Advertisement

- China

- /

- Metals and Mining

- /

- SZSE:002721

Global Penny Stocks Under US$2B Market Cap To Watch

Simply Wall St

Reviewed by Simply Wall St

Global markets have been navigating a mixed landscape, with small- and mid-cap indexes showing resilience amid ongoing trade discussions and economic uncertainties. As investors seek opportunities in this fluctuating environment, penny stocks emerge as an intriguing option. Despite their vintage name, these stocks often represent smaller or newer companies that can offer growth potential at lower price points when backed by strong financial health.

Top 10 Penny Stocks Globally

| Name | Share Price | Market Cap | Rewards & Risks |

| CNMC Goldmine Holdings (Catalist:5TP) | SGD0.395 | SGD160.09M | ✅ 4 ⚠️ 3 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD2.21 | SGD8.7B | ✅ 5 ⚠️ 0 View Analysis > |

| Angler Gaming (NGM:ANGL) | SEK3.71 | SEK278.19M | ✅ 5 ⚠️ 2 View Analysis > |

| SKP Resources Bhd (KLSE:SKPRES) | MYR1.04 | MYR1.62B | ✅ 5 ⚠️ 1 View Analysis > |

| NEXG Berhad (KLSE:NEXG) | MYR0.36 | MYR1.04B | ✅ 4 ⚠️ 3 View Analysis > |

| Lever Style (SEHK:1346) | HK$1.19 | HK$744.52M | ✅ 4 ⚠️ 2 View Analysis > |

| Goodbaby International Holdings (SEHK:1086) | HK$1.31 | HK$2.17B | ✅ 4 ⚠️ 2 View Analysis > |

| Warpaint London (AIM:W7L) | £3.97 | £320.73M | ✅ 4 ⚠️ 3 View Analysis > |

| Foresight Group Holdings (LSE:FSG) | £3.975 | £448.25M | ✅ 4 ⚠️ 1 View Analysis > |

| Bisalloy Steel Group (ASX:BIS) | A$3.35 | A$156.59M | ✅ 4 ⚠️ 1 View Analysis > |

Click here to see the full list of 5,648 stocks from our Global Penny Stocks screener.

Let's dive into some prime choices out of the screener.

Zhejiang Jihua Group (SHSE:603980)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Zhejiang Jihua Group Co., Ltd. operates in the dyestuff industry and has a market cap of CN¥3.05 billion.

Operations: Zhejiang Jihua Group Co., Ltd. does not report specific revenue segments.

Market Cap: CN¥3.05B

Zhejiang Jihua Group Co., Ltd. has shown a mixed financial performance, becoming profitable last year with revenues of CN¥1.64 billion, but experiencing a net loss in the recent quarter. Despite declining earnings over the past five years, its short-term assets significantly exceed both short and long-term liabilities, and it holds more cash than total debt. The company's stock is trading significantly below estimated fair value, yet its return on equity remains low at 1.1%. While not experiencing meaningful shareholder dilution recently, its dividend yield of 1.41% isn't well covered by earnings, indicating potential sustainability concerns.

- Navigate through the intricacies of Zhejiang Jihua Group with our comprehensive balance sheet health report here.

- Gain insights into Zhejiang Jihua Group's past trends and performance with our report on the company's historical track record.

Sundiro Holding (SZSE:000571)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Sundiro Holding Co., Ltd. operates in the coal industry both in China and internationally, with a market capitalization of CN¥4.01 billion.

Operations: Sundiro Holding Co., Ltd. has not reported any specific revenue segments.

Market Cap: CN¥4.01B

Sundiro Holding Co., Ltd. has faced financial challenges, with a significant decrease in quarterly sales to CN¥88.37 million from CN¥205.11 million the previous year and a net loss of CN¥33.4 million for the quarter ended March 31, 2025. Despite being unprofitable, the company has reduced its debt-to-equity ratio over five years and maintains more cash than total debt, indicating improved financial management. While short-term assets fall short of covering liabilities, Sundiro's experienced board and management team offer stability amidst volatility in earnings performance and shareholder value remains intact without recent dilution concerns.

- Click here and access our complete financial health analysis report to understand the dynamics of Sundiro Holding.

- Assess Sundiro Holding's previous results with our detailed historical performance reports.

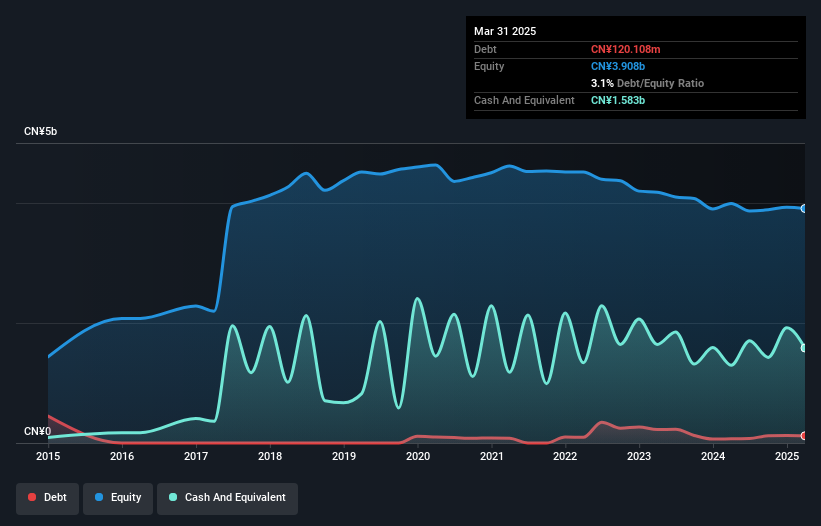

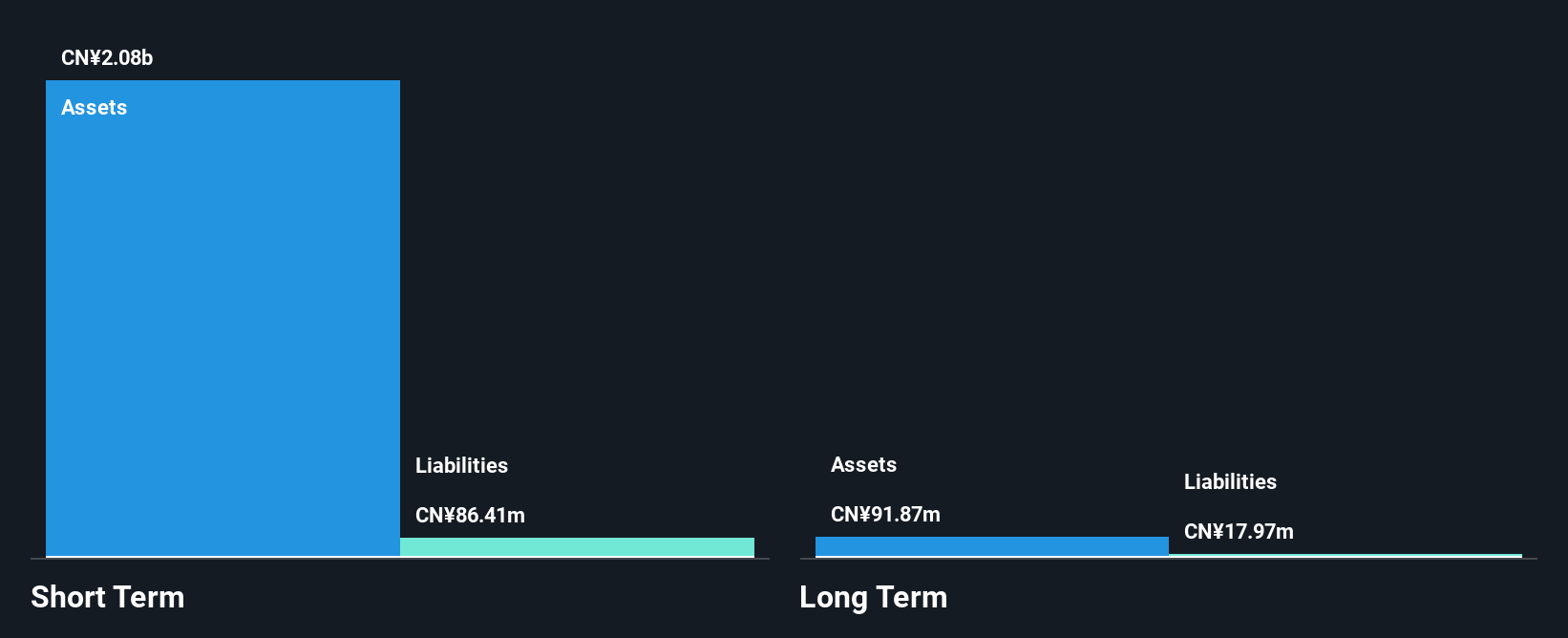

Beijing Kingee Culture Development (SZSE:002721)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Beijing Kingee Culture Development Co., Ltd. operates in the cultural and creative industries, with a market cap of CN¥7.26 billion.

Operations: Beijing Kingee Culture Development Co., Ltd. has not reported any specific revenue segments.

Market Cap: CN¥7.26B

Beijing Kingee Culture Development Co., Ltd. reported Q1 2025 sales of CN¥144.17 million, up from CN¥125.61 million a year ago, but posted a net loss of CN¥20.93 million compared to last year's net income of CN¥2.64 million, indicating financial challenges despite increased revenue. The company is debt-free and has reduced its debt-to-equity ratio from 144% five years ago to zero, showcasing improved financial health in that regard. With short-term assets covering both short- and long-term liabilities comfortably, the firm demonstrates solid liquidity management while maintaining shareholder value without dilution over the past year.

- Jump into the full analysis health report here for a deeper understanding of Beijing Kingee Culture Development.

- Explore historical data to track Beijing Kingee Culture Development's performance over time in our past results report.

Summing It All Up

- Dive into all 5,648 of the Global Penny Stocks we have identified here.

- Contemplating Other Strategies? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Kingee Culture Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002721

Beijing Kingee Culture Development

Engages in the research, design, development, and sale of gold jewelry under the Jinyi, Yuewang Jewelry, and Yue Wang Ancient Gold brands in China.

Flawless balance sheet with weak fundamentals.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative