Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Jiujiang Defu Technology Co., Limited (SZSE:301511) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Jiujiang Defu Technology

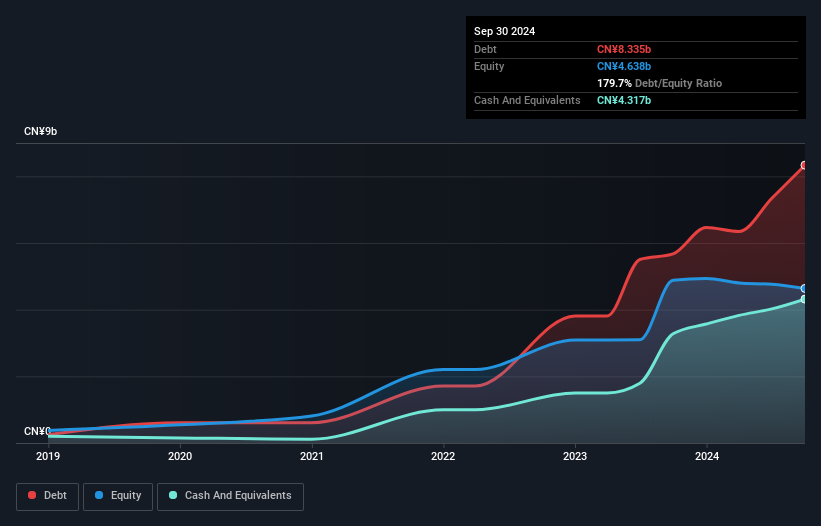

What Is Jiujiang Defu Technology's Debt?

As you can see below, at the end of September 2024, Jiujiang Defu Technology had CN¥8.33b of debt, up from CN¥5.67b a year ago. Click the image for more detail. However, it also had CN¥4.32b in cash, and so its net debt is CN¥4.02b.

How Strong Is Jiujiang Defu Technology's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Jiujiang Defu Technology had liabilities of CN¥9.96b due within 12 months and liabilities of CN¥1.46b due beyond that. On the other hand, it had cash of CN¥4.32b and CN¥3.44b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥3.67b.

While this might seem like a lot, it is not so bad since Jiujiang Defu Technology has a market capitalization of CN¥8.87b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Jiujiang Defu Technology will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Jiujiang Defu Technology wasn't profitable at an EBIT level, but managed to grow its revenue by 4.9%, to CN¥6.9b. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Jiujiang Defu Technology had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost CN¥161m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled CN¥567m in negative free cash flow over the last twelve months. So in short it's a really risky stock. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Jiujiang Defu Technology (at least 2 which are a bit concerning) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301511

Jiujiang Defu Technology

Engages in the research, development, production, and sale of electrolytic copper foil in China and internationally.

Slightly overvalued very low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor