Returns On Capital Signal Tricky Times Ahead For Gemac Engineering Machinery (SZSE:301048)

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Although, when we looked at Gemac Engineering Machinery (SZSE:301048), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Gemac Engineering Machinery:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

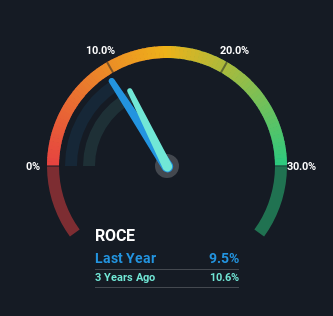

0.095 = CN¥262m ÷ (CN¥5.0b - CN¥2.2b) (Based on the trailing twelve months to September 2024).

So, Gemac Engineering Machinery has an ROCE of 9.5%. On its own that's a low return, but compared to the average of 5.2% generated by the Machinery industry, it's much better.

View our latest analysis for Gemac Engineering Machinery

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Gemac Engineering Machinery has performed in the past in other metrics, you can view this free graph of Gemac Engineering Machinery's past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

In terms of Gemac Engineering Machinery's historical ROCE movements, the trend isn't fantastic. Around five years ago the returns on capital were 15%, but since then they've fallen to 9.5%. However it looks like Gemac Engineering Machinery might be reinvesting for long term growth because while capital employed has increased, the company's sales haven't changed much in the last 12 months. It may take some time before the company starts to see any change in earnings from these investments.

On a side note, Gemac Engineering Machinery has done well to pay down its current liabilities to 45% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money. Either way, they're still at a pretty high level, so we'd like to see them fall further if possible.

The Key Takeaway

To conclude, we've found that Gemac Engineering Machinery is reinvesting in the business, but returns have been falling. Since the stock has declined 22% over the last three years, investors may not be too optimistic on this trend improving either. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

While Gemac Engineering Machinery doesn't shine too bright in this respect, it's still worth seeing if the company is trading at attractive prices. You can find that out with our FREE intrinsic value estimation for 301048 on our platform.

While Gemac Engineering Machinery may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you're looking to trade Gemac Engineering Machinery, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301048

Gemac Engineering Machinery

Engages in the research, development, production, sale, and maintenance of rail engineering equipment in China.

Flawless balance sheet and fair value.

Market Insights

Community Narratives