- China

- /

- Metals and Mining

- /

- SHSE:600117

Xining Special Steel.Co.,Ltd's (SHSE:600117) Business Is Trailing The Industry But Its Shares Aren't

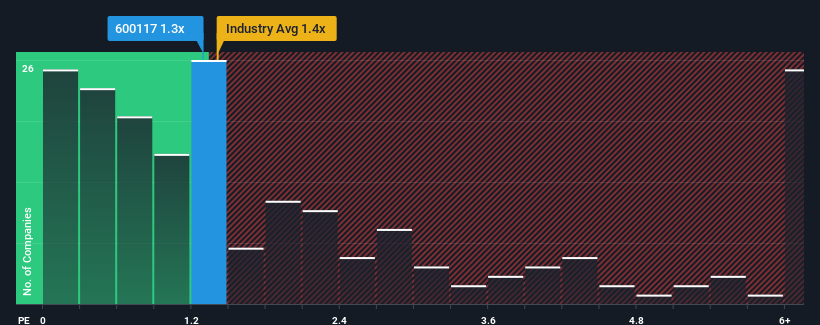

There wouldn't be many who think Xining Special Steel.Co.,Ltd's (SHSE:600117) price-to-sales (or "P/S") ratio of 1.3x is worth a mention when the median P/S for the Metals and Mining industry in China is similar at about 1.4x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for Xining Special Steel.Co.Ltd

What Does Xining Special Steel.Co.Ltd's P/S Mean For Shareholders?

With revenue growth that's exceedingly strong of late, Xining Special Steel.Co.Ltd has been doing very well. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Xining Special Steel.Co.Ltd will help you shine a light on its historical performance.What Are Revenue Growth Metrics Telling Us About The P/S?

Xining Special Steel.Co.Ltd's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 49%. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 53% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Comparing that to the industry, which is predicted to deliver 13% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this in mind, we find it worrying that Xining Special Steel.Co.Ltd's P/S exceeds that of its industry peers. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What Does Xining Special Steel.Co.Ltd's P/S Mean For Investors?

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look at Xining Special Steel.Co.Ltd revealed its shrinking revenues over the medium-term haven't impacted the P/S as much as we anticipated, given the industry is set to grow. Even though it matches the industry, we're uncomfortable with the current P/S ratio, as this dismal revenue performance is unlikely to support a more positive sentiment for long. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for Xining Special Steel.Co.Ltd that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600117

Xining Special Steel.Co.Ltd

Engages in the smelting, rolling, and processing of special steel products in China.

Acceptable track record and slightly overvalued.

Market Insights

Community Narratives