Shandong Dawn PolymerLtd (SZSE:002838) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Shandong Dawn Polymer Co.,Ltd. (SZSE:002838) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Shandong Dawn PolymerLtd

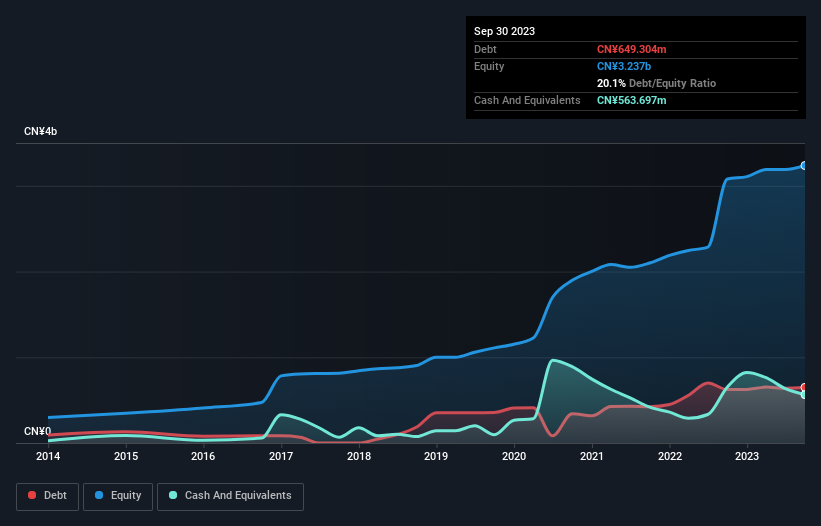

How Much Debt Does Shandong Dawn PolymerLtd Carry?

As you can see below, at the end of September 2023, Shandong Dawn PolymerLtd had CN¥649.3m of debt, up from CN¥623.3m a year ago. Click the image for more detail. However, it also had CN¥563.7m in cash, and so its net debt is CN¥85.6m.

How Strong Is Shandong Dawn PolymerLtd's Balance Sheet?

According to the last reported balance sheet, Shandong Dawn PolymerLtd had liabilities of CN¥1.10b due within 12 months, and liabilities of CN¥487.6m due beyond 12 months. Offsetting this, it had CN¥563.7m in cash and CN¥1.58b in receivables that were due within 12 months. So it actually has CN¥560.5m more liquid assets than total liabilities.

This surplus suggests that Shandong Dawn PolymerLtd has a conservative balance sheet, and could probably eliminate its debt without much difficulty.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 0.40 times EBITDA, Shandong Dawn PolymerLtd is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 9.1 times the interest expense over the last year. The modesty of its debt load may become crucial for Shandong Dawn PolymerLtd if management cannot prevent a repeat of the 38% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But it is Shandong Dawn PolymerLtd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Shandong Dawn PolymerLtd burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

While Shandong Dawn PolymerLtd's conversion of EBIT to free cash flow makes us cautious about it, its track record of (not) growing its EBIT is no better. But at least its net debt to EBITDA is a gleaming silver lining to those clouds. Looking at all the angles mentioned above, it does seem to us that Shandong Dawn PolymerLtd is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example Shandong Dawn PolymerLtd has 4 warning signs (and 1 which shouldn't be ignored) we think you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002838

Shandong Dawn PolymerLtd

Develops, produces, sells, and services thermoplastic elastomer, modified plastic, master batch, and other products in China and internationally.

Adequate balance sheet with acceptable track record.