Hengli PetrochemicalLtd's (SHSE:600346) Earnings Are Of Questionable Quality

Hengli Petrochemical Co.,Ltd.'s (SHSE:600346) stock was strong after they recently reported robust earnings. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

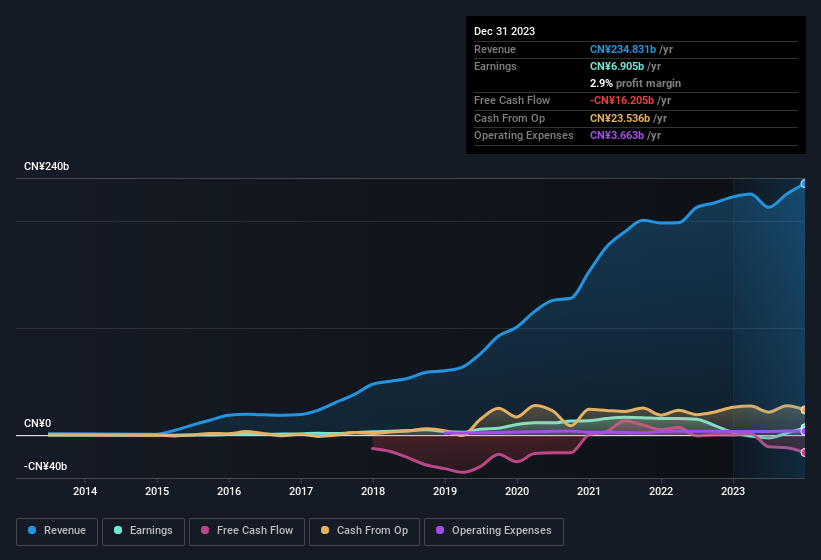

Check out our latest analysis for Hengli PetrochemicalLtd

How Do Unusual Items Influence Profit?

For anyone who wants to understand Hengli PetrochemicalLtd's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit gained from CN¥1.3b worth of unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. If Hengli PetrochemicalLtd doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Hengli PetrochemicalLtd's Profit Performance

Arguably, Hengli PetrochemicalLtd's statutory earnings have been distorted by unusual items boosting profit. Because of this, we think that it may be that Hengli PetrochemicalLtd's statutory profits are better than its underlying earnings power. The silver lining is that its EPS growth over the last year has been really wonderful, even if it's not a perfect measure. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Case in point: We've spotted 2 warning signs for Hengli PetrochemicalLtd you should be mindful of and 1 of them is a bit unpleasant.

This note has only looked at a single factor that sheds light on the nature of Hengli PetrochemicalLtd's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Hengli PetrochemicalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600346

Hengli PetrochemicalLtd

Engages in petrochemical industry in China and internationally.

Undervalued with proven track record.

Market Insights

Community Narratives