Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:603315

Uncovering Liaoning Fu-An Heavy IndustryLtd And 2 More Small Cap Gems With Robust Metrics

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with tariff uncertainties and mixed economic indicators, small-cap stocks have been navigating a complex landscape. Despite the recent decline in major indices like the S&P 500 and Russell 2000, there are opportunities to be found in companies that demonstrate strong fundamentals and resilience amidst market volatility. In this climate, identifying stocks with robust financial metrics can be crucial for investors looking to capitalize on potential growth.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Nihon Parkerizing | 0.31% | 2.12% | 6.94% | ★★★★★★ |

| Ohashi Technica | NA | 4.58% | -14.04% | ★★★★★★ |

| Otec | 8.17% | 3.43% | 1.06% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Komori | 9.28% | 8.79% | 64.70% | ★★★★★☆ |

| CMC | 1.42% | 1.60% | 10.14% | ★★★★★☆ |

| Marusan Securities | 5.46% | 0.83% | 4.55% | ★★★★★☆ |

| Nippon Ski Resort DevelopmentLtd | 43.84% | 7.58% | 32.78% | ★★★★★☆ |

| Mr Max Holdings | 54.12% | 0.97% | 4.23% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

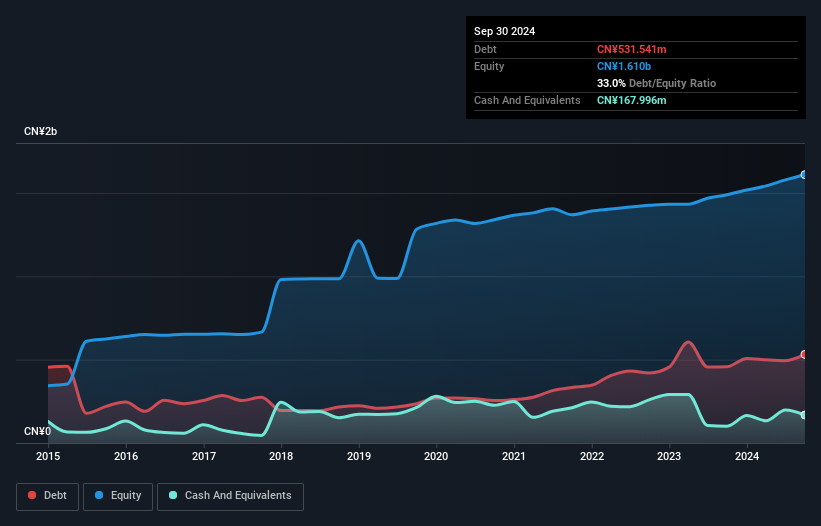

Liaoning Fu-An Heavy IndustryLtd (SHSE:603315)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Liaoning Fu-An Heavy Industry Co., Ltd specializes in the production and sale of steel castings in China, with a market capitalization of CN¥3.64 billion.

Operations: The company's primary revenue stream is from the production and sale of steel castings. It has a market capitalization of CN¥3.64 billion.

Liaoning Fu-An Heavy Industry, a smaller player in the metals and mining sector, has shown impressive earnings growth of 59.5% over the past year, outpacing the industry average of -2.3%. Despite this surge, its earnings have decreased by 13.1% annually over five years. The company's net debt to equity ratio stands at a satisfactory 22.6%, indicating manageable leverage levels. However, free cash flow remains negative, suggesting potential liquidity challenges despite profitability not being an immediate concern due to high-quality past earnings and sufficient interest coverage capabilities.

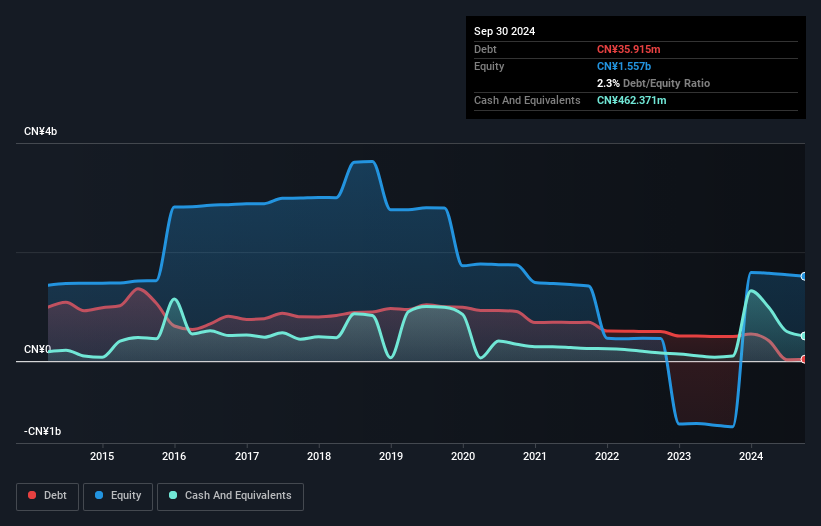

Shandong Oriental Ocean Sci-Tech (SZSE:002086)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shandong Oriental Ocean Sci-Tech Co., Ltd. operates in seawater seedling breeding, aquaculture, aquatic product processing, biotechnology, bonded warehousing, and logistics both in China and internationally with a market cap of CN¥4.99 billion.

Operations: The company's revenue streams are primarily derived from its diverse operations, including aquaculture and aquatic product processing. A significant portion of costs is associated with these core activities. The net profit margin has shown variability, reflecting changes in operational efficiency and market conditions.

Shandong Oriental Ocean Sci-Tech, a smaller player in its field, has made strides by becoming profitable this year. Its debt-to-equity ratio has impressively decreased from 35.5% to 2.3% over the past five years, indicating improved financial health. With a price-to-earnings ratio of 2.9x, it appears undervalued compared to the broader Chinese market's average of 36.7x. Despite its high-quality earnings and cash exceeding total debt, challenges remain with insufficient data on interest coverage by EBIT and negative free cash flow figures like -A$165 million recently reported as of September 2024, suggesting ongoing operational hurdles needing attention for sustained growth prospects.

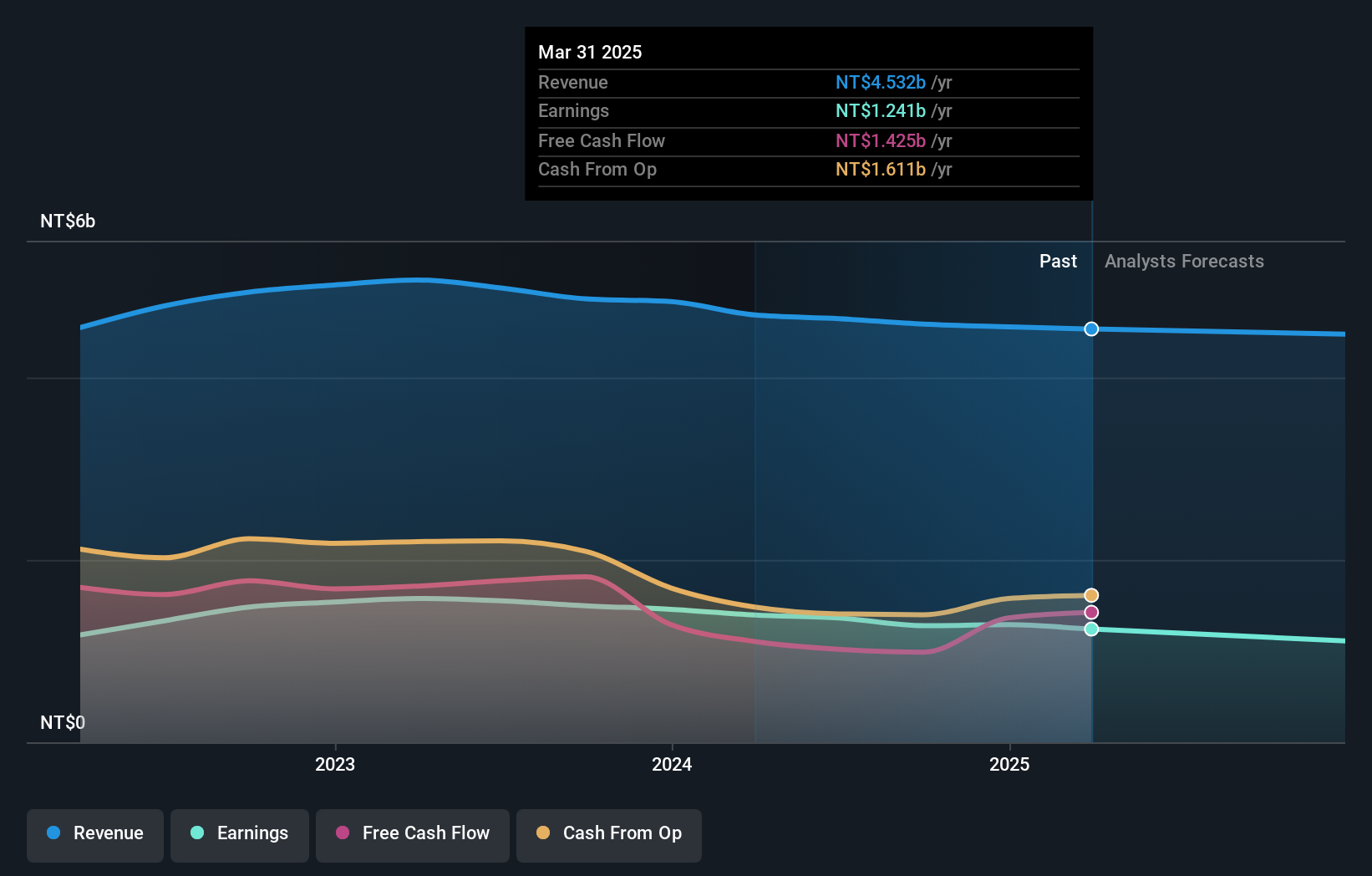

Sporton International (TPEX:6146)

Simply Wall St Value Rating: ★★★★★★

Overview: Sporton International Inc. offers product testing and certification services both in Taiwan and globally, with a market capitalization of approximately NT$20.98 billion.

Operations: Sporton International generates revenue primarily from testing, certification, and verification services amounting to NT$4.15 billion, alongside a smaller contribution from its Parts Division at NT$438.77 million. The company's financial performance is highlighted by its gross profit margin trends over recent periods.

Sporton International, a smaller player in the professional services sector, has demonstrated high-quality earnings despite facing challenges. The company is debt-free, which likely supports its strong financial position and allows it to focus on growth without interest burdens. However, recent negative earnings growth of 14.6% contrasts with an industry average of 10.3%. Its price-to-earnings ratio stands at 16.4x, undercutting the Taiwan market's average of 21.1x, suggesting potential value for investors seeking opportunities below market rates. While earnings are forecasted to grow at a rate of 6.82% annually, the upcoming special calls may provide further insights into future strategies and outlooks.

Taking Advantage

- Navigate through the entire inventory of 4690 Undiscovered Gems With Strong Fundamentals here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603315

Liaoning Fu-An Heavy IndustryLtd

Produces and sells steel castings in China.

Mediocre balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor