- China

- /

- Commercial Services

- /

- SZSE:300070

Global Growth Companies With High Insider Ownership In March 2025

Reviewed by Simply Wall St

As global markets navigate a landscape of steady interest rates and mixed economic signals, investors are closely monitoring shifts in growth and value sectors. In this environment, companies with high insider ownership can be particularly appealing as they often indicate strong internal confidence and alignment with shareholder interests.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 47.2% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| CD Projekt (WSE:CDR) | 29.7% | 39.1% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 125.9% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 60.9% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

Let's dive into some prime choices out of the screener.

HYBE (KOSE:A352820)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: HYBE Co., Ltd. operates in music production, publishing, and artist development and management, with a market cap of ₩9.70 trillion.

Operations: HYBE Co., Ltd. generates revenue primarily through its activities in music production, publishing, and the development and management of artists.

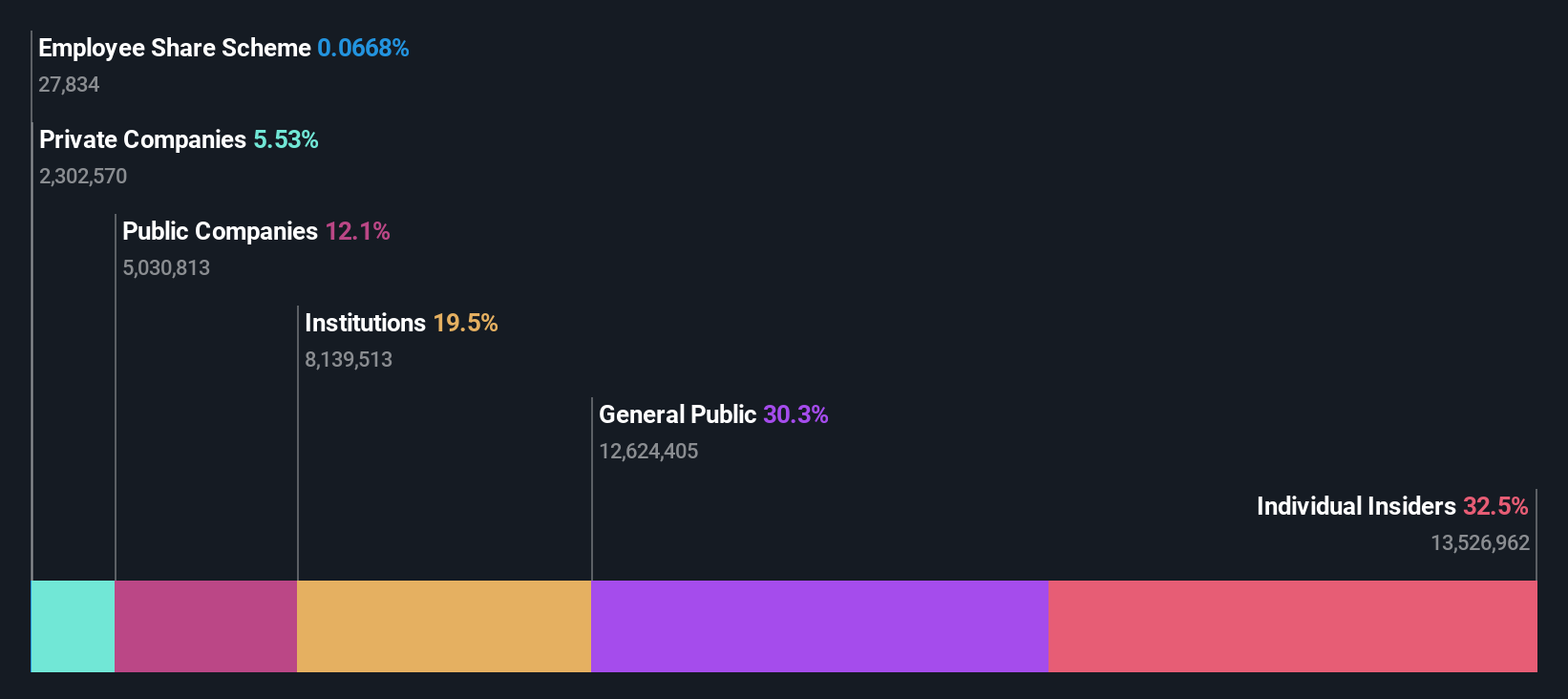

Insider Ownership: 32.5%

HYBE's earnings are projected to grow significantly at 49.1% annually, outpacing the KR market's growth rate of 23.2%. However, recent financial results show a decline in net income from KRW 187.25 billion to KRW 9.38 billion, impacting profit margins and earnings per share. Despite these challenges, HYBE's revenue is expected to grow faster than the market at 15.8% annually, though it remains below the high-growth threshold of 20%.

- Unlock comprehensive insights into our analysis of HYBE stock in this growth report.

- Upon reviewing our latest valuation report, HYBE's share price might be too optimistic.

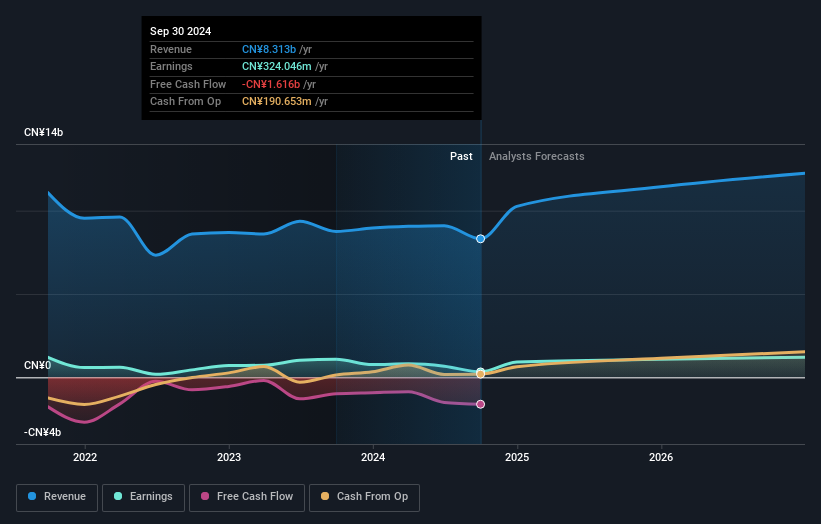

Beijing Originwater Technology (SZSE:300070)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Beijing Originwater Technology Co., Ltd. operates in the water treatment business both in China and internationally, with a market cap of CN¥17.90 billion.

Operations: Beijing Originwater Technology Co., Ltd.'s revenue segments primarily focus on the water treatment sector, serving both domestic and international markets.

Insider Ownership: 13.2%

Beijing Originwater Technology's earnings are forecast to grow significantly at 66.39% annually, surpassing the CN market's growth rate of 24.9%. Revenue growth is expected at 15.4% per year, outpacing the market's 13.1%, though below high-growth levels of 20%. Despite substantial insider ownership, recent financials reveal challenges with low profit margins (3.9%) and a Return on Equity forecasted at only 3.6%, while debt coverage by operating cash flow remains weak.

- Navigate through the intricacies of Beijing Originwater Technology with our comprehensive analyst estimates report here.

- The analysis detailed in our Beijing Originwater Technology valuation report hints at an inflated share price compared to its estimated value.

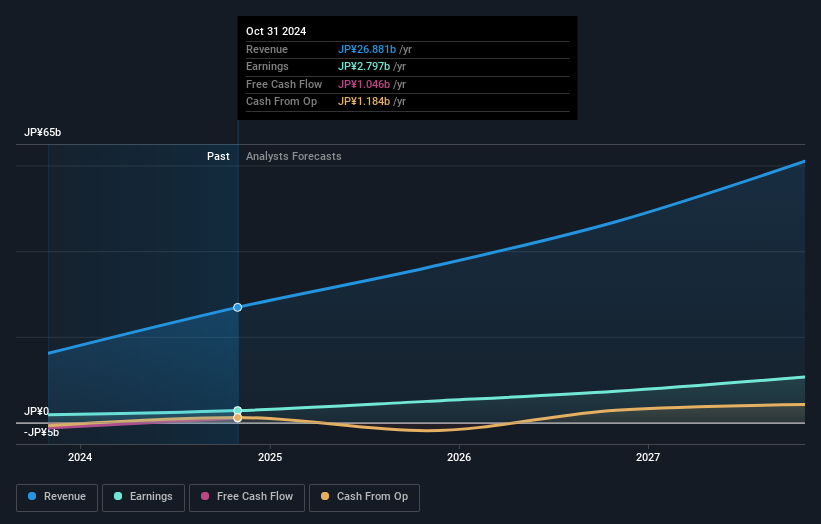

Timee (TSE:215A)

Simply Wall St Growth Rating: ★★★★★★

Overview: Timee, Inc. plans, develops, and operates a job platform in Japan with a market cap of ¥148.74 billion.

Operations: The company's revenue segment is derived from its job platform, generating ¥26.88 billion.

Insider Ownership: 25.9%

Timee, Inc. exhibits significant growth potential with earnings projected to grow at 37.59% annually, outpacing the JP market's 8%. Revenue is similarly expected to rise by 26.1% each year, surpassing the market's 4.3%. Despite a volatile share price and high non-cash earnings, Timee's Return on Equity is forecasted to be very high in three years at 42.5%, indicating robust future profitability prospects without recent insider trading activity impacting its valuation significantly below fair value estimates.

- Get an in-depth perspective on Timee's performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Timee is priced higher than what may be justified by its financials.

Turning Ideas Into Actions

- Discover the full array of 896 Fast Growing Global Companies With High Insider Ownership right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Originwater Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300070

Beijing Originwater Technology

Operates in the water treatment business in China and internationally.

High growth potential and fair value.

Market Insights

Community Narratives