Shanghai Xuerong Biotechnology Co.,Ltd.'s (SZSE:300511) Shares Bounce 25% But Its Business Still Trails The Industry

Those holding Shanghai Xuerong Biotechnology Co.,Ltd. (SZSE:300511) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 41% over that time.

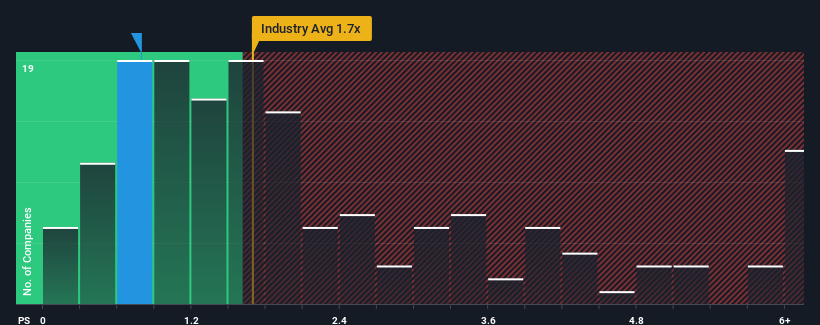

In spite of the firm bounce in price, Shanghai Xuerong BiotechnologyLtd may still be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.8x, since almost half of all companies in the Food industry in China have P/S ratios greater than 1.7x and even P/S higher than 4x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Shanghai Xuerong BiotechnologyLtd

What Does Shanghai Xuerong BiotechnologyLtd's P/S Mean For Shareholders?

The revenue growth achieved at Shanghai Xuerong BiotechnologyLtd over the last year would be more than acceptable for most companies. One possibility is that the P/S is low because investors think this respectable revenue growth might actually underperform the broader industry in the near future. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Shanghai Xuerong BiotechnologyLtd will help you shine a light on its historical performance.Is There Any Revenue Growth Forecasted For Shanghai Xuerong BiotechnologyLtd?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Shanghai Xuerong BiotechnologyLtd's to be considered reasonable.

Retrospectively, the last year delivered a decent 14% gain to the company's revenues. Revenue has also lifted 18% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 16% shows it's noticeably less attractive.

With this in consideration, it's easy to understand why Shanghai Xuerong BiotechnologyLtd's P/S falls short of the mark set by its industry peers. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

The Final Word

Shanghai Xuerong BiotechnologyLtd's stock price has surged recently, but its but its P/S still remains modest. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Shanghai Xuerong BiotechnologyLtd revealed its three-year revenue trends are contributing to its low P/S, given they look worse than current industry expectations. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. If recent medium-term revenue trends continue, it's hard to see the share price experience a reversal of fortunes anytime soon.

Before you settle on your opinion, we've discovered 2 warning signs for Shanghai Xuerong BiotechnologyLtd that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300511

Shanghai Xuerong BiotechnologyLtd

Engages in the research and development, industrial planting, and sale of fresh edible mushrooms in the People’s Republic of China.

Slightly overvalued very low.

Market Insights

Community Narratives