for media platforms. With a market capitalization of CN¥3.68 billion, it focuses on providing secure and innovative video technologies to enhance media operations.

Despite a challenging environment, Hangzhou Arcvideo Technology has demonstrated robust revenue growth, with an impressive 27.9% increase per year, outpacing the broader Chinese market's growth rate of 13.8%. This momentum is underpinned by significant R&D investment which fuels innovation and competitive edge in the tech sector. However, it's important to note that the company is currently unprofitable with a net loss reducing from CNY 96.16 million to CNY 69.45 million year-over-year, showing signs of financial stabilization albeit slowly. Looking ahead, earnings are expected to surge by an astonishing 124.1% annually over the next three years as the company approaches profitability and continues to capitalize on high demand for advanced technology solutions in its market segment.

- Delve into the full analysis health report here for a deeper understanding of Hangzhou Arcvideo Technology.

Learn about Hangzhou Arcvideo Technology's historical performance.

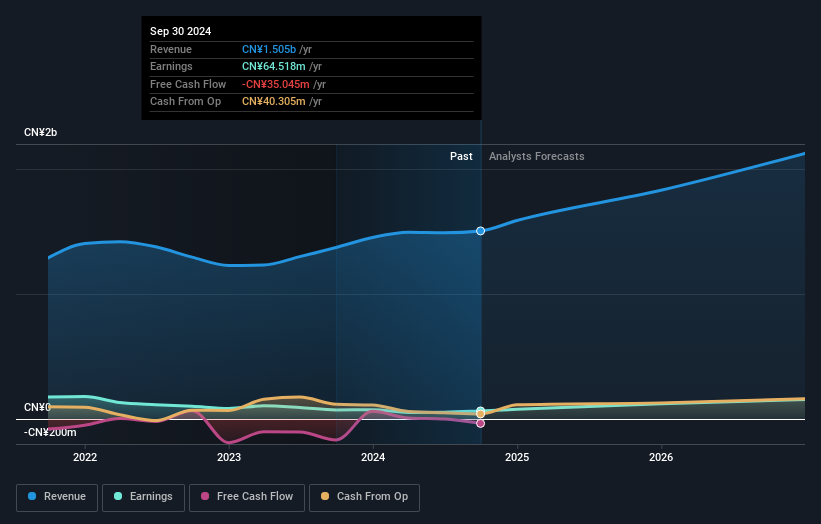

Beijing Zhidemai Technology (SZSE:300785)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Beijing Zhidemai Technology Co., Ltd. is involved in Internet information promotion activities both within China and globally, with a market cap of CN¥6.36 billion.

Operations: Zhidemai Technology focuses on Internet information promotion services, operating both domestically and internationally. The company generates revenue through digital marketing and advertising activities, leveraging its platform to connect consumers with various brands and products.

Beijing Zhidemai Technology is navigating a complex market landscape, evidenced by its recent financial performance with revenues climbing to CNY 1.01 billion, up from CNY 959.05 million the previous year. Despite this growth, net income has dipped to CNY 3.8 million from CNY 14.06 million, reflecting a challenging operational environment but also underscoring resilience in revenue streams. The company's commitment to innovation is marked by robust R&D spending which strategically positions it for future technology demands and competitive differentiation in the tech sector; such investment is crucial as it seeks to enhance its product offerings and market reach amidst forecasts of revenue growth at 15.2% annually—outpacing the broader Chinese market's expansion rate of 13.8%. Moreover, earnings are projected to surge by an impressive 39.5% per year, signaling potential for significant financial improvements and shareholder value creation in the coming years.

- Click here and access our complete health analysis report to understand the dynamics of Beijing Zhidemai Technology.

Understand Beijing Zhidemai Technology's track record by examining our Past report.

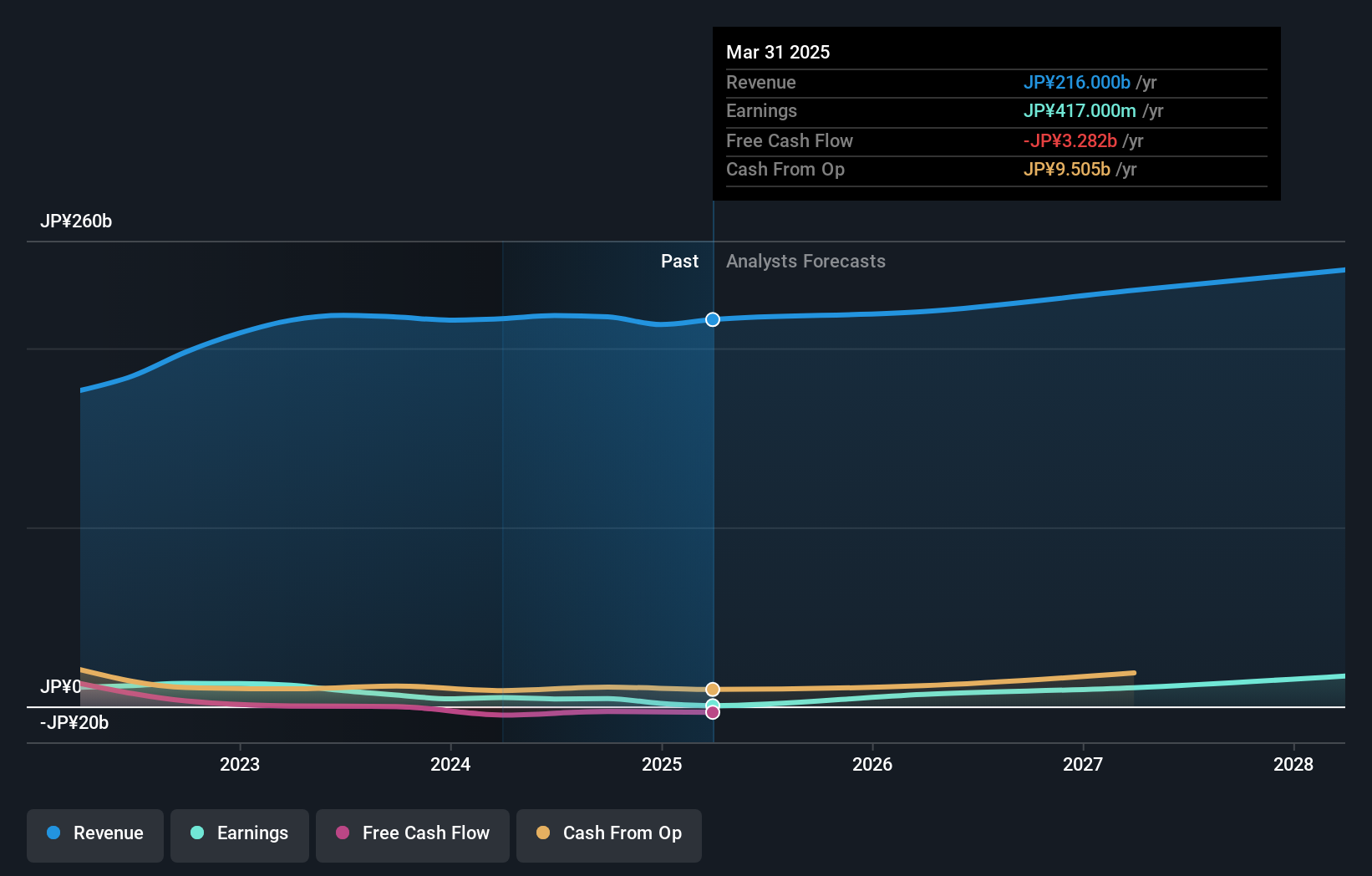

Topcon (TSE:7732)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Topcon Corporation, with a market cap of ¥178.57 billion, develops, manufactures, and sells positioning, eye care, and smart infrastructure products both in Japan and internationally through its subsidiaries.

Operations: Topcon focuses on three main business segments: positioning, eye care, and smart infrastructure. The company's revenue streams are diversified across these segments, with a significant portion derived from international markets.

Topcon's strategic focus on integrating AI in healthcare imaging, as evidenced by its collaboration with BeeKeeperAI, underscores its innovative approach to expanding market reach and enhancing disease management capabilities. This partnership not only accelerates the application of AI models but also ensures data privacy and intellectual property protection, crucial in the competitive tech landscape. Financially, Topcon is positioning for growth with expected revenue hitting JPY 220 billion and a robust profit forecast of JPY 4.5 billion for FY2025. The company's R&D commitment is reflected in its substantial investment rate of 6%, aimed at fostering advancements in technology that align with industry demands and future profitability, projected to surge by an impressive 30.2% annually.

- Get an in-depth perspective on Topcon's performance by reading our health report here.

Evaluate Topcon's historical performance by accessing our past performance report.

Key Takeaways

- Gain an insight into the universe of 1282 High Growth Tech and AI Stocks by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Topcon might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7732

Topcon

Develops, manufactures, and sells positioning, eye care, and smart infrastructure products in Japan and internationally.

Reasonable growth potential slight.