- China

- /

- Healthcare Services

- /

- SHSE:600829

Is HPGC Renmintongtai Pharmaceutical (SHSE:600829) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, HPGC Renmintongtai Pharmaceutical Corporation (SHSE:600829) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for HPGC Renmintongtai Pharmaceutical

What Is HPGC Renmintongtai Pharmaceutical's Net Debt?

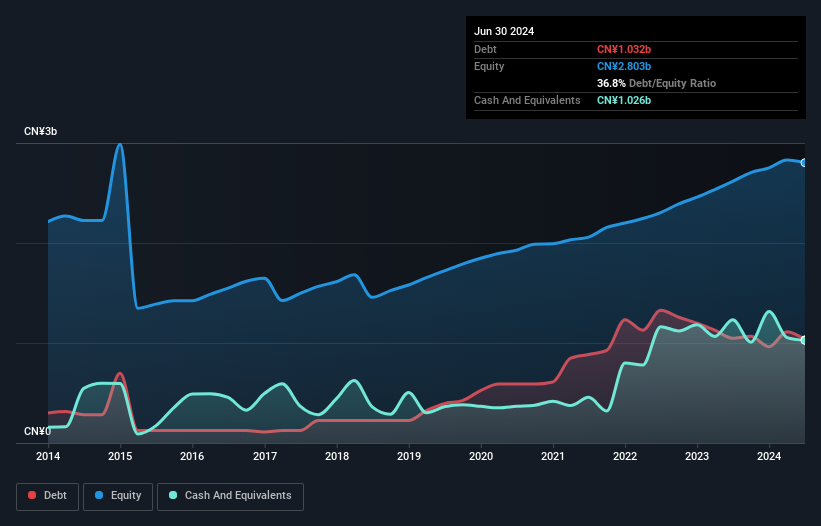

The chart below, which you can click on for greater detail, shows that HPGC Renmintongtai Pharmaceutical had CN¥1.03b in debt in June 2024; about the same as the year before. However, because it has a cash reserve of CN¥1.03b, its net debt is less, at about CN¥5.86m.

How Healthy Is HPGC Renmintongtai Pharmaceutical's Balance Sheet?

The latest balance sheet data shows that HPGC Renmintongtai Pharmaceutical had liabilities of CN¥4.23b due within a year, and liabilities of CN¥154.7m falling due after that. On the other hand, it had cash of CN¥1.03b and CN¥4.54b worth of receivables due within a year. So it can boast CN¥1.18b more liquid assets than total liabilities.

This surplus strongly suggests that HPGC Renmintongtai Pharmaceutical has a rock-solid balance sheet (and the debt is of no concern whatsoever). Having regard to this fact, we think its balance sheet is as strong as an ox. Carrying virtually no net debt, HPGC Renmintongtai Pharmaceutical has a very light debt load indeed.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

HPGC Renmintongtai Pharmaceutical has barely any net debt, as demonstrated by its net debt to EBITDA ratio of only 0.015. Humorously, it actually received more in interest over the last twelve months than it had to pay. So there's no doubt this company can take on debt as easily as enthusiastic spray-tanners take on an orange hue. On the other hand, HPGC Renmintongtai Pharmaceutical's EBIT dived 15%, over the last year. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. There's no doubt that we learn most about debt from the balance sheet. But it is HPGC Renmintongtai Pharmaceutical's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, HPGC Renmintongtai Pharmaceutical created free cash flow amounting to 19% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Happily, HPGC Renmintongtai Pharmaceutical's impressive interest cover implies it has the upper hand on its debt. But the stark truth is that we are concerned by its EBIT growth rate. It's also worth noting that HPGC Renmintongtai Pharmaceutical is in the Healthcare industry, which is often considered to be quite defensive. Looking at all the aforementioned factors together, it strikes us that HPGC Renmintongtai Pharmaceutical can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example - HPGC Renmintongtai Pharmaceutical has 2 warning signs we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if HPGC Renmintongtai Pharmaceutical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600829

HPGC Renmintongtai Pharmaceutical

Engages in the wholesale and retail of pharmaceutical products in China.

Adequate balance sheet second-rate dividend payer.