As global markets navigate a challenging landscape marked by cautious Fed commentary and political uncertainties, investors are increasingly focused on the resilience of growth companies with strong insider ownership. In such volatile times, stocks with high insider ownership can be appealing as they often indicate confidence from those who know the company best, potentially aligning management's interests with those of shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 23.9% | 37.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.4% |

| Medley (TSE:4480) | 34% | 31.7% |

| Pharma Mar (BME:PHM) | 11.8% | 56.2% |

| CD Projekt (WSE:CDR) | 29.7% | 27% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.4% | 66.3% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's take a closer look at a couple of our picks from the screened companies.

Pexip Holding (OB:PEXIP)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Pexip Holding ASA is a video technology company that offers an end-to-end video conferencing platform and digital infrastructure globally, with a market cap of NOK4.60 billion.

Operations: The company's revenue primarily comes from the Sale of Collaboration Services, amounting to NOK1.07 billion.

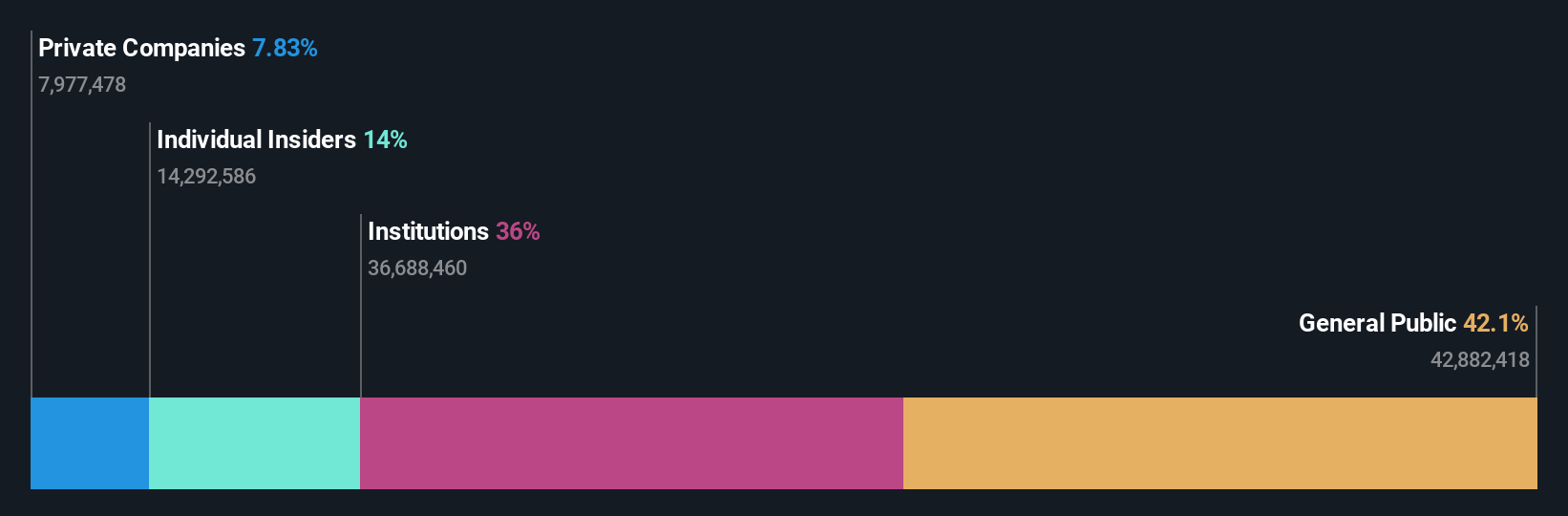

Insider Ownership: 19.1%

Revenue Growth Forecast: 12.6% p.a.

Pexip Holding's recent earnings report shows a positive turnaround with NOK 5.8 million net income in Q3 2024, compared to a loss last year. Despite forecasts of modest revenue growth at 12.6% annually, the company is expected to achieve above-average profit growth over the next three years. While significant insider selling occurred recently, Pexip trades at a substantial discount to its estimated fair value, reflecting potential for future appreciation amidst cautious investor sentiment.

- Click here and access our complete growth analysis report to understand the dynamics of Pexip Holding.

- The analysis detailed in our Pexip Holding valuation report hints at an deflated share price compared to its estimated value.

Zhejiang Zhongxin Fluoride MaterialsLtd (SZSE:002915)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Zhongxin Fluoride Materials Co., Ltd engages in the research, development, production, and sale of fluorine fine chemicals in China with a market cap of CN¥4.41 billion.

Operations: Zhejiang Zhongxin Fluoride Materials Co., Ltd generates its revenue through the research, development, production, and sale of fluorine fine chemicals in China.

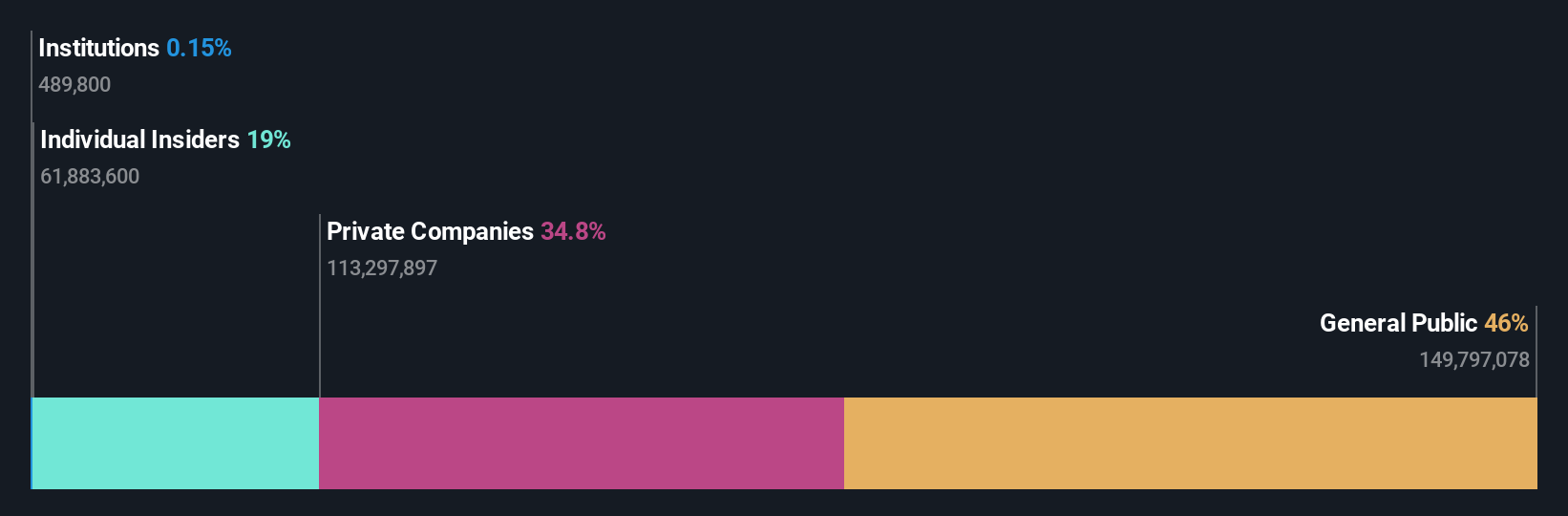

Insider Ownership: 20.7%

Revenue Growth Forecast: 30.8% p.a.

Zhejiang Zhongxin Fluoride Materials is forecast to achieve strong revenue growth of 30.8% annually, surpassing the market average. Despite a current net loss of CNY 42.99 million for the first nine months of 2024, profitability is expected within three years, indicating potential for future expansion. However, the company's financial position shows operating cash flow inadequately covering debt and a volatile share price adds risk. Recent exclusion from the S&P Global BMI Index may impact investor perception.

- Get an in-depth perspective on Zhejiang Zhongxin Fluoride MaterialsLtd's performance by reading our analyst estimates report here.

- The analysis detailed in our Zhejiang Zhongxin Fluoride MaterialsLtd valuation report hints at an inflated share price compared to its estimated value.

Msscorps (TWSE:6830)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Msscorps Co., Ltd. is involved in the testing and analysis of electronic materials across Asia, the United States, and internationally, with a market cap of NT$8.36 billion.

Operations: The company generates its revenue primarily from the Testing and Analysis Service segment, amounting to NT$1.93 billion.

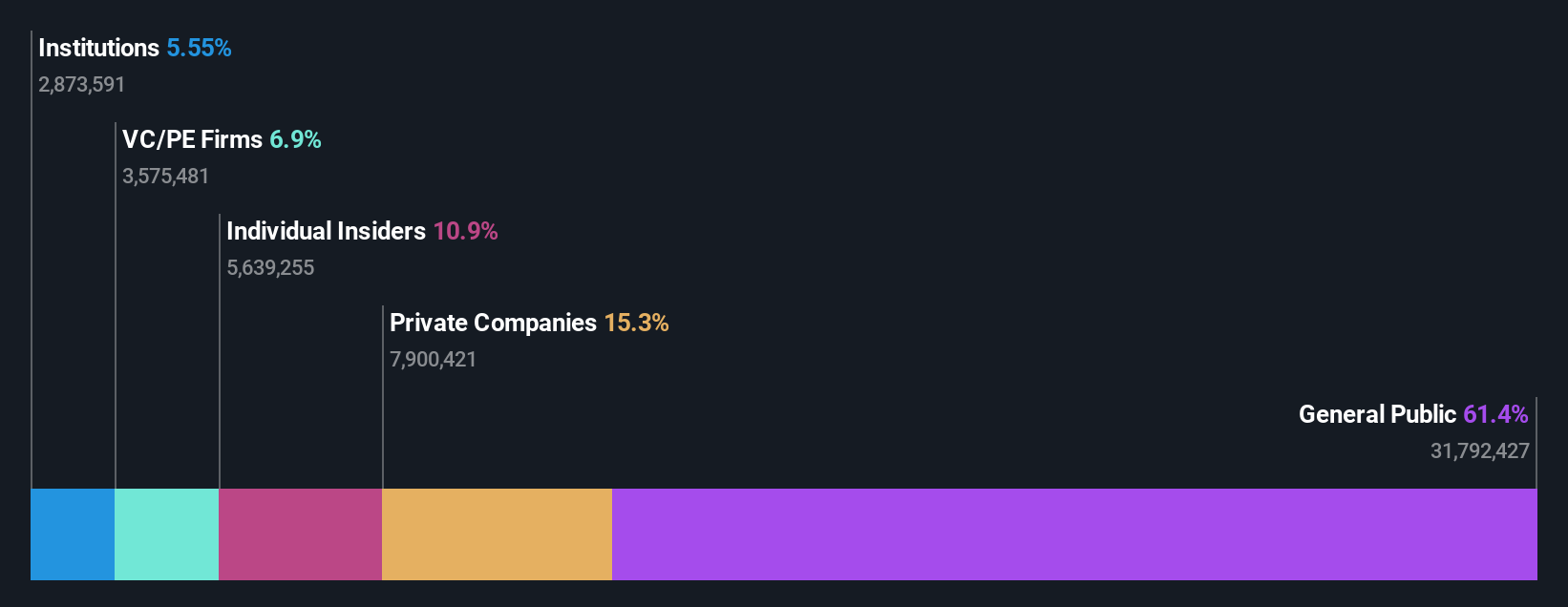

Insider Ownership: 10.9%

Revenue Growth Forecast: 17.4% p.a.

Msscorps is projected to experience significant earnings growth of 71.54% annually, outpacing the Taiwan market's average. However, recent earnings reports reveal a sharp decline in net income for the third quarter and nine months of 2024, with diluted EPS dropping from TWD 1.54 to TWD 0.26 year-on-year. Despite high non-cash earnings quality, revenue growth lags at 17.4% per year and profit margins have decreased significantly from last year, indicating potential challenges ahead.

- Unlock comprehensive insights into our analysis of Msscorps stock in this growth report.

- In light of our recent valuation report, it seems possible that Msscorps is trading beyond its estimated value.

Summing It All Up

- Delve into our full catalog of 1512 Fast Growing Companies With High Insider Ownership here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Zhongxin Fluoride MaterialsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002915

Zhejiang Zhongxin Fluoride MaterialsLtd

Research, develops, produces, and sells fluorine fine chemicals in China.

High growth potential with imperfect balance sheet.

Market Insights

Community Narratives