- China

- /

- Capital Markets

- /

- SHSE:601696

Investor Optimism Abounds BOC International (China) CO., LTD. (SHSE:601696) But Growth Is Lacking

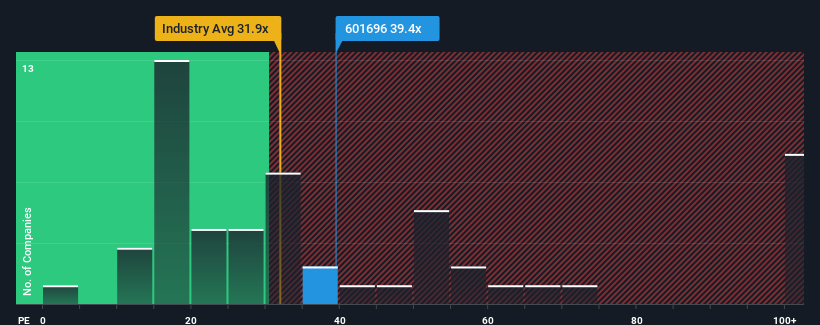

With a median price-to-earnings (or "P/E") ratio of close to 37x in China, you could be forgiven for feeling indifferent about BOC International (China) CO., LTD.'s (SHSE:601696) P/E ratio of 39.4x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

With earnings that are retreating more than the market's of late, BOC International (China) has been very sluggish. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders may be a little nervous about the viability of the share price.

View our latest analysis for BOC International (China)

How Is BOC International (China)'s Growth Trending?

In order to justify its P/E ratio, BOC International (China) would need to produce growth that's similar to the market.

Retrospectively, the last year delivered a frustrating 10% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 23% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 20% during the coming year according to the one analyst following the company. Meanwhile, the rest of the market is forecast to expand by 37%, which is noticeably more attractive.

In light of this, it's curious that BOC International (China)'s P/E sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of BOC International (China)'s analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Before you settle on your opinion, we've discovered 1 warning sign for BOC International (China) that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if BOC International (China) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601696

BOC International (China)

Provides investment banking and securities services in the People’s Republic of China.

Excellent balance sheet unattractive dividend payer.

Market Insights

Community Narratives