Advertisement

Zhejiang Cfmoto Power Co.,Ltd (SHSE:603129) Held Back By Insufficient Growth Even After Shares Climb 30%

Zhejiang Cfmoto Power Co.,Ltd (SHSE:603129) shareholders have had their patience rewarded with a 30% share price jump in the last month. The last 30 days bring the annual gain to a very sharp 98%.

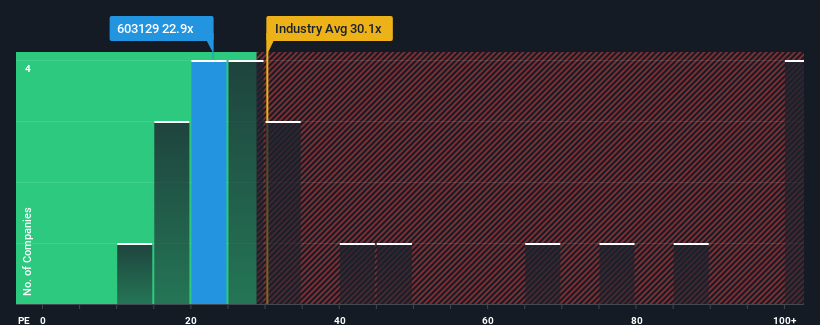

In spite of the firm bounce in price, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 35x, you may still consider Zhejiang Cfmoto PowerLtd as an attractive investment with its 22.9x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Zhejiang Cfmoto PowerLtd as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Zhejiang Cfmoto PowerLtd

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Zhejiang Cfmoto PowerLtd's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered an exceptional 37% gain to the company's bottom line. Pleasingly, EPS has also lifted 189% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the nine analysts covering the company suggest earnings should grow by 26% over the next year. That's shaping up to be materially lower than the 38% growth forecast for the broader market.

In light of this, it's understandable that Zhejiang Cfmoto PowerLtd's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Despite Zhejiang Cfmoto PowerLtd's shares building up a head of steam, its P/E still lags most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Zhejiang Cfmoto PowerLtd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Zhejiang Cfmoto PowerLtd with six simple checks will allow you to discover any risks that could be an issue.

Of course, you might also be able to find a better stock than Zhejiang Cfmoto PowerLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Cfmoto PowerLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603129

Zhejiang Cfmoto PowerLtd

Engages in the development, manufacture, marketing, and delivery of motorcycles, off-road vehicles, engines, frames, parts, apparel, and accessories in China, rest of Asia, North America, Oceania, Africa, South America, and Europe.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor