Investors Don't See Light At End Of Hengli Petrochemical Co.,Ltd.'s (SHSE:600346) Tunnel

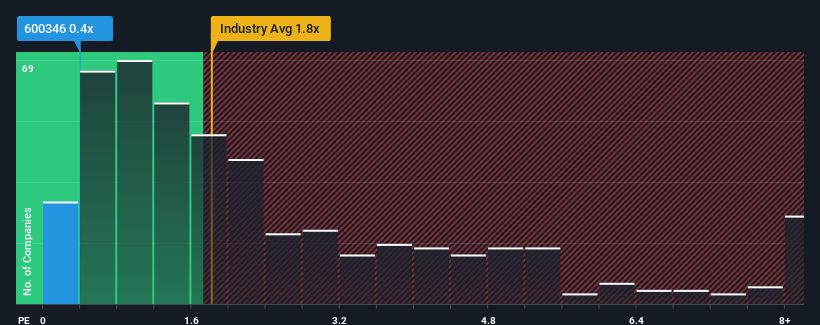

With a price-to-sales (or "P/S") ratio of 0.4x Hengli Petrochemical Co.,Ltd. (SHSE:600346) may be sending bullish signals at the moment, given that almost half of all the Chemicals companies in China have P/S ratios greater than 1.8x and even P/S higher than 4x are not unusual. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Hengli PetrochemicalLtd

What Does Hengli PetrochemicalLtd's Recent Performance Look Like?

Hengli PetrochemicalLtd certainly has been doing a good job lately as it's been growing revenue more than most other companies. One possibility is that the P/S ratio is low because investors think this strong revenue performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Hengli PetrochemicalLtd will help you uncover what's on the horizon.How Is Hengli PetrochemicalLtd's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Hengli PetrochemicalLtd's is when the company's growth is on track to lag the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 5.3% last year. The latest three year period has also seen an excellent 35% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next year should generate growth of 9.0% as estimated by the eleven analysts watching the company. With the industry predicted to deliver 24% growth, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Hengli PetrochemicalLtd's P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Hengli PetrochemicalLtd maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider and we've discovered 2 warning signs for Hengli PetrochemicalLtd (1 is a bit unpleasant!) that you should be aware of before investing here.

If these risks are making you reconsider your opinion on Hengli PetrochemicalLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Hengli PetrochemicalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600346

Hengli PetrochemicalLtd

Engages in petrochemical industry in China and internationally.

Undervalued with proven track record.

Market Insights

Community Narratives