- China

- /

- Metals and Mining

- /

- SZSE:300337

If EPS Growth Is Important To You, Yinbang Clad MaterialLtd (SZSE:300337) Presents An Opportunity

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Yinbang Clad MaterialLtd (SZSE:300337). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Yinbang Clad MaterialLtd with the means to add long-term value to shareholders.

See our latest analysis for Yinbang Clad MaterialLtd

How Fast Is Yinbang Clad MaterialLtd Growing?

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That makes EPS growth an attractive quality for any company. Impressively, Yinbang Clad MaterialLtd has grown EPS by 24% per year, compound, in the last three years. This has no doubt fuelled the optimism that sees the stock trading on a high multiple of earnings.

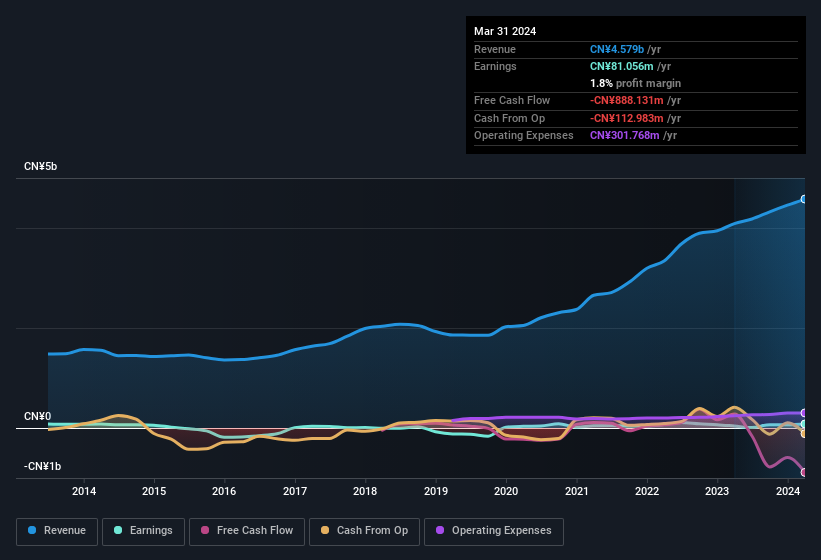

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. While we note Yinbang Clad MaterialLtd achieved similar EBIT margins to last year, revenue grew by a solid 12% to CN¥4.6b. That's encouraging news for the company!

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

While it's always good to see growing profits, you should always remember that a weak balance sheet could come back to bite. So check Yinbang Clad MaterialLtd's balance sheet strength, before getting too excited.

Are Yinbang Clad MaterialLtd Insiders Aligned With All Shareholders?

It should give investors a sense of security owning shares in a company if insiders also own shares, creating a close alignment their interests. So it is good to see that Yinbang Clad MaterialLtd insiders have a significant amount of capital invested in the stock. Notably, they have an enviable stake in the company, worth CN¥1.4b. That equates to 25% of the company, making insiders powerful and aligned with other shareholders. Very encouraging.

It's good to see that insiders are invested in the company, but are remuneration levels reasonable? Well, based on the CEO pay, you'd argue that they are indeed. For companies with market capitalisations between CN¥2.9b and CN¥12b, like Yinbang Clad MaterialLtd, the median CEO pay is around CN¥987k.

The CEO of Yinbang Clad MaterialLtd was paid just CN¥429k in total compensation for the year ending December 2023. You could consider this pay as somewhat symbolic, which suggests the CEO does not need a lot of compensation to stay motivated. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Is Yinbang Clad MaterialLtd Worth Keeping An Eye On?

For growth investors, Yinbang Clad MaterialLtd's raw rate of earnings growth is a beacon in the night. If you need more convincing beyond that EPS growth rate, don't forget about the reasonable remuneration and the high insider ownership. This may only be a fast rundown, but the key takeaway is that Yinbang Clad MaterialLtd is worth keeping an eye on. Even so, be aware that Yinbang Clad MaterialLtd is showing 3 warning signs in our investment analysis , and 2 of those are a bit unpleasant...

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in CN with promising growth potential and insider confidence.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade Yinbang Clad MaterialLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300337

Yinbang Clad MaterialLtd

Researches, develops, produces, and sells aluminum alloy composites, non-composite materials, and multi-metal composite materials in China.

Solid track record with imperfect balance sheet.