As global markets continue to navigate the evolving landscape of U.S. policy changes and AI-driven optimism, major indices like the S&P 500 have reached new heights, buoyed by a resurgence in growth stocks. In this environment, companies with high insider ownership often attract attention as they signal confidence from those closest to the business operations.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 22.7% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| CD Projekt (WSE:CDR) | 29.7% | 34.6% |

| Waystream Holding (OM:WAYS) | 11.3% | 113.3% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Pharma Mar (BME:PHM) | 11.9% | 55.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

Let's uncover some gems from our specialized screener.

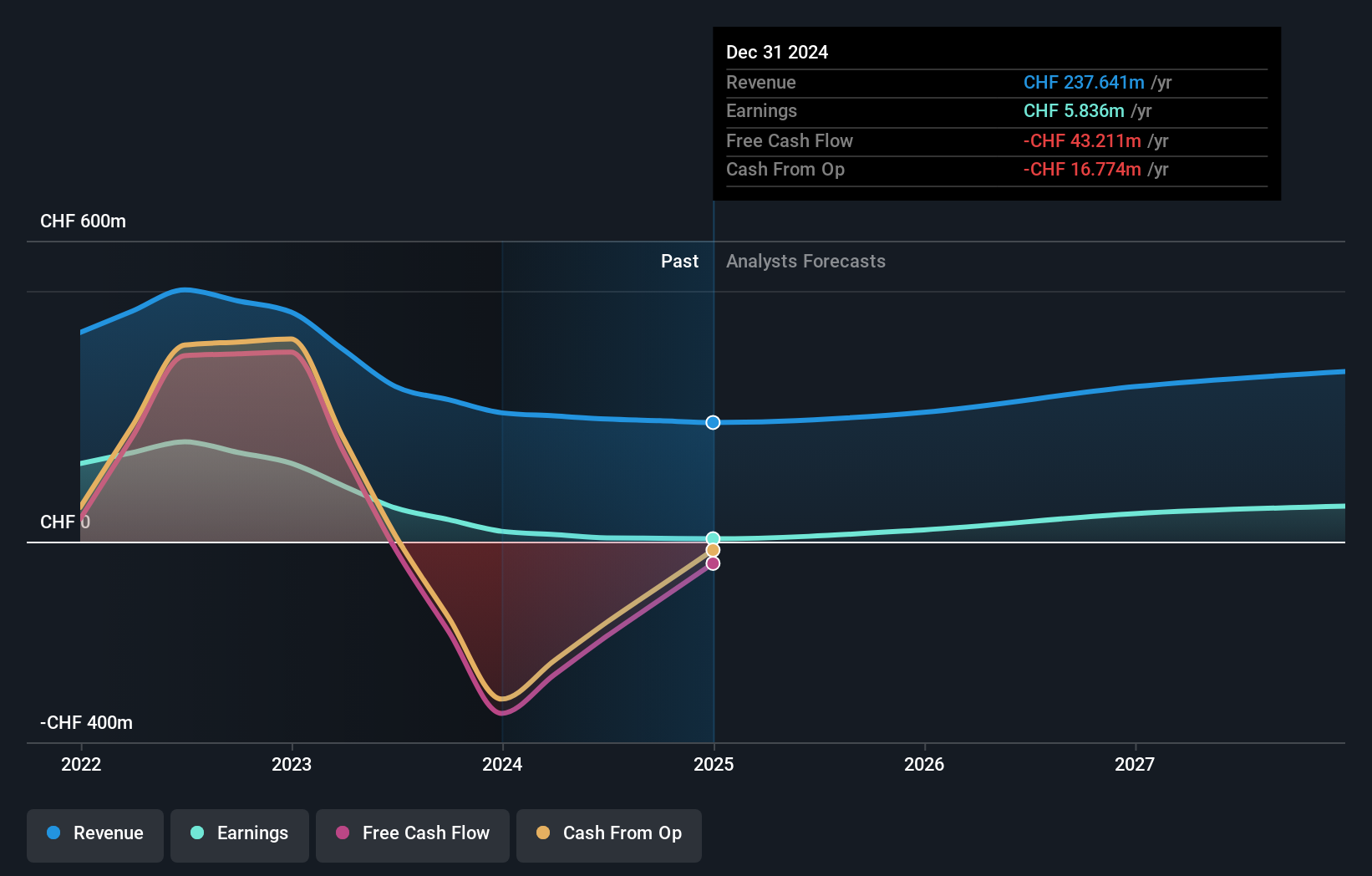

Leonteq (SWX:LEON)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Leonteq AG offers structured investment products and long-term savings and retirement solutions across Switzerland, Europe, and Asia including the Middle East, with a market cap of CHF331.88 million.

Operations: The company generates revenue from its brokerage segment, amounting to CHF244.51 million.

Insider Ownership: 17.7%

Earnings Growth Forecast: 31.2% p.a.

Leonteq's earnings are anticipated to grow significantly at 31.2% annually, outpacing the Swiss market's growth of 11.2%. Despite trading at a substantial discount to its estimated fair value, Leonteq faces challenges with a volatile share price and unsustainable dividend coverage. The company’s revenue is expected to grow faster than the Swiss market but remains below significant growth levels. Recent presentations highlight continued investor engagement despite financial hurdles like low return on equity and debt coverage issues.

- Get an in-depth perspective on Leonteq's performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Leonteq is priced higher than what may be justified by its financials.

Qingdao Gon Technology (SZSE:002768)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Qingdao Gon Technology Co., Ltd. is involved in the R&D, production, and sale of modified plastic particles and functional plastic plates both domestically and internationally, with a market cap of CN¥6.38 billion.

Operations: Qingdao Gon Technology generates revenue through its activities in the research, development, production, and sale of modified plastic particles and functional plastic plates both within China and globally.

Insider Ownership: 15.3%

Earnings Growth Forecast: 29.6% p.a.

Qingdao Gon Technology is trading at a favorable price-to-earnings ratio of 11.7x, below the CN market average of 35.1x, suggesting good relative value. The company's earnings are projected to grow significantly at 29.6% annually, surpassing the broader market's growth rate of 25.1%. Recent earnings reports show revenue growth from CNY 12.67 billion to CNY 14.16 billion year-over-year, with net income rising from CNY 378.15 million to CNY 458.19 million, indicating robust financial performance despite an unstable dividend track record and low future return on equity forecasts.

- Click here to discover the nuances of Qingdao Gon Technology with our detailed analytical future growth report.

- Our expertly prepared valuation report Qingdao Gon Technology implies its share price may be lower than expected.

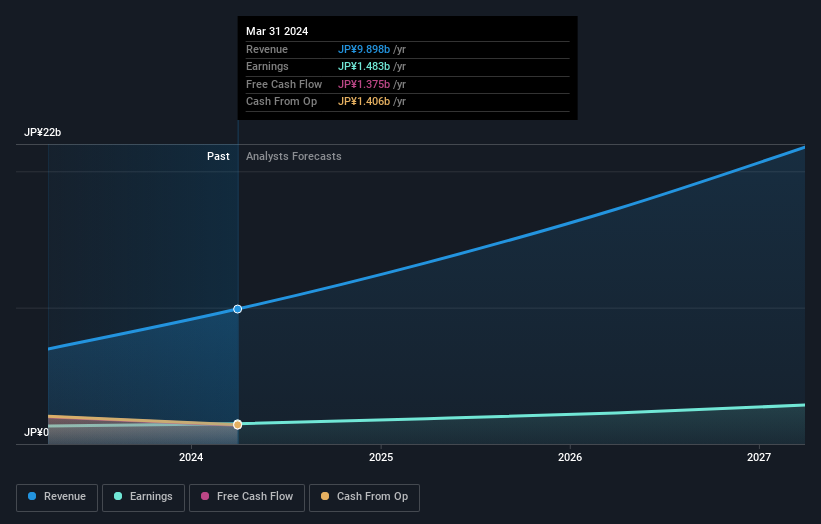

dely (TSE:299A)

Simply Wall St Growth Rating: ★★★★★★

Overview: Dely Inc. plans, develops, manages, and operates multiple smartphone apps and web media with a market cap of ¥46.64 billion.

Operations: The company's revenue primarily comes from its Platform Business, generating ¥9.90 billion.

Insider Ownership: 20.2%

Earnings Growth Forecast: 23.3% p.a.

dely inc. recently completed an IPO, raising ¥15.15 billion through a direct listing with sponsor backing, offering 12.63 million shares at ¥1,200 each. The company's earnings are forecast to grow significantly at 23.3% annually, outpacing the JP market's growth rate of 8.1%. Despite having less than three years of financial data and highly illiquid shares, dely inc.'s revenue is expected to grow robustly by 24.8% per year, exceeding market averages.

- Navigate through the intricacies of dely with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that dely's share price might be on the expensive side.

Summing It All Up

- Unlock more gems! Our Fast Growing Companies With High Insider Ownership screener has unearthed 1465 more companies for you to explore.Click here to unveil our expertly curated list of 1468 Fast Growing Companies With High Insider Ownership.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao Gon Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002768

Qingdao Gon Technology

Engages in the research and development, production, and sale of modified plastic particles and products, and functional plastic plates in China and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Community Narratives