Advertisement

- China

- /

- Electrical

- /

- SHSE:605117

3 Asian Stocks That Might Be Trading At A Discount Of Up To 29.4%

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate mixed economic signals, including a weakening U.S. labor market and varying performances in key indices, attention turns to Asia where stock valuations may present intriguing opportunities. For investors looking for potential bargains amid these shifting conditions, identifying undervalued stocks can be appealing as they might offer significant upside when the broader market stabilizes or improves.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zhejiang Century Huatong GroupLtd (SZSE:002602) | CN¥18.86 | CN¥37.07 | 49.1% |

| Walvax Biotechnology (SZSE:300142) | CN¥12.25 | CN¥24.48 | 50% |

| Suzhou Alton Electrical & Mechanical Industry (SZSE:301187) | CN¥29.10 | CN¥58.19 | 50% |

| SRE Holdings (TSE:2980) | ¥3295.00 | ¥6563.07 | 49.8% |

| Pansoft (SZSE:300996) | CN¥17.14 | CN¥34.20 | 49.9% |

| Meitu (SEHK:1357) | HK$9.03 | HK$18.01 | 49.9% |

| Kuraray (TSE:3405) | ¥1774.50 | ¥3497.71 | 49.3% |

| Kolmar Korea (KOSE:A161890) | ₩78400.00 | ₩154965.83 | 49.4% |

| Japan Data Science ConsortiumLtd (TSE:4418) | ¥988.00 | ¥1944.67 | 49.2% |

| HL Holdings (KOSE:A060980) | ₩41900.00 | ₩82588.45 | 49.3% |

Let's take a closer look at a couple of our picks from the screened companies.

Sanil Electric (KOSE:A062040)

Overview: Sanil Electric Co., Ltd. manufactures and sells transformers in Korea and internationally, with a market cap of ₩3.42 billion.

Operations: Sanil Electric Co., Ltd. generates revenue primarily from its Electric Equipment segment, totaling ₩415.20 million.

Estimated Discount To Fair Value: 12.2%

Sanil Electric is trading at ₩112,600, which is 12.2% below its estimated fair value of ₩128,189.59. Despite high non-cash earnings and a volatile share price recently, the company shows strong potential with earnings expected to grow significantly over the next three years at 22.72% annually. Revenue growth is forecasted to outpace the Korean market at 21.1% per year, supported by a high projected return on equity of 27.7%.

- Our expertly prepared growth report on Sanil Electric implies its future financial outlook may be stronger than recent results.

- Unlock comprehensive insights into our analysis of Sanil Electric stock in this financial health report.

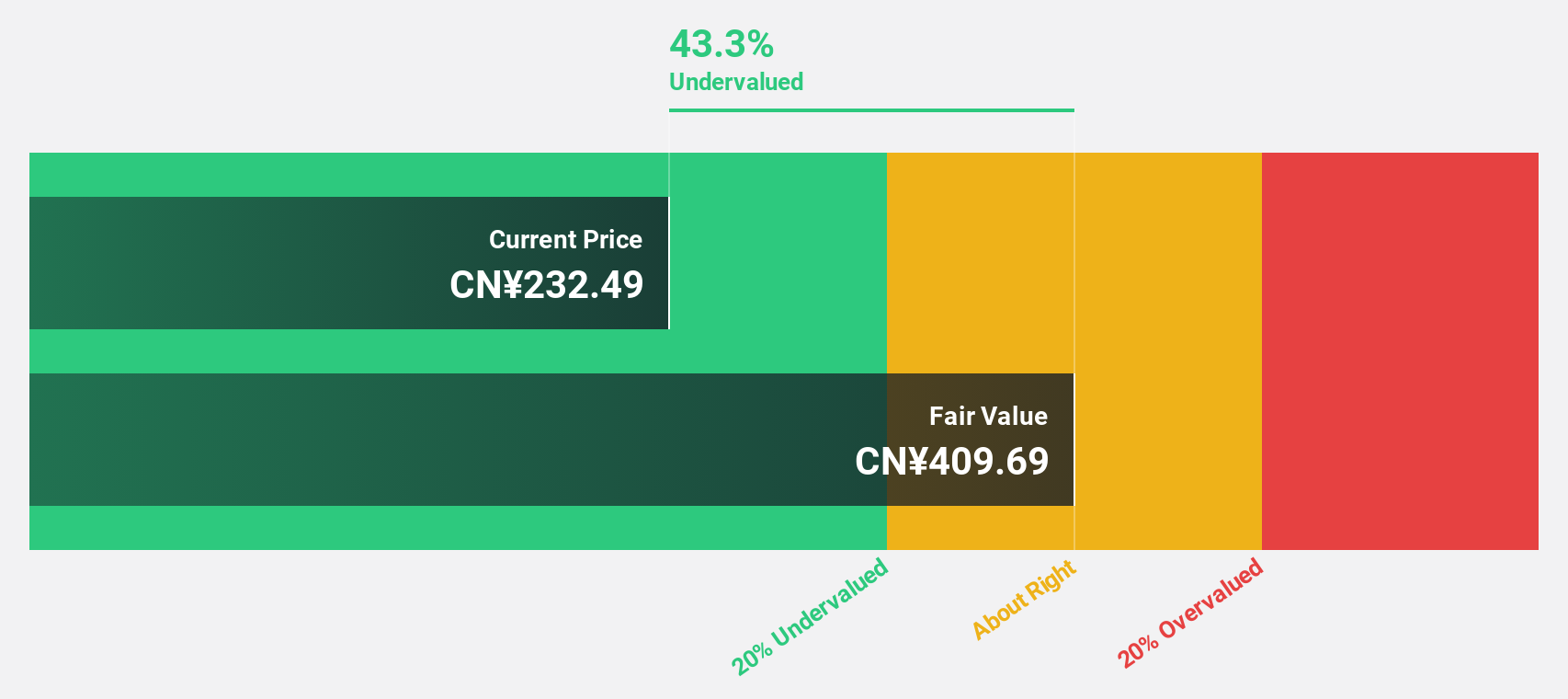

Zhejiang Cfmoto PowerLtd (SHSE:603129)

Overview: Zhejiang Cfmoto Power Co., Ltd, along with its subsidiaries, develops, manufactures, markets, and delivers motorcycles, off-road vehicles, engines, frames, parts, apparel, and accessories across various global markets including China and has a market cap of approximately CN¥41.66 billion.

Operations: Zhejiang Cfmoto Power Co., Ltd generates revenue through its diverse operations that include the production and sale of motorcycles, off-road vehicles, engines, frames, parts, apparel, and accessories across multiple regions such as China, Asia, North America, Oceania, Africa, South America, and Europe.

Estimated Discount To Fair Value: 29.4%

Zhejiang Cfmoto Power Ltd is trading at CN¥273.06, significantly below its estimated fair value of CN¥386.93, indicating it may be undervalued based on cash flows. The company's revenue and earnings are projected to grow at 20.8% and 21.1% annually, respectively, outpacing the broader Chinese market in revenue growth but lagging slightly in earnings growth. Recent half-year results showed robust sales of CN¥9.86 billion and net income of CN¥1 billion, reflecting strong operational performance.

- In light of our recent growth report, it seems possible that Zhejiang Cfmoto PowerLtd's financial performance will exceed current levels.

- Click to explore a detailed breakdown of our findings in Zhejiang Cfmoto PowerLtd's balance sheet health report.

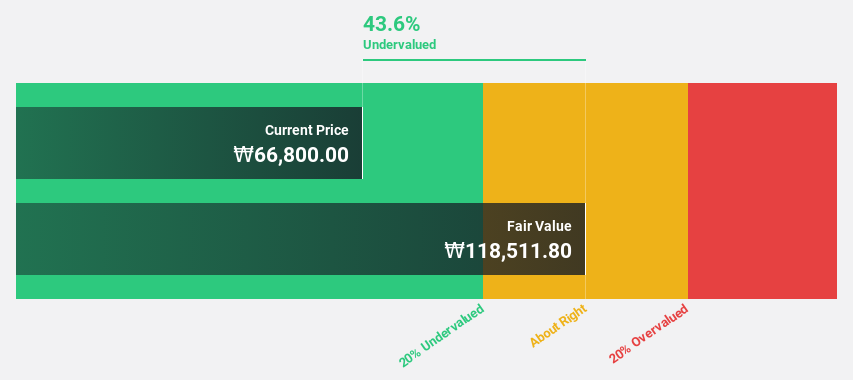

Ningbo Deye Technology Group (SHSE:605117)

Overview: Ningbo Deye Technology Group Co., Ltd. specializes in the production and sales of heat exchangers, inverters, and dehumidifiers across various international markets, with a market cap of CN¥63.31 billion.

Operations: The company's revenue is derived from its operations in producing and selling heat exchangers, inverters, and dehumidifiers across international markets such as South Africa, Brazil, Hong Kong, Germany, and India.

Estimated Discount To Fair Value: 11.2%

Ningbo Deye Technology Group is trading at CN¥70.15, below its estimated fair value of CN¥79.02, suggesting undervaluation based on cash flows. Recent earnings showed revenue of CNY 5.54 billion and net income of CNY 1.52 billion, reflecting solid growth over the previous year. While revenue is expected to grow faster than the Chinese market at 22.3% annually, earnings growth is projected to be slower at 19.2%, yet remains robust compared to peers and industry standards.

- Upon reviewing our latest growth report, Ningbo Deye Technology Group's projected financial performance appears quite optimistic.

- Dive into the specifics of Ningbo Deye Technology Group here with our thorough financial health report.

Make It Happen

- Gain an insight into the universe of 285 Undervalued Asian Stocks Based On Cash Flows by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ningbo Deye Technology Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:605117

Ningbo Deye Technology Group

Engages in the production and sales of heat exchangers, inverters, and dehumidifiers in South Africa, Brazil, Hongkong, Germany, India, and internationally.

Outstanding track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|30.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|25.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|63.2% undervalued

ME

Community Contributor