- China

- /

- Commercial Services

- /

- SZSE:300422

Improved Revenues Required Before Anhui Bossco Environmental Protection Technology Co.,Ltd. (SZSE:300422) Stock's 39% Jump Looks Justified

Anhui Bossco Environmental Protection Technology Co.,Ltd. (SZSE:300422) shares have had a really impressive month, gaining 39% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 12% over that time.

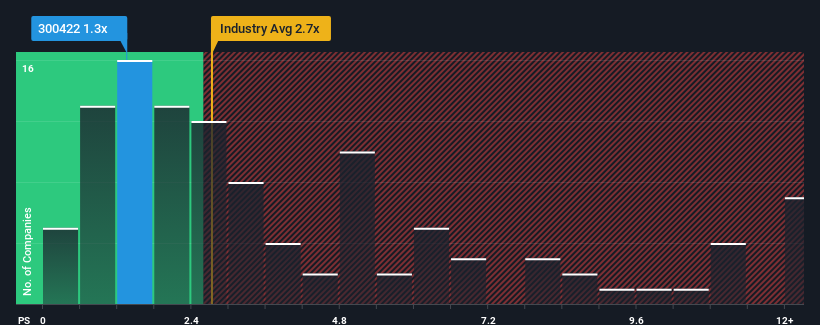

Although its price has surged higher, Anhui Bossco Environmental Protection TechnologyLtd may still be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.3x, since almost half of all companies in the Commercial Services industry in China have P/S ratios greater than 2.7x and even P/S higher than 6x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Anhui Bossco Environmental Protection TechnologyLtd

What Does Anhui Bossco Environmental Protection TechnologyLtd's Recent Performance Look Like?

Revenue has risen at a steady rate over the last year for Anhui Bossco Environmental Protection TechnologyLtd, which is generally not a bad outcome. One possibility is that the P/S ratio is low because investors think this good revenue growth might actually underperform the broader industry in the near future. Those who are bullish on Anhui Bossco Environmental Protection TechnologyLtd will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Anhui Bossco Environmental Protection TechnologyLtd's earnings, revenue and cash flow.Do Revenue Forecasts Match The Low P/S Ratio?

Anhui Bossco Environmental Protection TechnologyLtd's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Retrospectively, the last year delivered a decent 5.1% gain to the company's revenues. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 43% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 28% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this in mind, we understand why Anhui Bossco Environmental Protection TechnologyLtd's P/S is lower than most of its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Bottom Line On Anhui Bossco Environmental Protection TechnologyLtd's P/S

Anhui Bossco Environmental Protection TechnologyLtd's stock price has surged recently, but its but its P/S still remains modest. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Anhui Bossco Environmental Protection TechnologyLtd confirms that the company's shrinking revenue over the past medium-term is a key factor in its low price-to-sales ratio, given the industry is projected to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 2 warning signs for Anhui Bossco Environmental Protection TechnologyLtd (1 shouldn't be ignored!) that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300422

Anhui Bossco Environmental Protection TechnologyLtd

Anhui Bossco Environmental Protection Technology Co.,Ltd.

Good value with mediocre balance sheet.

Market Insights

Community Narratives