Advertisement

Guilin Layn Natural Ingredients Corp.'s (SZSE:002166) 31% Cheaper Price Remains In Tune With Earnings

The Guilin Layn Natural Ingredients Corp. (SZSE:002166) share price has softened a substantial 31% over the previous 30 days, handing back much of the gains the stock has made lately. Longer-term shareholders will rue the drop in the share price, since it's now virtually flat for the year after a promising few quarters.

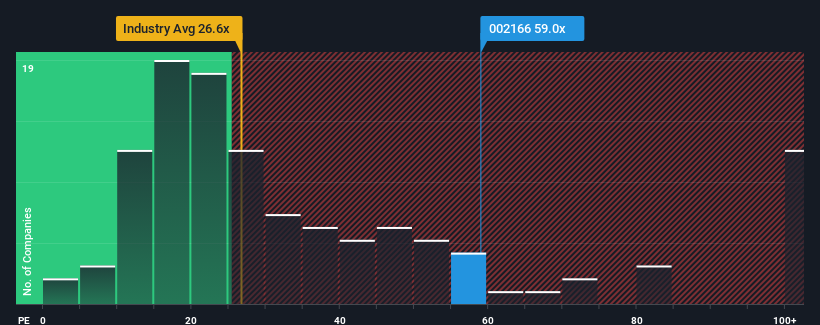

Although its price has dipped substantially, given close to half the companies in China have price-to-earnings ratios (or "P/E's") below 30x, you may still consider Guilin Layn Natural Ingredients as a stock to avoid entirely with its 59x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Guilin Layn Natural Ingredients hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for Guilin Layn Natural Ingredients

Does Growth Match The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Guilin Layn Natural Ingredients' is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 52% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 24% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 55% per year during the coming three years according to the only analyst following the company. With the market only predicted to deliver 25% per year, the company is positioned for a stronger earnings result.

With this information, we can see why Guilin Layn Natural Ingredients is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Guilin Layn Natural Ingredients' shares may have retreated, but its P/E is still flying high. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Guilin Layn Natural Ingredients' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

You should always think about risks. Case in point, we've spotted 4 warning signs for Guilin Layn Natural Ingredients you should be aware of, and 1 of them is a bit unpleasant.

You might be able to find a better investment than Guilin Layn Natural Ingredients. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002166

Guilin Layn Natural Ingredients

Produces and sells plant extracts and natural flavors in China and internationally.

High growth potential with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor