Guangdong Insight Brand Marketing Group Co.,Ltd.'s (SZSE:300781) 29% Dip Still Leaving Some Shareholders Feeling Restless Over Its P/SRatio

Guangdong Insight Brand Marketing Group Co.,Ltd. (SZSE:300781) shares have retraced a considerable 29% in the last month, reversing a fair amount of their solid recent performance. Still, a bad month hasn't completely ruined the past year with the stock gaining 100%, which is great even in a bull market.

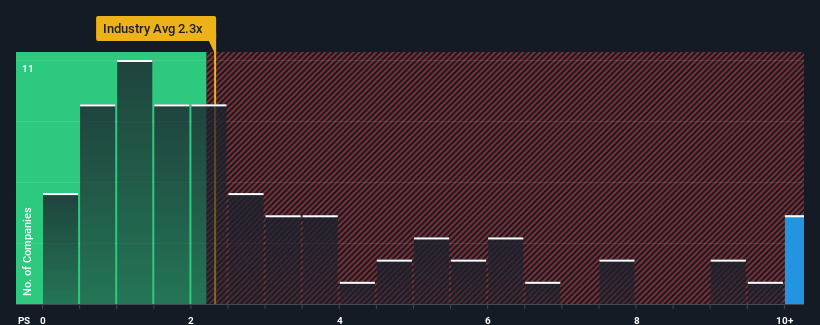

In spite of the heavy fall in price, given around half the companies in China's Media industry have price-to-sales ratios (or "P/S") below 2.3x, you may still consider Guangdong Insight Brand Marketing GroupLtd as a stock to avoid entirely with its 11.3x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Guangdong Insight Brand Marketing GroupLtd

How Guangdong Insight Brand Marketing GroupLtd Has Been Performing

For instance, Guangdong Insight Brand Marketing GroupLtd's receding revenue in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/S from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

Although there are no analyst estimates available for Guangdong Insight Brand Marketing GroupLtd, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Guangdong Insight Brand Marketing GroupLtd?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Guangdong Insight Brand Marketing GroupLtd's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 11%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 65% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

It's interesting to note that the rest of the industry is similarly expected to grow by 20% over the next year, which is fairly even with the company's recent medium-term annualised growth rates.

In light of this, it's curious that Guangdong Insight Brand Marketing GroupLtd's P/S sits above the majority of other companies. Apparently many investors in the company are more bullish than recent times would indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as a continuation of recent revenue trends would weigh down the share price eventually.

What We Can Learn From Guangdong Insight Brand Marketing GroupLtd's P/S?

Even after such a strong price drop, Guangdong Insight Brand Marketing GroupLtd's P/S still exceeds the industry median significantly. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We didn't expect to see Guangdong Insight Brand Marketing GroupLtd trade at such a high P/S considering its last three-year revenue growth has only been on par with the rest of the industry. When we see average revenue with industry-like growth combined with a high P/S, we suspect the share price is at risk of declining, bringing the P/S back in line with the industry too. Unless there is a significant improvement in the company's medium-term trends, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Guangdong Insight Brand Marketing GroupLtd that you need to be mindful of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300781

Guangdong Insight Brand Marketing GroupLtd

Guangdong Insight Brand Marketing Group Co.,Ltd.

Excellent balance sheet with acceptable track record.

Market Insights

Community Narratives