- China

- /

- Metals and Mining

- /

- SZSE:000708

Is Citic Pacific Special Steel Group (SZSE:000708) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Citic Pacific Special Steel Group Co., Ltd (SZSE:000708) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Citic Pacific Special Steel Group

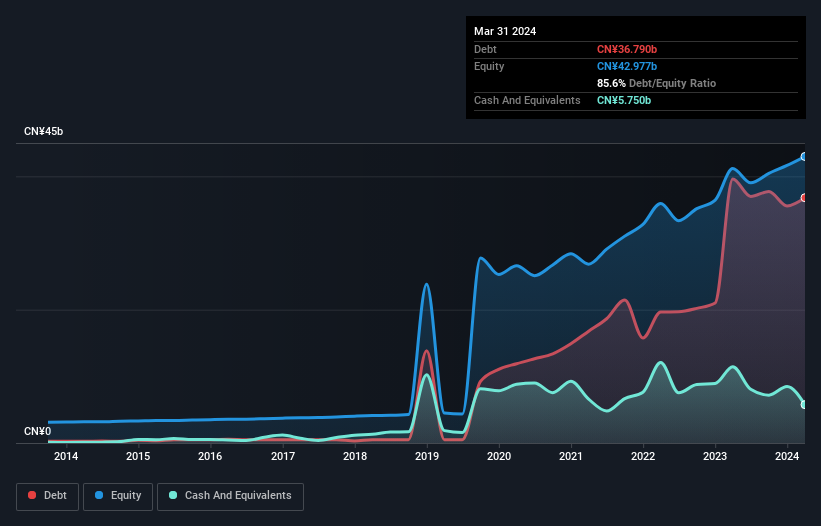

What Is Citic Pacific Special Steel Group's Debt?

As you can see below, Citic Pacific Special Steel Group had CN¥36.8b of debt at March 2024, down from CN¥39.6b a year prior. However, because it has a cash reserve of CN¥5.75b, its net debt is less, at about CN¥31.0b.

How Strong Is Citic Pacific Special Steel Group's Balance Sheet?

According to the last reported balance sheet, Citic Pacific Special Steel Group had liabilities of CN¥46.6b due within 12 months, and liabilities of CN¥24.4b due beyond 12 months. On the other hand, it had cash of CN¥5.75b and CN¥23.2b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥42.1b.

This deficit is considerable relative to its market capitalization of CN¥61.7b, so it does suggest shareholders should keep an eye on Citic Pacific Special Steel Group's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Citic Pacific Special Steel Group has net debt to EBITDA of 2.6 suggesting it uses a fair bit of leverage to boost returns. But the high interest coverage of 8.1 suggests it can easily service that debt. Sadly, Citic Pacific Special Steel Group's EBIT actually dropped 8.4% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Citic Pacific Special Steel Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Citic Pacific Special Steel Group actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

On our analysis Citic Pacific Special Steel Group's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. For example, its EBIT growth rate makes us a little nervous about its debt. When we consider all the factors mentioned above, we do feel a bit cautious about Citic Pacific Special Steel Group's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Citic Pacific Special Steel Group , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000708

Citic Pacific Special Steel Group

CITIC Pacific Special Steel Group Co., Ltd manufactures and sells steel materials in China.

Undervalued established dividend payer.

Market Insights

Community Narratives