Advertisement

- China

- /

- Consumer Durables

- /

- SZSE:000921

Hisense Home Appliances Group Co., Ltd. (SZSE:000921) Not Doing Enough For Some Investors As Its Shares Slump 26%

Hisense Home Appliances Group Co., Ltd. (SZSE:000921) shareholders won't be pleased to see that the share price has had a very rough month, dropping 26% and undoing the prior period's positive performance. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 18%.

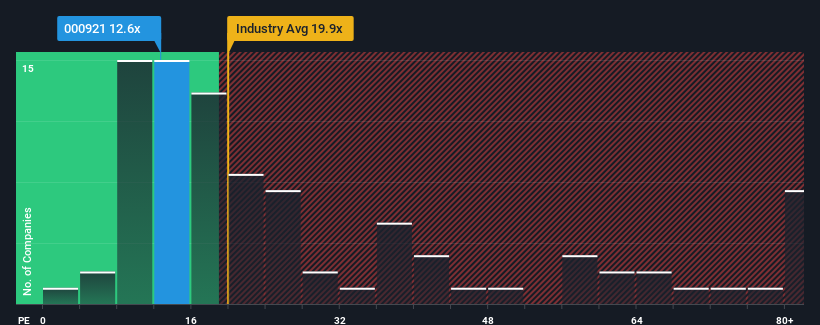

Following the heavy fall in price, Hisense Home Appliances Group may be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 12.6x, since almost half of all companies in China have P/E ratios greater than 29x and even P/E's higher than 54x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Hisense Home Appliances Group as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Hisense Home Appliances Group

How Is Hisense Home Appliances Group's Growth Trending?

In order to justify its P/E ratio, Hisense Home Appliances Group would need to produce anemic growth that's substantially trailing the market.

If we review the last year of earnings growth, the company posted a terrific increase of 81%. The latest three year period has also seen an excellent 80% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 10% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 25% per annum growth forecast for the broader market.

In light of this, it's understandable that Hisense Home Appliances Group's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Hisense Home Appliances Group's P/E?

Having almost fallen off a cliff, Hisense Home Appliances Group's share price has pulled its P/E way down as well. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Hisense Home Appliances Group maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Hisense Home Appliances Group that you need to be mindful of.

If these risks are making you reconsider your opinion on Hisense Home Appliances Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Hisense Home Appliances Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:000921

Hisense Home Appliances Group

Engages in the manufacture and sale of household electrical appliances under the Hisense, Ronshen, Kelon, Hitachi, gorenge, ASKO, and York brands in the People’s Republic of China and internationally.

Very undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor