Zhejiang Wufangzhai Industry's (SHSE:603237) Earnings Are Weaker Than They Seem

Zhejiang Wufangzhai Industry Co., Ltd.'s (SHSE:603237) robust earnings report didn't manage to move the market for its stock. Our analysis suggests that shareholders have noticed something concerning in the numbers.

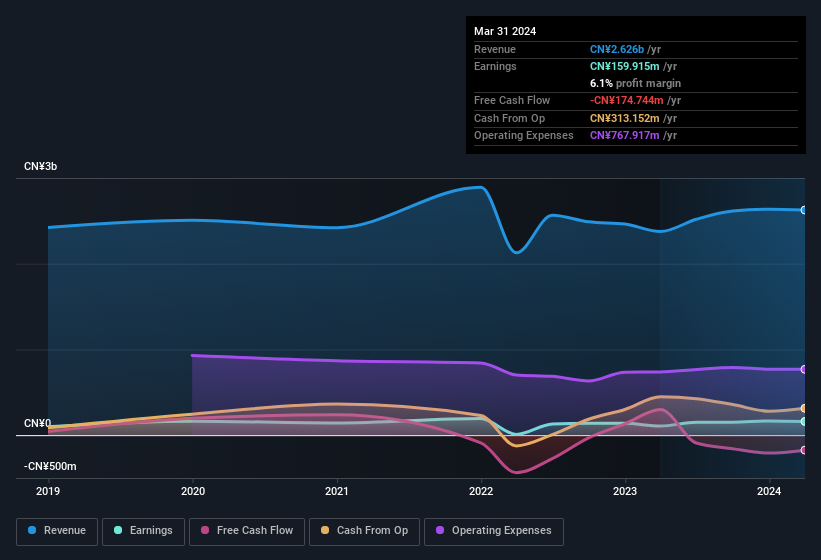

See our latest analysis for Zhejiang Wufangzhai Industry

Examining Cashflow Against Zhejiang Wufangzhai Industry's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Over the twelve months to March 2024, Zhejiang Wufangzhai Industry recorded an accrual ratio of 0.41. As a general rule, that bodes poorly for future profitability. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of CN¥175m, in contrast to the aforementioned profit of CN¥159.9m. It's worth noting that Zhejiang Wufangzhai Industry generated positive FCF of CN¥300m a year ago, so at least they've done it in the past. The good news for shareholders is that Zhejiang Wufangzhai Industry's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. As a result, some shareholders may be looking for stronger cash conversion in the current year.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Zhejiang Wufangzhai Industry's Profit Performance

As we have made quite clear, we're a bit worried that Zhejiang Wufangzhai Industry didn't back up the last year's profit with free cashflow. For this reason, we think that Zhejiang Wufangzhai Industry's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. The good news is that, its earnings per share increased by 36% in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. If you'd like to know more about Zhejiang Wufangzhai Industry as a business, it's important to be aware of any risks it's facing. Every company has risks, and we've spotted 1 warning sign for Zhejiang Wufangzhai Industry you should know about.

This note has only looked at a single factor that sheds light on the nature of Zhejiang Wufangzhai Industry's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you're looking to trade Zhejiang Wufangzhai Industry, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Zhejiang Wufangzhai Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603237

Flawless balance sheet with proven track record and pays a dividend.

Market Insights

Community Narratives