Discovering Undiscovered Gems with Strong Potential in December 2024

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by interest rate adjustments and mixed economic indicators, small-cap stocks have faced particular challenges, with the Russell 2000 Index underperforming larger indices. In this environment, identifying stocks with strong fundamentals and growth potential becomes crucial for investors seeking opportunities amidst broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Marítima de Inversiones | NA | 82.67% | 21.14% | ★★★★★★ |

| Bahrain National Holding Company B.S.C | NA | 20.11% | 5.44% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Forest Packaging GroupLtd | 17.72% | 2.87% | -6.03% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Insurance Group (B.S.C.) | NA | -59.20% | 20.33% | ★★★★★☆ |

| Elite Color Environmental Resources Science & Technology | 30.80% | 12.99% | 1.83% | ★★★★★☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| La Positiva Seguros y Reaseguros | 0.04% | 8.44% | 27.31% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

HMT (Xiamen) New Technical Materials (SHSE:603306)

Simply Wall St Value Rating: ★★★★★☆

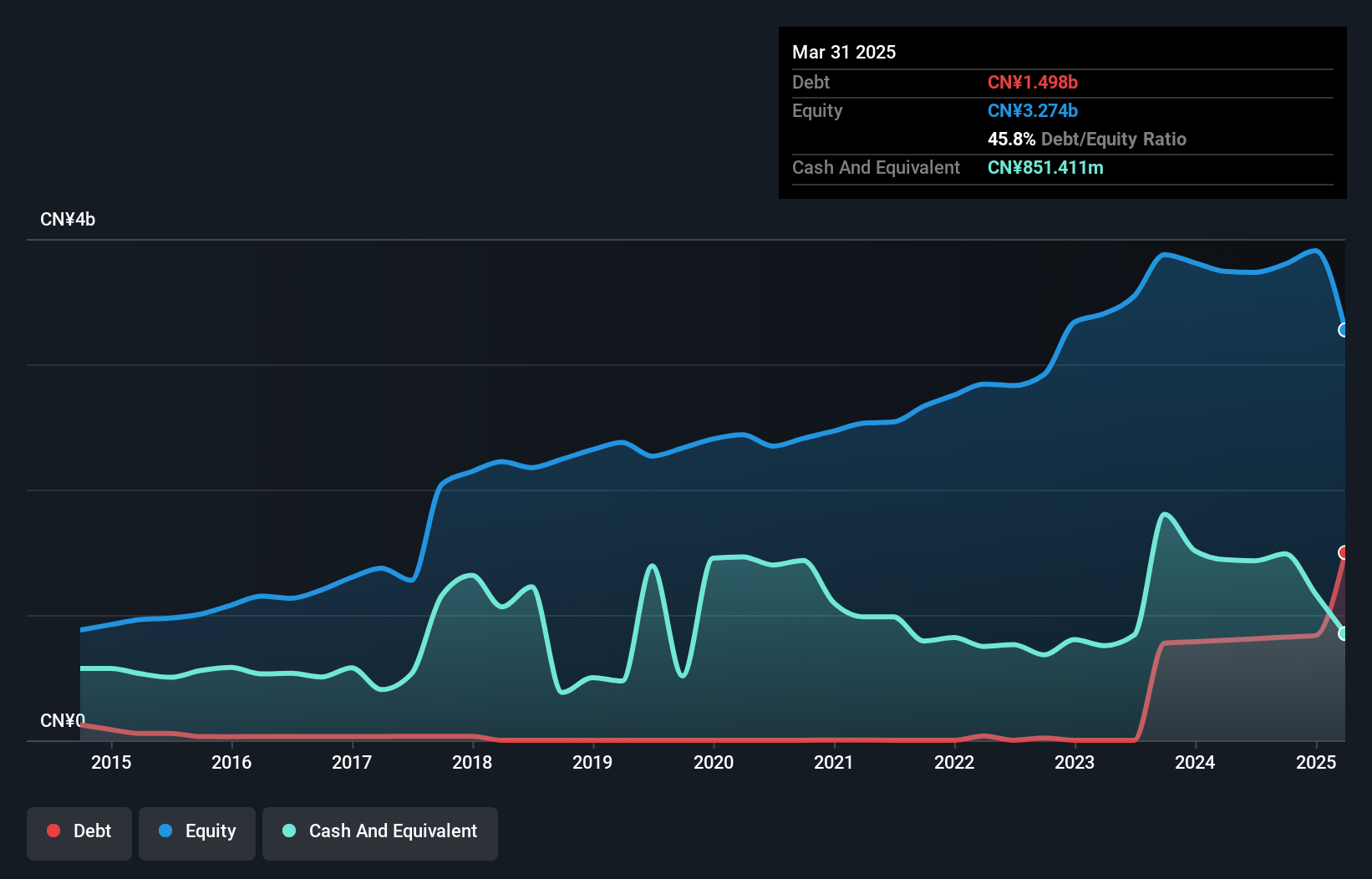

Overview: HMT (Xiamen) New Technical Materials Co., Ltd. is involved in the automobile parts manufacturing industry and has a market capitalization of CN¥9.31 billion.

Operations: HMT (Xiamen) New Technical Materials generates revenue primarily from its automobile parts manufacturing segment, amounting to CN¥2.14 billion. The company's market capitalization is CN¥9.31 billion.

HMT (Xiamen) New Technical Materials, a company with a market presence in the luxury industry, has shown robust performance with earnings growing 30% over the past year, outpacing the industry's 3.3%. The firm reported net income of CNY 196 million for nine months ending September 2024, up from CNY 149 million previously. With high-quality earnings and trading at approximately two-thirds below its estimated fair value, HMT seems undervalued. Despite an increase in debt to equity ratio to 21.7% over five years, its interest payments are well covered by EBIT at a multiple of 109.4 times.

- Delve into the full analysis health report here for a deeper understanding of HMT (Xiamen) New Technical Materials.

Learn about HMT (Xiamen) New Technical Materials' historical performance.

Shin-Etsu PolymerLtd (TSE:7970)

Simply Wall St Value Rating: ★★★★★★

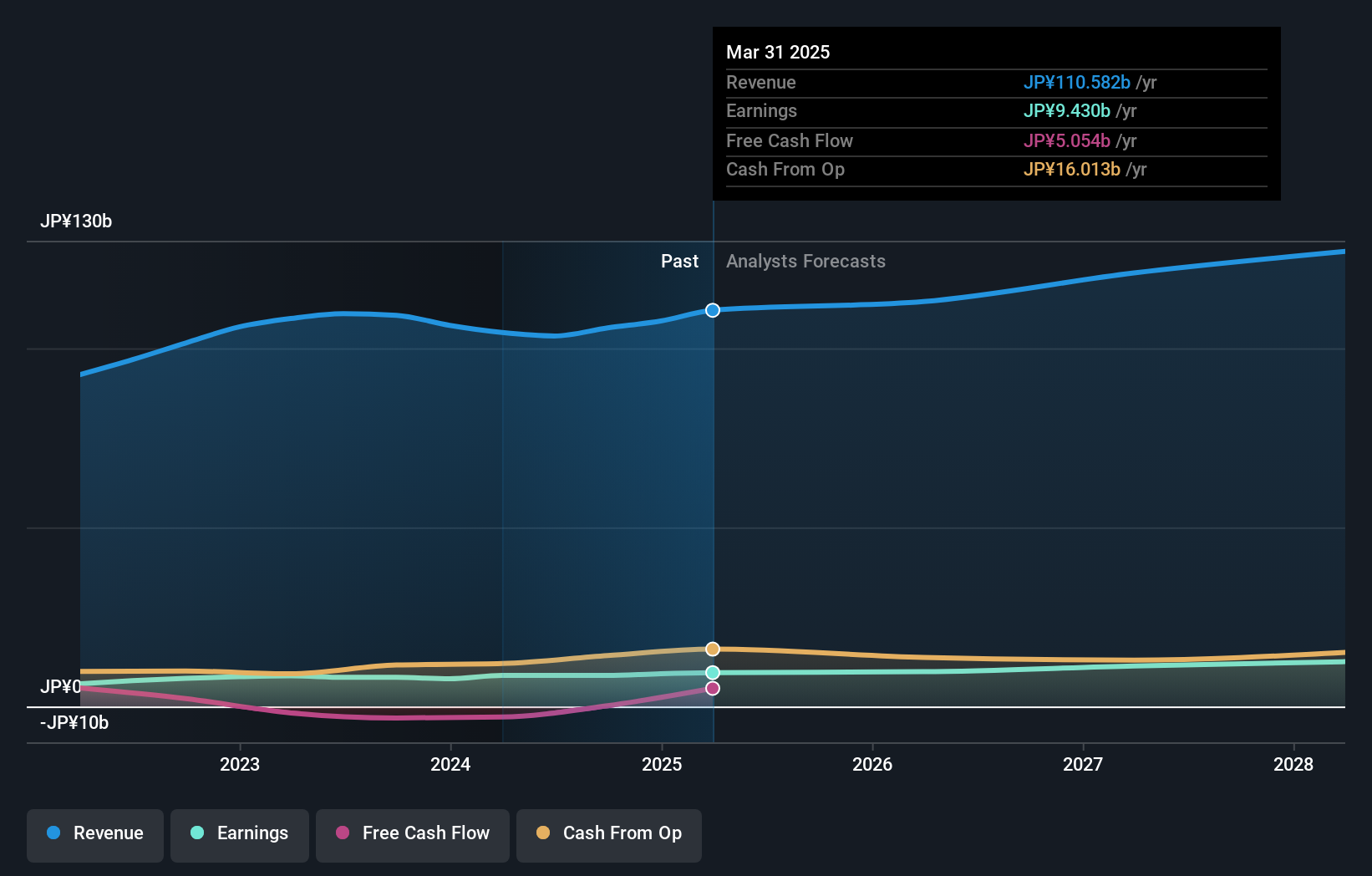

Overview: Shin-Etsu Polymer Co., Ltd. is a global manufacturer and seller of polyvinyl chloride (PVC) products, with a market capitalization of ¥126.46 billion.

Operations: Shin-Etsu Polymer generates revenue primarily from its Precision Molded Product segment, which accounts for ¥50.10 billion, followed by the Electronic Device segment at ¥26.05 billion. The company's net profit margin reflects its profitability after accounting for all expenses and taxes.

Shin-Etsu Polymer, a nimble player in the market, has shown impressive financial health with high-quality earnings and no debt burden over the past five years. The company's earnings have increased by 10.5% annually, though recent growth of 6.6% lagged behind the broader Chemicals industry at 14%. Trading at a substantial discount of 62.6% to its estimated fair value suggests potential upside for investors. A recent share repurchase program completed in December saw the company buy back 500,000 shares for ¥809 million, indicating strategic capital allocation and confidence in its own valuation.

Matsuya Foods Holdings (TSE:9887)

Simply Wall St Value Rating: ★★★★★☆

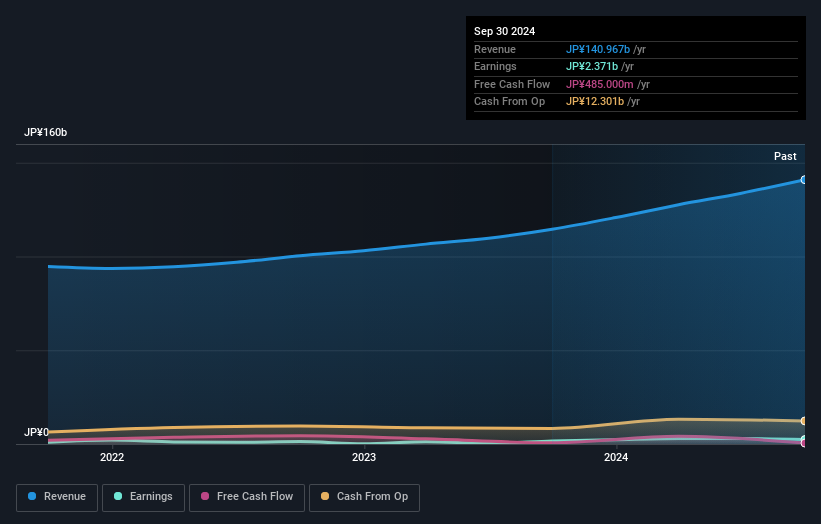

Overview: Matsuya Foods Holdings Co., Ltd. owns and operates restaurants in Japan, China, and Taiwan, with a market capitalization of ¥1.29 billion.

Operations: The primary revenue stream for Matsuya Foods Holdings comes from its Food and Beverage Business, generating ¥140.97 billion. The company's financial performance includes a focus on managing costs to influence profitability, with particular attention to the net profit margin trends over time.

Matsuya Foods Holdings, a small player in the hospitality sector, has demonstrated impressive earnings growth of 45.5% over the past year, outpacing the industry average of 24.5%. The company's net debt to equity ratio stands at 25.7%, which is considered satisfactory and indicates a balanced approach to leveraging debt. Additionally, Matsuya's interest payments are well covered by EBIT with a coverage ratio of 48.3x, highlighting its strong ability to manage debt obligations. Despite an increase in its debt to equity ratio from 26.2% to 59.6% over five years, Matsuya remains free cash flow positive and continues to show resilience in its financial strategy.

- Unlock comprehensive insights into our analysis of Matsuya Foods Holdings stock in this health report.

Assess Matsuya Foods Holdings' past performance with our detailed historical performance reports.

Summing It All Up

- Unlock more gems! Our Undiscovered Gems With Strong Fundamentals screener has unearthed 4499 more companies for you to explore.Click here to unveil our expertly curated list of 4502 Undiscovered Gems With Strong Fundamentals.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7970

Shin-Etsu PolymerLtd

Manufactures and sells polyvinyl chloride (PVC) products worldwide.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives