- China

- /

- Entertainment

- /

- SZSE:300426

Optimistic Investors Push Zhejiang Talent Television and Film Co., Ltd. (SZSE:300426) Shares Up 26% But Growth Is Lacking

Despite an already strong run, Zhejiang Talent Television and Film Co., Ltd. (SZSE:300426) shares have been powering on, with a gain of 26% in the last thirty days. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 4.8% in the last twelve months.

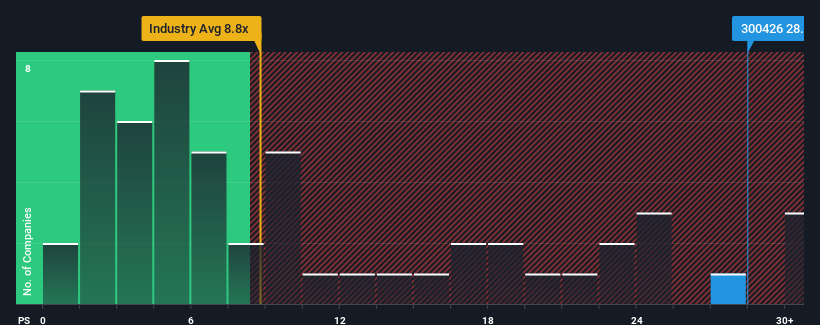

Since its price has surged higher, given around half the companies in China's Entertainment industry have price-to-sales ratios (or "P/S") below 8.8x, you may consider Zhejiang Talent Television and Film as a stock to avoid entirely with its 28.5x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for Zhejiang Talent Television and Film

How Zhejiang Talent Television and Film Has Been Performing

For instance, Zhejiang Talent Television and Film's receding revenue in recent times would have to be some food for thought. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Zhejiang Talent Television and Film will help you shine a light on its historical performance.Do Revenue Forecasts Match The High P/S Ratio?

Zhejiang Talent Television and Film's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 67%. The last three years don't look nice either as the company has shrunk revenue by 19% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 34% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we find it worrying that Zhejiang Talent Television and Film's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

What Does Zhejiang Talent Television and Film's P/S Mean For Investors?

The strong share price surge has lead to Zhejiang Talent Television and Film's P/S soaring as well. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Zhejiang Talent Television and Film currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

Having said that, be aware Zhejiang Talent Television and Film is showing 1 warning sign in our investment analysis, you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Talent Television and Film might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300426

Zhejiang Talent Television and Film

Zhejiang Talent Television and Film Co., Ltd.

Worrying balance sheet minimal.

Market Insights

Community Narratives