- China

- /

- Energy Services

- /

- SZSE:300471

Houpu Clean Energy Group Co., Ltd.'s (SZSE:300471) Share Price Is Still Matching Investor Opinion Despite 25% Slump

Houpu Clean Energy Group Co., Ltd. (SZSE:300471) shareholders won't be pleased to see that the share price has had a very rough month, dropping 25% and undoing the prior period's positive performance. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 35% in that time.

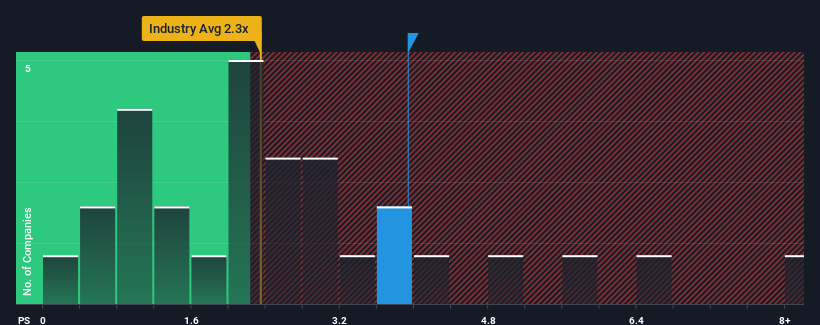

Although its price has dipped substantially, given close to half the companies operating in China's Energy Services industry have price-to-sales ratios (or "P/S") below 2.3x, you may still consider Houpu Clean Energy Group as a stock to potentially avoid with its 3.9x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for Houpu Clean Energy Group

How Houpu Clean Energy Group Has Been Performing

Recent times have been quite advantageous for Houpu Clean Energy Group as its revenue has been rising very briskly. The P/S ratio is probably high because investors think this strong revenue growth will be enough to outperform the broader industry in the near future. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Houpu Clean Energy Group will help you shine a light on its historical performance.How Is Houpu Clean Energy Group's Revenue Growth Trending?

In order to justify its P/S ratio, Houpu Clean Energy Group would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 31% last year. Pleasingly, revenue has also lifted 96% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 15% shows it's noticeably more attractive.

With this information, we can see why Houpu Clean Energy Group is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Final Word

There's still some elevation in Houpu Clean Energy Group's P/S, even if the same can't be said for its share price recently. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

It's no surprise that Houpu Clean Energy Group can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 2 warning signs for Houpu Clean Energy Group that we have uncovered.

If you're unsure about the strength of Houpu Clean Energy Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Houpu Clean Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300471

Excellent balance sheet with weak fundamentals.

Similar Companies

Market Insights

Community Narratives