- China

- /

- Entertainment

- /

- SZSE:300251

Investors Appear Satisfied With Beijing Enlight Media Co., Ltd.'s (SZSE:300251) Prospects As Shares Rocket 28%

Beijing Enlight Media Co., Ltd. (SZSE:300251) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. Taking a wider view, although not as strong as the last month, the full year gain of 22% is also fairly reasonable.

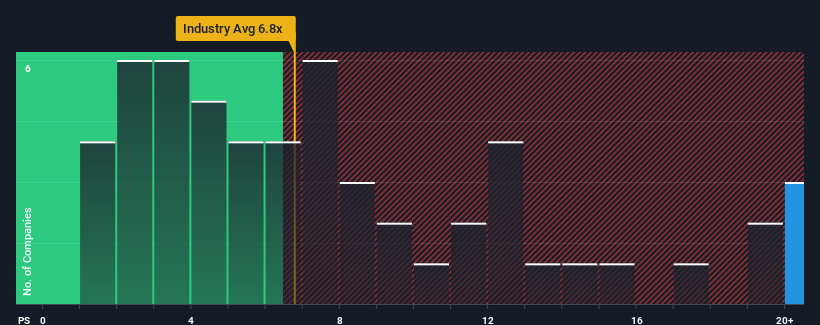

Since its price has surged higher, Beijing Enlight Media may be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 27.3x, since almost half of all companies in the Entertainment industry in China have P/S ratios under 6.8x and even P/S lower than 3x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Beijing Enlight Media

How Beijing Enlight Media Has Been Performing

Beijing Enlight Media certainly has been doing a good job lately as it's been growing revenue more than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Beijing Enlight Media.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Beijing Enlight Media would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 15% last year. The latest three year period has also seen a 19% overall rise in revenue, aided extensively by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the ten analysts covering the company suggest revenue should grow by 112% over the next year. That's shaping up to be materially higher than the 35% growth forecast for the broader industry.

With this information, we can see why Beijing Enlight Media is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What Does Beijing Enlight Media's P/S Mean For Investors?

Shares in Beijing Enlight Media have seen a strong upwards swing lately, which has really helped boost its P/S figure. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Beijing Enlight Media's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Beijing Enlight Media with six simple checks.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Enlight Media might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300251

Beijing Enlight Media

Engages in the investment, production, and distribution of film and television projects in China.

Flawless balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Community Narratives