Advertisement

Miracll ChemicalsLtd's (SZSE:300848) Anemic Earnings Might Be Worse Than You Think

The subdued market reaction suggests that Miracll Chemicals Co.,Ltd's (SZSE:300848) recent earnings didn't contain any surprises. However, we believe that investors should be aware of some underlying factors which may be of concern.

View our latest analysis for Miracll ChemicalsLtd

A Closer Look At Miracll ChemicalsLtd's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

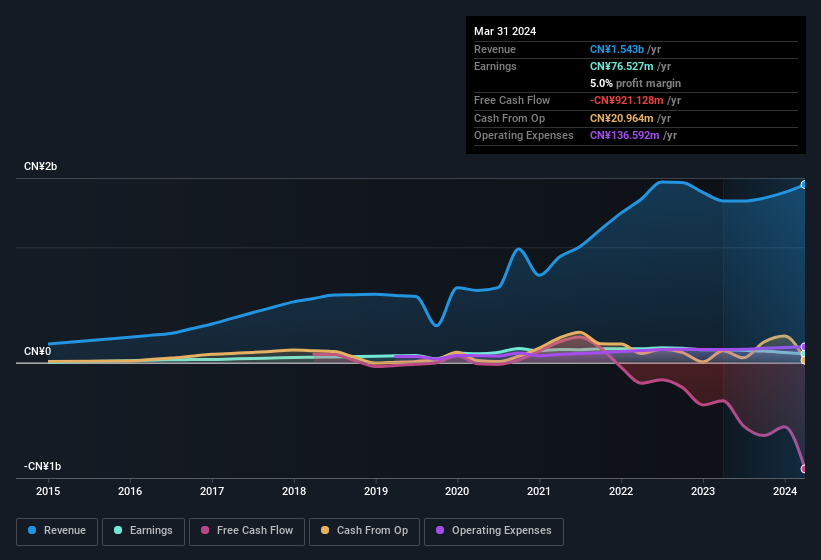

Miracll ChemicalsLtd has an accrual ratio of 0.80 for the year to March 2024. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of CN¥921m, in contrast to the aforementioned profit of CN¥76.5m. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of CN¥921m, this year, indicates high risk. Having said that, there is more to consider. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, Miracll ChemicalsLtd increased the number of shares on issue by 6.2% over the last twelve months by issuing new shares. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Miracll ChemicalsLtd's EPS by clicking here.

A Look At The Impact Of Miracll ChemicalsLtd's Dilution On Its Earnings Per Share (EPS)

Miracll ChemicalsLtd's net profit dropped by 33% per year over the last three years. And even focusing only on the last twelve months, we see profit is down 32%. Like a sack of potatoes thrown from a delivery truck, EPS fell harder, down 32% in the same period. So you can see that the dilution has had a bit of an impact on shareholders.

If Miracll ChemicalsLtd's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

The Impact Of Unusual Items On Profit

Unfortunately (in the short term) Miracll ChemicalsLtd saw its profit reduced by unusual items worth CN¥11m. In the case where this was a non-cash charge it would have made it easier to have high cash conversion, so it's surprising that the accrual ratio tells a different story. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Miracll ChemicalsLtd to produce a higher profit next year, all else being equal.

Our Take On Miracll ChemicalsLtd's Profit Performance

Summing up, Miracll ChemicalsLtd's unusual items suggest that its statutory earnings were temporarily depressed, and its accrual ratio indicates a lack of free cash flow relative to profit. On top of that, the dilution means that shareholders now own less of the company. Based on these factors, we think that Miracll ChemicalsLtd's statutory profits probably make it seem better than it is on an underlying level. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For example, Miracll ChemicalsLtd has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300848

Miracll ChemicalsLtd

Researches, develops, manufactures, and sells thermoplastic polyurethane (TPU) elastomers.

High growth potential with acceptable track record.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.3% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor