- China

- /

- Energy Services

- /

- SZSE:002207

Xinjiang Zhundong Petroleum Technology Co., Ltd. (SZSE:002207) Stock Rockets 26% As Investors Are Less Pessimistic Than Expected

Those holding Xinjiang Zhundong Petroleum Technology Co., Ltd. (SZSE:002207) shares would be relieved that the share price has rebounded 26% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 6.7% in the last twelve months.

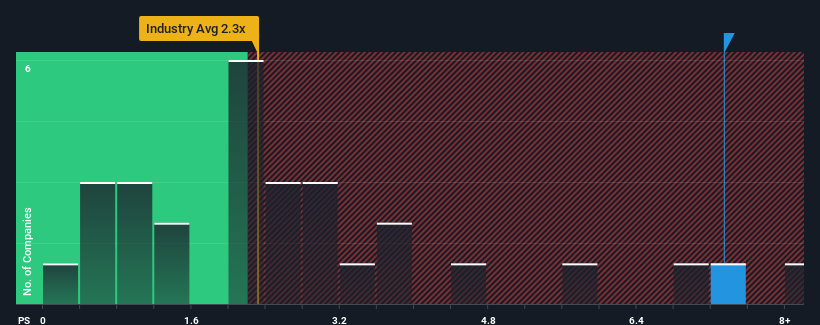

Since its price has surged higher, you could be forgiven for thinking Xinjiang Zhundong Petroleum Technology is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 7.3x, considering almost half the companies in China's Energy Services industry have P/S ratios below 2.3x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Xinjiang Zhundong Petroleum Technology

How Has Xinjiang Zhundong Petroleum Technology Performed Recently?

The revenue growth achieved at Xinjiang Zhundong Petroleum Technology over the last year would be more than acceptable for most companies. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Xinjiang Zhundong Petroleum Technology will help you shine a light on its historical performance.How Is Xinjiang Zhundong Petroleum Technology's Revenue Growth Trending?

Xinjiang Zhundong Petroleum Technology's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 16%. Although, its longer-term performance hasn't been as strong with three-year revenue growth being relatively non-existent overall. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 19% shows it's noticeably less attractive.

With this information, we find it concerning that Xinjiang Zhundong Petroleum Technology is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

Shares in Xinjiang Zhundong Petroleum Technology have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

The fact that Xinjiang Zhundong Petroleum Technology currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Xinjiang Zhundong Petroleum Technology, and understanding should be part of your investment process.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002207

Xinjiang Zhundong Petroleum Technology

Xinjiang Zhundong Petroleum Technology Co., Ltd.

Mediocre balance sheet minimal.

Market Insights

Community Narratives