- China

- /

- Commercial Services

- /

- SHSE:603359

Revenues Not Telling The Story For Dongzhu Ecological Environment Protection Co., Ltd. (SHSE:603359) After Shares Rise 38%

The Dongzhu Ecological Environment Protection Co., Ltd. (SHSE:603359) share price has done very well over the last month, posting an excellent gain of 38%. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 45% in the last twelve months.

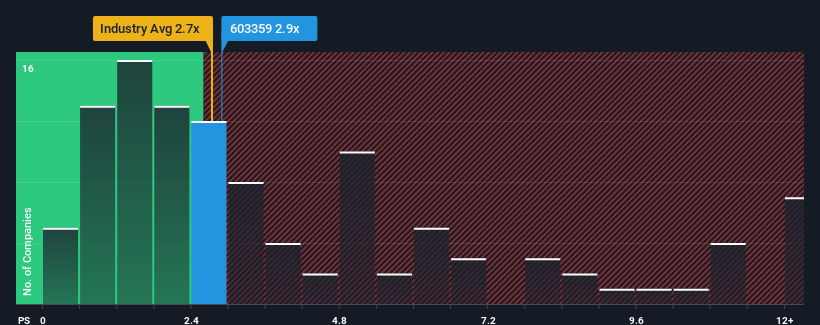

Even after such a large jump in price, there still wouldn't be many who think Dongzhu Ecological Environment Protection's price-to-sales (or "P/S") ratio of 2.9x is worth a mention when the median P/S in China's Commercial Services industry is similar at about 2.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Dongzhu Ecological Environment Protection

What Does Dongzhu Ecological Environment Protection's Recent Performance Look Like?

Revenue has risen firmly for Dongzhu Ecological Environment Protection recently, which is pleasing to see. One possibility is that the P/S is moderate because investors think this respectable revenue growth might not be enough to outperform the broader industry in the near future. Those who are bullish on Dongzhu Ecological Environment Protection will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Dongzhu Ecological Environment Protection's earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Dongzhu Ecological Environment Protection's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 8.8%. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 70% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

In contrast to the company, the rest of the industry is expected to grow by 28% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we find it worrying that Dongzhu Ecological Environment Protection's P/S exceeds that of its industry peers. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

What Does Dongzhu Ecological Environment Protection's P/S Mean For Investors?

Its shares have lifted substantially and now Dongzhu Ecological Environment Protection's P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

The fact that Dongzhu Ecological Environment Protection currently trades at a P/S on par with the rest of the industry is surprising to us since its recent revenues have been in decline over the medium-term, all while the industry is set to grow. When we see revenue heading backwards in the context of growing industry forecasts, it'd make sense to expect a possible share price decline on the horizon, sending the moderate P/S lower. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

Plus, you should also learn about this 1 warning sign we've spotted with Dongzhu Ecological Environment Protection.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603359

Dongzhu Ecological Environment Protection

Dongzhu Ecological Environment Protection Co., Ltd.

Adequate balance sheet and fair value.

Market Insights

Community Narratives